Despite there being no resolution in sight in for the US government shutdown, Wall Street’s S&P 500 index has still managed a marginal rise to reach yet another record close.

On the local market, the 0.3 per cent gain implied by futures trading might be enough to deliver the ASX 200 the 32 points needed to hit a new record close today.

Follow the day’s financial news and insights from our specialist business reporters on our live blog.

Disclaimer: this blog is not intended as investment advice.

Key Events

Market snapshot

- ASX 200: +0.3% to 9,011 points

- Australian dollar: -0.2% at 65.86 US cents

- Wall Street (Friday): S&P500 flat, Dow +0.5%, Nasdaq -0.4%

- Europe (Friday): Dax -0.2%, FTSE +0.7%, Eurostoxx +0.2%

- Spot gold: +0.6% at $US3,913/ounce

- Brent crude: +0.9% to $US 65.11/barrel

- Iron ore (Friday): -0.1% at $US103.70/tonne

- Bitcoin: +0.5% at $US123,336

Prices current at around 10:15am AEDT

Key Event

ASX 200 on track for fresh record, opens 0.3% higher

The ASX 200 has opened 0.3% higher to be on track for a record close (11:00am AEDT).

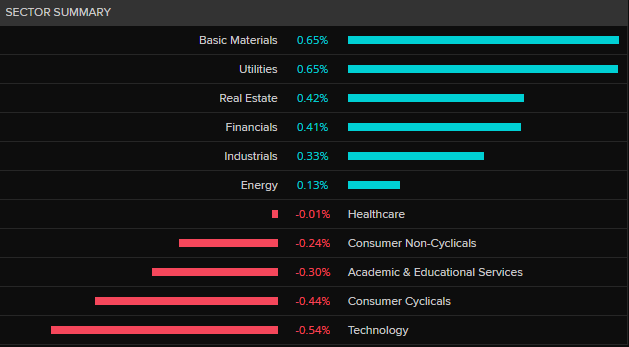

The materials and relatively small utilities sectors are leading the way, while discretionary retail and technology stocks are less in favour.

Financials stocks are well bid with the banks are being led by Westpac (+0.7%) while QBE (+1.4%) is the best of the insurers.

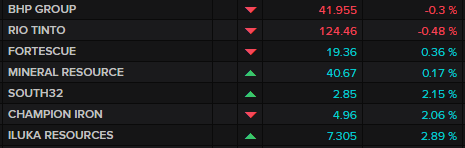

While the materials sector is generally stronger, the mega miners BHP (-0.3%) and Rio Tinto (-0.4%) are weaker.

Gold miners continue to be in demand as the spot price for the metal pushes through $US3,900/ounce to a new record high.

Rare earth miners and explorers are also enjoying a solid start with Lynas up 3.5%.

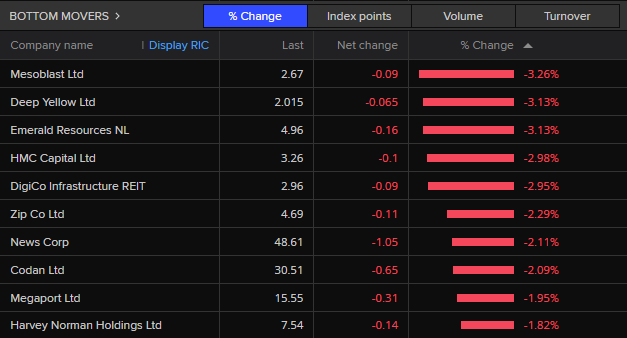

However, uranium miners are being sold off after a solid recent run with Deep Yellow deeply red (-3.1%).

Retailers are spluttering along – Coles is up 0.1%, while Woolworths (-0.5%) and Harvey Norman (-1.4%) are out of favour.

The top movers on the ASX 200 are headed by building materials maker James Hardie (+4.2%) followed by an array of rare earth, lithium and gold miners.

Stem cell focussed biotech Mesoblast is the worst performer on the ASX 200 down more than 3% this morning.

ASX opens 0.3% higher

The ASX 200 has opened 0.3% higher at 9011.2 points (11:15 am AEDT) — which, for those interested in such things, is 0.1 point higher than its record close posted in August.

Will it hang on for a fresh record today? Stick with the blog and we’ll let you know.

ICYMI: Kohler on housing’s ‘chicken or egg’ quandry

Heaven forbid, but if you were watching the “Festival of the Boot” last night and not ABC’s esteemed 7pm news bulletin, you would have missed another thought-provoking look at Australia’s housing problems from guru-in-residence Alan Kohler.

Problem solved, here’s Alan’s piece attempting to unscramble housing’s chicken vs egg/supply vs demand debate.

Loading…

This week: Consumers surveyed, US shutdown continues

Australia:

Mon: Inflation gauge (Sep)

Tue: Consumer confidence (Oct) Job ads (Sep)

Thu: Consumer inflation expectations (Oct)

Fri: RBA Governor front senate committee, Business turnover (Aug)

International:

Tue: US — Trade balance (Aug), Consumer credit (Sep)

Wed: NZ — RBNZ rates decision

US — Fed Reserve meeting minutes

Thu: US — Wholesale trade & inventories (Aug)

Fri: US- Consumer sentiment (Oct), Federal budget balance

All up, it’s a quiet week for macro wonks, both domestically and internationally.

