As global markets react to changes in interest rates and trade developments, Asian economies are navigating a complex landscape marked by economic slowdowns and potential stimulus measures. In this environment, identifying undervalued stocks becomes crucial for investors seeking opportunities that align with current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Tibet GaoZheng Explosive (SZSE:002827) | CN¥38.64 | CN¥76.93 | 49.8% |

| Selvas AI (KOSDAQ:A108860) | ₩14310.00 | ₩28429.24 | 49.7% |

| Pansoft (SZSE:300996) | CN¥17.12 | CN¥33.73 | 49.2% |

| NexTone (TSE:7094) | ¥2260.00 | ¥4458.55 | 49.3% |

| Kolmar Korea (KOSE:A161890) | ₩78900.00 | ₩155317.12 | 49.2% |

| Inspur Digital Enterprise Technology (SEHK:596) | HK$9.38 | HK$18.75 | 50% |

| FP Partner (TSE:7388) | ¥2260.00 | ¥4425.25 | 48.9% |

| Food Empire Holdings (SGX:F03) | SGD2.65 | SGD5.15 | 48.5% |

| Everest Medicines (SEHK:1952) | HK$54.70 | HK$107.56 | 49.1% |

| Anhui Ronds Science & Technology (SHSE:688768) | CN¥49.57 | CN¥96.92 | 48.9% |

Underneath we present a selection of stocks filtered out by our screen.

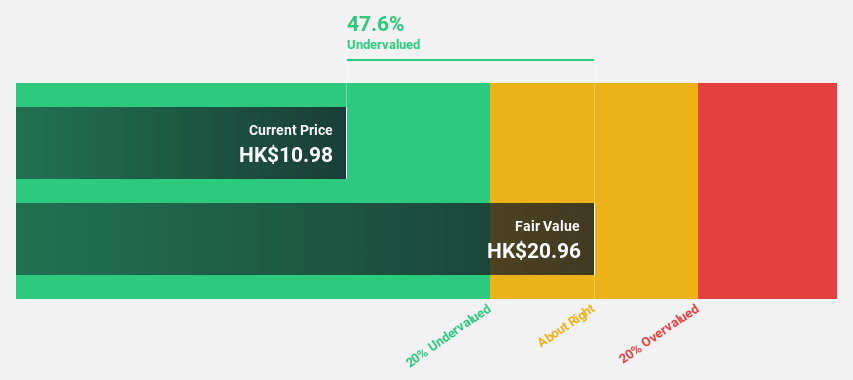

InnoCare Pharma (SEHK:9969)

Overview: InnoCare Pharma Limited is a biopharmaceutical company focused on discovering, developing, and commercializing drugs for cancer and autoimmune diseases in China, with a market cap of HK$34.11 billion.

Operations: InnoCare Pharma Limited generates revenue from its pharmaceuticals segment, which amounted to CN¥1.32 billion.

Estimated Discount To Fair Value: 29.3%

InnoCare Pharma, trading at HK$17.31, is significantly undervalued based on discounted cash flow analysis with a fair value estimate of HK$24.49. The company has shown strong revenue growth, reporting CNY 731.43 million for the first half of 2025 compared to CNY 419.74 million a year ago, and is expected to maintain high revenue growth rates exceeding market averages. Recent approvals for its novel drug orelabrutinib in Singapore and China further bolster its potential future cash flows amidst ongoing clinical advancements in oncology treatments.

- Our earnings growth report unveils the potential for significant increases in InnoCare Pharma’s future results.

- Take a closer look at InnoCare Pharma’s balance sheet health here in our report.

