The company made a big bet on a fast-growing international market that has taken a turn for the worse.

For decades, the beauty sector seemed unflappable. Companies expanded to international markets where people had increasing amounts of disposable income to spend on fragrance, skincare, and makeup products. Global population growth — especially in Asia — was another major tailwind. This is how leading beauty conglomerate Estée Lauder (EL -3.63%) grew to a market cap of over $100 billion a few years ago.

Today, most of this value has been lost. How? Those prior tailwinds have turned into headwinds, especially in the Chinese market. Here’s why Estée Lauder’s stock has plunged 82% from its all-time high, and how investors should look at the stock going forward.

Chinese consumer recession

It’s no secret why beauty companies like Estée Lauder poured resources into China. The country has a population of over 1 billion people with a huge beauty culture, and growth in this market propelled revenue in Estée Lauder’s Asia Pacific segment to nearly $5.5 billion in 2021. It owns well-known brands such as Clinique, Aveda, and Bobbi Brown.

However, 2021 was also the year China’s real estate bubble collapsed with an estimated $18 trillion of wealth wiped off Chinese consumers’ balance sheets, according to banking analysts. Consumer spending in China has been woefully anemic for years now, which has greatly affected Estée Lauder’s operations.

In the company’s fiscal 2025 first quarter (ended Sept. 30), Asia Pacific revenue declined 11% year over year to $944 million. This was on top of a 6% decline in fiscal 2024 and a 4% decline in 2023. Investors see no signs of a recovery in China with management saying last quarter that consumer sentiment there continues to weaken. It doesn’t help that China’s population has started to decline and is projected to continue doing so for the next few decades.

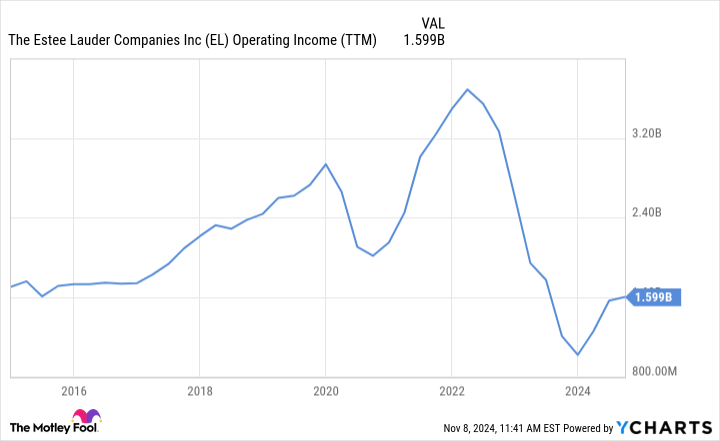

Big stock drawdown, declining profit margins

In the last 12 months alone, Estée Lauder stock is down over 40%, even though the S&P 500 has soared over the same period. The company’s trailing-12-month revenue has fallen to $15.4 billion, which is right around its pre-pandemic level. However, the stock is much lower than where it traded in 2019 and early 2020.

Estée Lauder has also struggled to manage rising costs for its business. The company’s operating margin has fallen to 10% in the last 12 months, compared to its historic range of 15% to 20%. This has dragged its trailing operating income close to a 10-year low. At the end of the day, investors care about profits, which is why Estée Lauder stock is struggling so much.

Data by YCharts.

Should you buy the dip?

Making any projection about the future of this stock requires an analysis of its future earnings potential. On the one hand, cost pressures have affected margins, and it is suffering in the Asia Pacific market. It is hard to predict if or when this pain will end.

On the other hand, the company does not solely sell products in China. It also has large markets in the Americas, Europe, and the Middle East that made up over 70% of its sales last quarter. These regions will (hopefully) offer the business some stability.

With that in mind, expectations for Estée Lauder stock are low, too. The stock’s market cap is $23 billion, or about 14 times its trailing operating income of $1.6 billion, and the challenges the company faces around profitability and weak demand in China are already priced into its shares. For long-term investors who believe in the lasting power of Estée Lauder’s brands, this could be the right time to buy the stock.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.