Locally, the highlight may be RBA Governor Michele Bullock fronting a Senate committee meeting on Friday.

She dispatched the House of Reps economics committee with consummate ease last month — expect more of the same this time around.

The Westpac/Melbourne Institute consumer confidence survey (Tuesday) is always worth a look and may shift subtly either way, depending on whether those surveyed have picked up on the RBA’s slightly more hawkish stance on rate cuts recently.

Across the ditch, the NZ Reserve Bank is expected to cut rates again, and it could be 50 bps, which may be interesting if you’re planning a trip to NZ anytime soon.

The US? Well, who knows what’s coming out this week, given the government shutdown, which has dried up the data flow is likely to continue for some time yet.

There could be a deluge of backlogged releases if the Senate deadlock is broken, or maybe nothing.

Friday’s consumer sentiment survey is compiled by the University of Michigan, so it should be OK, if slightly gloomier.

One other release worth keeping an eye out for is the RBA’s annual report on Wednesday.

It’s always a good read, and interesting to see how much the bank has made, or lost, on currency transactions.

Spoiler alert: The RBA generally makes a motza from its FX trading and pays a handy dividend to the federal government.

Key Event

OPEC+ raises output targets again

The oil cartel OPEC+ has raised its output targets again, further unwinding years of cuts in an effort to wrest back market share from US producers.

OPEC+ said it would raise oil output from November by 137,000 barrels per day (bpd) the same level of increase as announced for October.

While only a modest increase, it comes amid persistent concerns among producing nations of a looming supply glut.

Brent prices briefly fell below $US65 per barrel on Friday, as analysts predict a supply glut in the fourth quarter and in 2026 due to slower demand and rising US supply.

Prices are trading below this year’s peaks of $US82 per barrel but above $US60 per barrel seen in May.

The meeting highlighted differences in opinion between two of OPEC+’s most powerful members.

Russia pushed for the modest increase to avoid putting prices under further pressure, while Saudi Arabia argued for a production increase of three-to-four times larger than the agreed target with an aim of winning back market share and putting US shale oil producers under pressure.

“OPEC+ stepped carefully after witnessing how nervous the market had become,” Rystad Energy’s Jorge Leon told Reuters.

“The group is walking a tightrope between maintaining stability and clawing back market share in a surplus environment.”

Key Event

ASX set to follow Wall Street’s lead higher

The key Wall Street index, the S&P 500 eked out a marginal rise on Friday, but it was still enough to chalk up another record close.

The 0.01% gain was marginal but still a gain.

The blue-chip Dow picked up 0.5%, but the Nasdaq gave up 0.4% as tech stocks took a bit of a breather from their recent run.

ASX 200 futures closed on Friday up 0.3%.

A gain of about that size could deliver the 32 points needed to eclipse the record close of 9,091 points hit in August.

Friday’s trade rumbled on in the dark about the latest happenings in the labour market, given the Bureau of Labor Statistics, like virtually every US government agency, remained shut down.

Congress is one exception to the shutdown.

It seems the Senate is no closer to solving the budgetary impasse, but elected members continue to get paid handsomely despite orchestrating the closure of everyone else’s jobs.

The only fresh data came from the private sector, where the Institute for Supply Management’s survey showed the services employment index contracted for the fourth consecutive month.

Not compelling evidence, but it leans in favour of more interest rate cuts from the Federal Reserve.

“It certainly feels like momentum is on the side of investors over the last few days,” head of investment strategy at Edward Jones, Mona Mahajan, told Reuters.

Over the week the S&P 500 gained 1.1%.

However, that was outpaced by the Eurozone (+2.7%), China (+2.0%) and Australia (+2.3%).

Oil continued its slide to be down 1% for the session and down 7.4% for the week.

Metals had a better time of it.

Gold (+0.8%) notched its seventh consecutive positive week and will stroll through $US4,000/ounce in the near term if analysts at investment bank HSBC are correct.

Copper hit a 16-month high to have its best week of the year, up 2.2% on Friday to $US10,719/tonne.

Bitcoin also briefly hit a record high above $US125,000, before edging lower.

Good morning

Good morning and welcome to another day on the ABC markets and finance blog.

Stephen Letts from ABC business team limbering up for a blow-by-blow coverage of the day’s events, where every post is hopefully a winner, but none should be construed as financial advice.

In short, it looks like the ASX will push higher, with futures trading pointing to a 0.3% gain on opening.

That might be just enough to deliver a new record close on the ASX 200 above 9019 points.

As always, the game’s afoot, so let’s get blogging.

Loading

Market Snapshot

- ASX 200 futures: +0.3% to 9,045 points

- Australian dollar: -0.2% at 65.87 US cents

- Wall Street: S&P500 flat, Dow +0.5%, Nasdaq -0.4%

- Europe: Dax -0.2%, FTSE +0.7%, Eurostoxx +0.2%

- Spot gold: +0.8% at $US3,886/ounce

- Brent crude: -1.0% to $US 65.40/barrel

- Iron ore: -0.1% at $US103.70/tonne

- Bitcoin: +0.7% at $US122,766

Prices current at around 7:00am AEDT