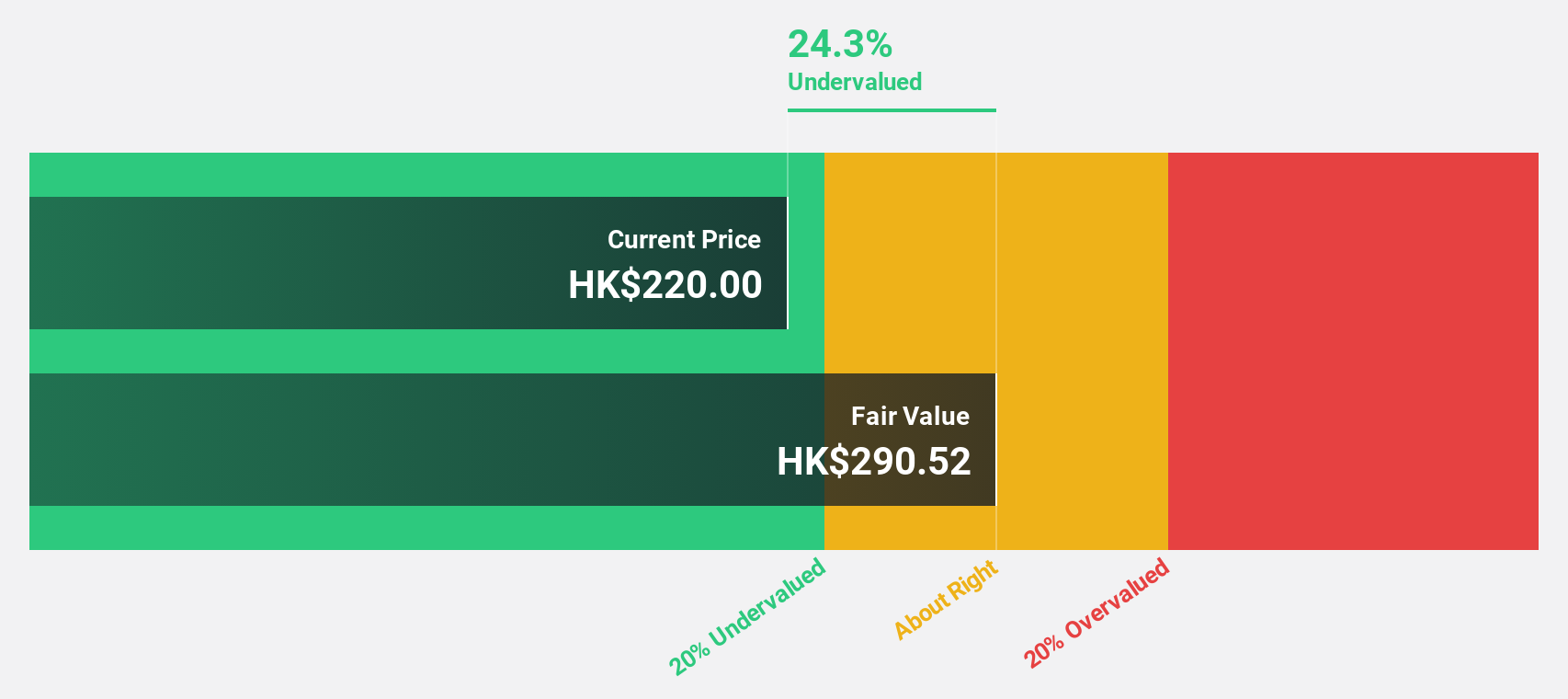

Pop Mart International Group (SEHK:9992)

Overview: Pop Mart International Group Limited is an investment holding company that designs, develops, and sells pop toys across the People’s Republic of China, Hong Kong, Macao, Taiwan, and internationally with a market cap of HK$343.73 billion.

Operations: The company’s revenue primarily comes from its brand development, design, and sales of toys, generating CN¥22.36 billion.

Estimated Discount To Fair Value: 10.4%

Pop Mart International Group, trading at HK$258.8, is undervalued based on discounted cash flow analysis with a fair value estimate of HK$288.69. The company reported substantial earnings growth for the first half of 2025, with sales reaching CNY 13.88 billion and net income at CNY 4.57 billion compared to the previous year. Its addition to several major indices and a strategic partnership with Books-A-Million highlight its expanding market presence and potential for future revenue growth above market averages.

- According our earnings growth report, there’s an indication that Pop Mart International Group might be ready to expand.

- Unlock comprehensive insights into our analysis of Pop Mart International Group stock in this financial health report.

