If you’ve been following Revolution Medicines (RVMD), you know this week brought a flurry of developments that could matter for anyone weighing their next move. Piper Sandler just initiated coverage with a confident nod, while the company itself is touting progress in key Phase 3 trials for daraxonrasib and highlighting two recent FDA Breakthrough Therapy Designations. These milestones are watched closely by biotech investors and signal increased attention from both Wall Street and regulators, putting RVMD back on the radar for growth-focused investors tracking the oncology pipeline race. Taking a step back, RVMD’s stock has seesawed over the past year, sliding roughly 16% since January and trading about 15% lower than this time last year. The short-term trend has been soft, but the long-range tells a different story, with shares up 74% in three years and still more than doubling investors’ money over five. That uneven path reflects both the risks and rewards in biotech, where clinical progress can quickly change sentiment. Investors saw this dynamic again this week after the Phase 3 and regulatory news. So, after all this news and a choppy year for the share price, does RVMD stand out as an opportunity before the market catches on, or is recent optimism already reflected in the stock’s valuation?

Price-to-Book of 3.7x: Is it justified?

Revolution Medicines currently trades at a price-to-book ratio of 3.7 times, which is notably above both the US Biotech industry average of 2x and the peer average of 2.3x. This suggests the stock is valued at a premium based on this commonly used multiple for asset-heavy biotech firms.

The price-to-book ratio compares a company’s market value to its book value. This metric is especially relevant when evaluating unprofitable biotech companies with little or negative net income. Investors look to this ratio to gauge market expectations of future asset value creation and potential breakthroughs.

This premium may indicate that the market is pricing in high expectations for Revolution Medicines’ drug pipeline and revenue growth. However, such a valuation also raises questions about whether these ambitions are justified, particularly given the company’s current lack of profitability.

Result: Fair Value of $37.01 (OVERVALUED)

See our latest analysis for Revolution Medicines.

However, regulatory setbacks or delays in clinical trials could quickly challenge optimism and remind investors how swiftly circumstances can shift in this sector.

Find out about the key risks to this Revolution Medicines narrative.

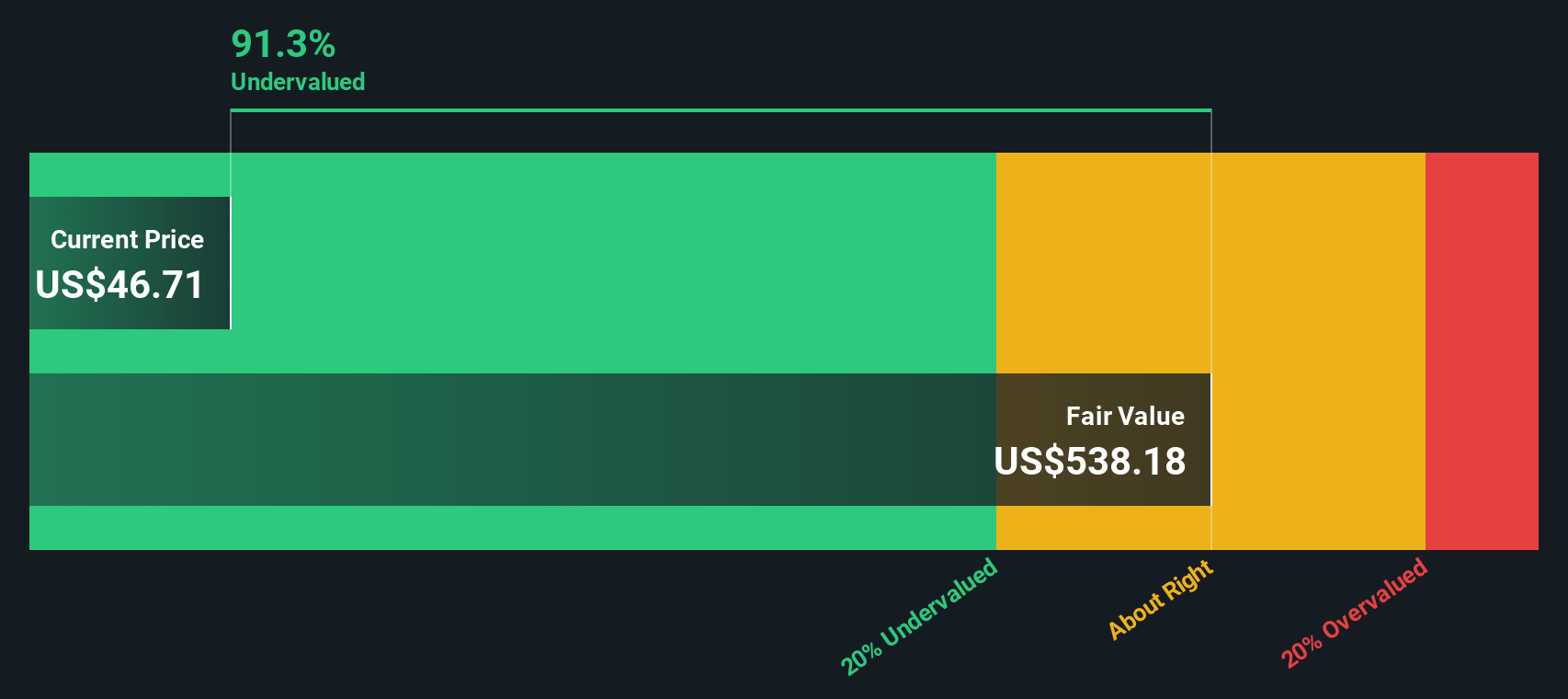

Another View: SWS DCF Model Says Undervalued

While the current market price appears expensive based on traditional asset-based metrics, our DCF model presents a different perspective and suggests the stock is deeply undervalued. The reality may lie somewhere between these two viewpoints.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Revolution Medicines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own Revolution Medicines Narrative

If you see the story differently or want to dig into the numbers on your own terms, it’s easy to build a personal take on RVMD in just a few minutes, so you can do it your way.

A great starting point for your Revolution Medicines research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Compelling Investment Ideas?

Smart investors keep options open and seize opportunities others miss. If you want to spot stocks with stronger potential or unique angles, put the Simply Wall Street Screener to work for you. Here are three strategies you can use right now to uncover what might be next in your portfolio:

- Find stability and steady income with a curated selection of dividend stocks with yields > 3% delivering yields above 3%, which could help anchor your long-term returns.

- Stay ahead of the next tech boom by exploring the most promising AI penny stocks that are shaping the future of artificial intelligence across industries.

- Spot value hiding in plain sight using our powerful insights to reveal undervalued stocks based on cash flows trading below their cash flow potential before the rest of the market takes notice.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com