Markets have been in an “increasingly positive mood” since the April Federal Reserve meeting and while there are still hurdles to overcome, there are factors in the market’s favor after last month’s downturn, Deutsche Bank said this week.

The S&P 500 (SP500)(VOO)(IVV) during early May posted its best four-day performance so far this year, aided by the 10-year yield (US10Y) falling for five consecutive sessions for the first time since August, Deutsche Bank (DB) Macro Strategist Henry Allen said in a research note.

“That’s a decent turnaround from mid-April, back when the S&P 500 posted a run of 6 consecutive declines, and there were strong fears about sticky inflation and geopolitical risks,” he said. The benchmark fell 4.2% in April.

“Of course, there’s still plenty to navigate over the rest of the year, but there are several reasons to believe that a more positive market narrative is now emerging.”

DB listed “5 reasons to be positive” about stocks:

At a global level, data releases are looking increasingly positive across the board.

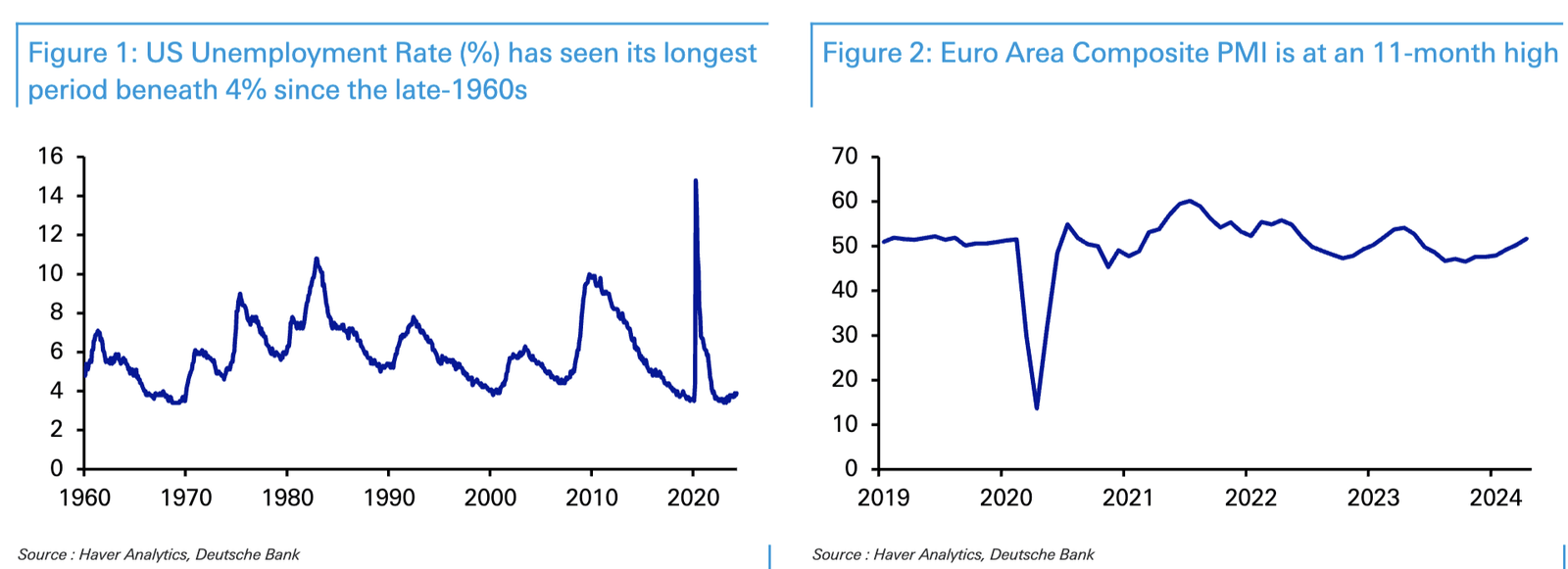

Allen said the U.S. economy remains in “robust shape,” with unemployment continuing to run below 4%. Euro-area growth is improving after several quarters of largely stagnant conditions and China’s 5.3% Q1 GDP growth was stronger than anticipated.

For now, Fed Chair Powell’s comments and data take out near-term tail risk of rate hikes.

