Do you remember what you were doing exactly a year ago? Most likely, you were glued to your Bloomberg terminal or responding to calls and emails from your clients while the S&P 500 index plunged by as much as 18.7% from its peak in February. Yes, it has already been a year since ‘Liberation Day,’ and the image that has gone down in history is that of Donald Trump holding an enormous board listing each of the tariffs that the U.S. was going to apply to countries with which it maintained a large trade deficit—though not exclusively.

For the markets, this staging had another meaning: the return of volatility and uncertainty that continue today, now driven by geopolitics and oil. As Mauro Valle, head of fixed income at Generali AM (part of Generali Investments), points out when taking stock of this first year of a new normal in U.S. trade policy, the most relevant aspect is the changes in the market that have occurred since Liberation Day.

“President Trump’s protectionist policy had two consequences in the months following the announcement of the tariffs. The first was in the bond market, where the yield on the 10-year U.S. Treasury rose sharply. The second, which still largely persists, was a weaker dollar against currencies such as the euro. In fact, the dollar has depreciated in recent months due to other factors such as twin deficits, geopolitics, and the fragmentation of global capital flows. However, in these recent phases of acute risk aversion, it can still strengthen tactically, reflecting its liquidity function. It remains to be seen whether, after this crisis, the dollar will continue to be perceived as a safe-haven asset or not,” explains Valle.

Market Performance

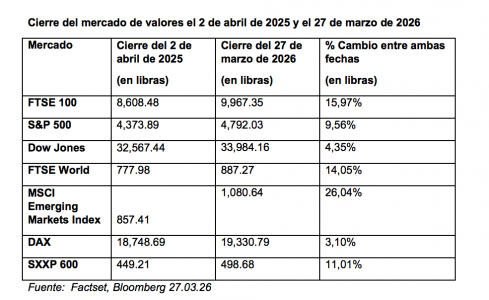

The surprise has been that, despite the initial impact, the balance of the past year shows a different message: emerging markets defied expectations and led the gains in global stock markets one year after the announcement of the Liberation Day tariffs. According to data analyzed by Aberdeen Investments, which focuses on comparing percentage changes to assess how markets have performed across six major global markets between the market close on April 2, 2025, and one year later, on March 27, 2026, overall, most major indices experienced positive dynamics, with emerging markets at the forefront.

According to the asset manager, global stock markets recorded strong gains over the period, but the MSCI Emerging Markets index had the best performance, with a rise of 26%, followed by the FTSE 100, with 16%, and the FTSE World, with 14.1%. Meanwhile, the S&P 500 posted an increase of 9.6%, while the Dow Jones and the DAX recorded more modest gains of 4.4% and 3.1%, respectively.