Customers Bancorp (CUBI) is back on investors’ radar after fresh Wall Street coverage highlighted its expanding commercial banking teams and its growing cubiX real time payments platform, a combination that is reshaping its deposit base and funding costs.

See our latest analysis for Customers Bancorp.

The latest coverage comes as the share price has climbed to $71.65 and logged a robust year to date share price return of just over 51%, while the five year total shareholder return above 300% suggests momentum has been building, not fading.

If this kind of steady execution appeals to you, it could be a good time to explore other banks and lenders using solid balance sheet and fundamentals stocks screener (None results) to see which names also pair growth with resilient balance sheets.

With shares already near recent highs and analysts still seeing upside, the key question now is whether Customers Bancorp’s improving fundamentals justify a higher valuation, or if the market has already priced in the next leg of growth.

Most Popular Narrative Narrative: 16% Undervalued

With Customers Bancorp last closing at $71.65 against a narrative fair value near $85, the storyline leans toward meaningful upside driven by growth.

The rapid digitization of commercial banking and payments is driving institutional clients to seek tech focused, 24/7 banking solutions, a shift that Customers Bancorp capitalizes on through its proprietary cubiX platform. With payments volume of $1.5 trillion in 2024 and accelerating growth, ongoing regulatory clarity around digital assets and stablecoins positions Customers as the leading provider, supporting significant potential for deposit and fee income growth.

Want to see what kind of revenue surge and margin lift this payments engine is betting on, and how that feeds into long term earnings power and valuation? The narrative lays out a multi year roadmap that turns today’s niche digital banking edge into tomorrow’s mainstream profit machine, but the exact growth curve and profit multiple might surprise you. Dive in to uncover the assumptions behind this projected upside.

Result: Fair Value of $85.33 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, several risks remain, particularly around concentration in digital asset deposits and execution challenges in scaling cubiX profitably amid intensifying competition and regulatory scrutiny.

Find out about the key risks to this Customers Bancorp narrative.

Another Angle on Valuation

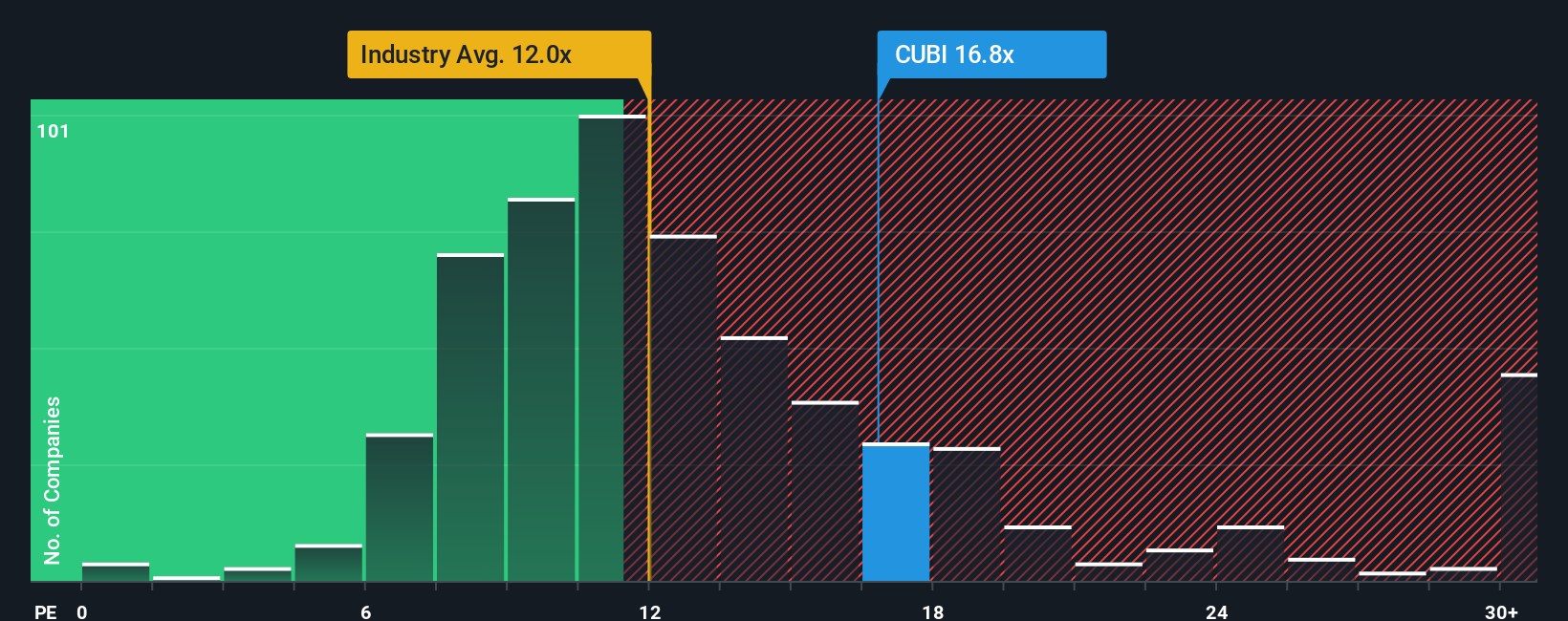

Looked at through its price to earnings ratio, Customers Bancorp is less obviously cheap. The stock trades around 15.1 times earnings versus 11.6 times for the US banks industry and 12.5 times peers, even though a fair ratio of 16.5 times suggests some, but not huge, upside left. Is that premium a cushion or a ceiling if growth stumbles?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Customers Bancorp Narrative

If you see the numbers differently or want to dig into the details yourself, you can build a custom view in minutes: Do it your way.

A great starting point for your Customers Bancorp research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by using the Simply Wall Street Screener to uncover stocks that match your goals with data backed insights.

- Boost your growth potential by targeting these 25 AI penny stocks that are reshaping industries with breakthrough automation and intelligent software.

- Secure your income stream by focusing on these 12 dividend stocks with yields > 3% that can help support steady cash returns in changing markets.

- Position yourself early in disruptive finance trends by zeroing in on these 81 cryptocurrency and blockchain stocks that may benefit as blockchain adoption accelerates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com