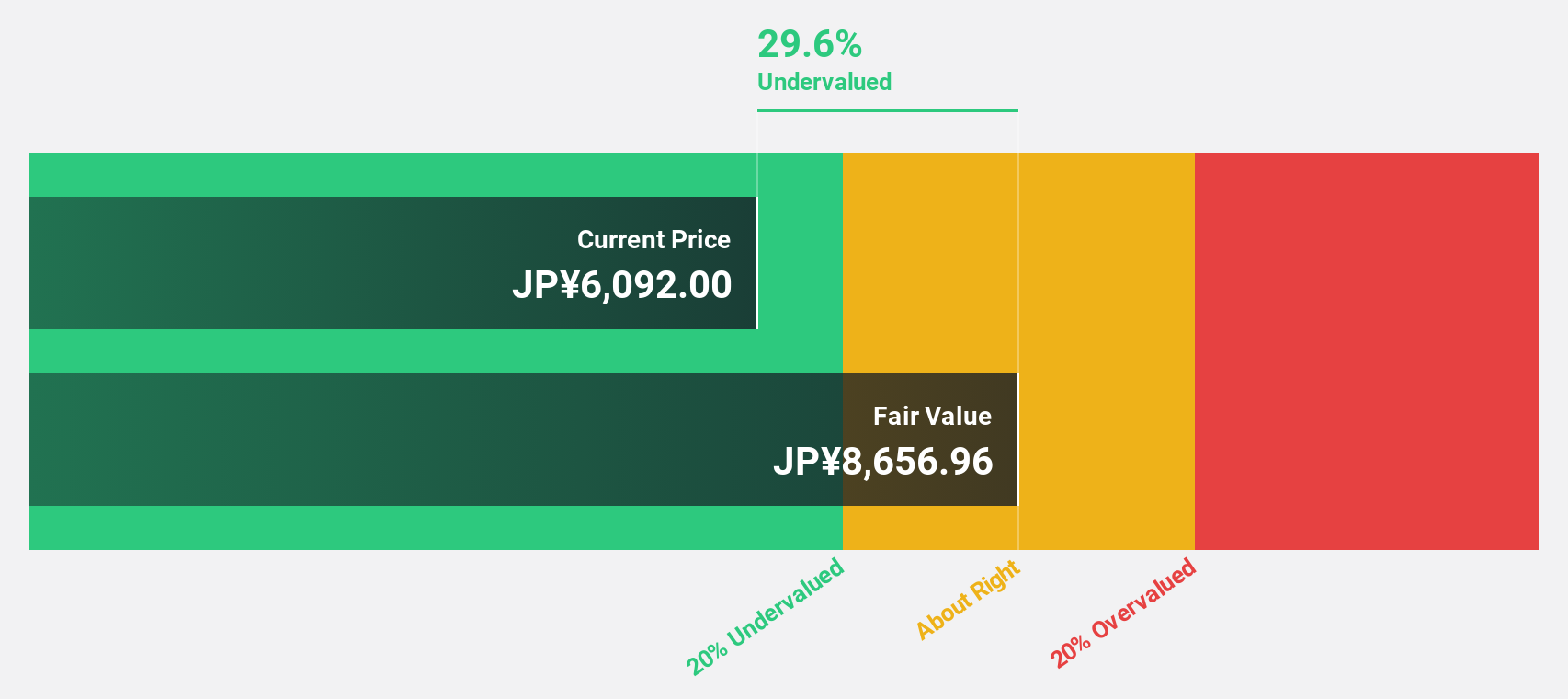

Chugai Pharmaceutical (TSE:4519)

Overview: Chugai Pharmaceutical Co., Ltd. is a company that, along with its subsidiaries, focuses on the research, development, manufacture, sale, importation, and exportation of pharmaceuticals both in Japan and globally; it has a market cap of ¥11.14 trillion.

Operations: The company’s revenue primarily comes from its Pharmaceuticals segment, which generated ¥1.20 trillion.

Estimated Discount To Fair Value: 24.6%

Chugai Pharmaceutical, trading at ¥6,772, is undervalued based on discounted cash flow analysis with an estimated fair value of ¥8,985.23. Recent positive results from the ACHIEVE-3 trial with Eli Lilly underscore Chugai’s potential in diabetes treatment innovations. The company’s earnings are projected to grow 8.54% annually, outpacing the Japanese market average. However, its share price has been highly volatile recently despite robust revenue growth forecasts and a strategic focus on enhancing R&D capabilities through new infrastructure investments.

- Our expertly prepared growth report on Chugai Pharmaceutical implies its future financial outlook may be stronger than recent results.

- Get an in-depth perspective on Chugai Pharmaceutical’s balance sheet by reading our health report here.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 273 Undervalued Asian Stocks Based On Cash Flows now.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St’s portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it’s free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com