Powell after the April meeting said it was “unlikely that the next policy rate move will be a hike,” calming market fears following heated inflation data. Allen said slightly weaker-than-expected data, including the soft April jobs report, spurred investors to price in +40 bps of rate cuts by the Fed’s December meeting, up from a low of 28bps before the April meeting.

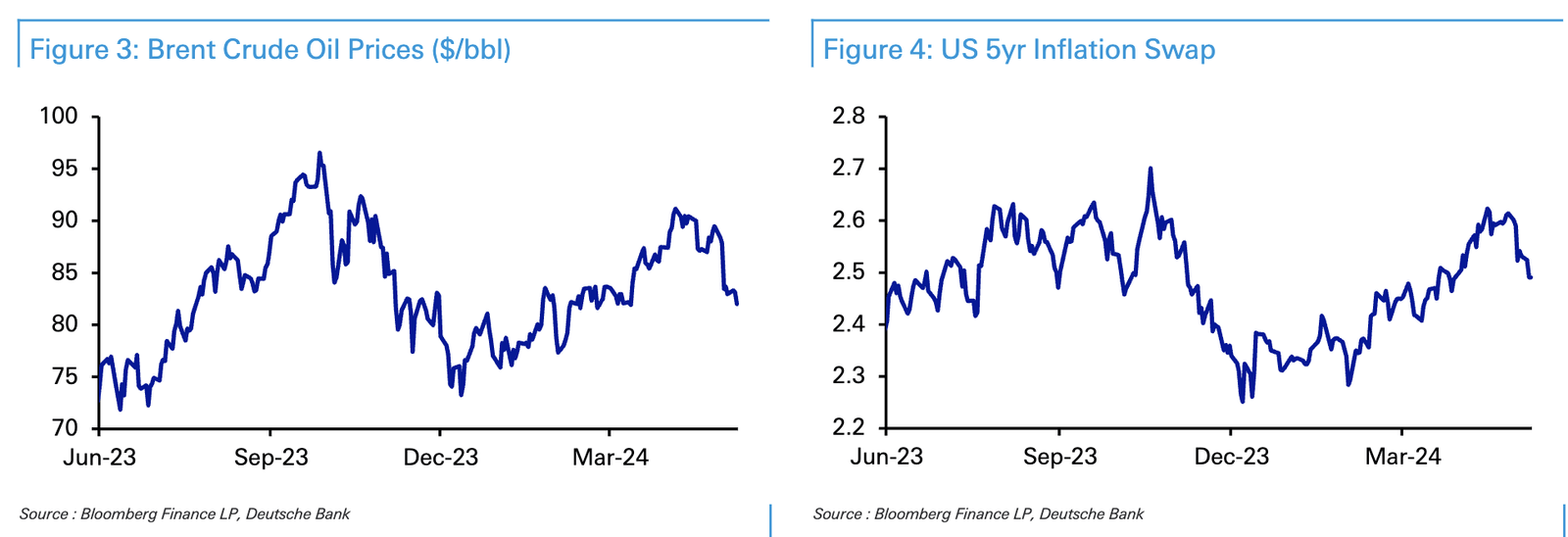

Oil prices are coming down again, helping to alleviate inflationary pressures.

Brent crude (CO1:COM) at around $83/bbl was at its lowest price in almost two months, largely because fears of a wider geopolitical escalation haven’t materialized, in turn, lowering inflation expectations, Allen said. The U.S. 5-year inflation swap this week closed below 2.5% for the first time since late March.

The global economy has continued to prove impressively resilient to higher rates so far.

There has been no major downturn given the fast speed of rate hikes, and periods of turmoil such as the Silicon Valley Bank collapse have been contained, Allen said. “Since monetary policy operates with a lag, this pass-through is still happening, particularly for fixed-rate borrowers. But with each month that passes, the economy is increasingly adjusting to the higher level of rates that now prevail.”

Recession hasn’t materialized after periodical data deterioration

Some indicators are pointing in a more negative direction, such as the 10-year yield falling below the 2-year yield (US2Y), a move that’s signaled the last 10 U.S. recessions. “But it’s been continuously inverted since July 2022, the longest 2s10s inversion on record, and there’s still no sign of a recession yet,” Allen said.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)