The ASX is on the slide today despite Wall Street posting record highs.

And despite all the share market hope of de-escalation in the Iran war, the price of oil remains elevated, well above $90 a barrel.

Locally, the Australian market is waiting on a damage report from a fire at one of its only two fuel refineries.

Follow the day’s financial news and insights from our specialist business reporters on our live blog.

Disclaimer: This blog is not intended as investment advice.

Key Events

Market snapshot

S&P/ASX 200: -0.5% to 8,905 points

Australian dollar: 0.1% at 71.6 US cents

Dow Jones: +0.2% to 48,578 points

S&P 500: +0.3% to 7,041 points

Nasdaq: +0.4% to 24,102 points

FTSE: +0.2% to 10,589 points

EuroStoxx: -0.1% to 616 points

Spot gold: -0.1% to $US4,782/ounce

Brent crude: -1.0% to $US98.35/barrel

Iron ore: +0.4% to $US106.75/tonne

Bitcoin: -0.3% to $US74,905

Prices current around 11:30am AEST.

Live updates on the major ASX indices:

Gold heads for fourth weekly gain

Gold prices are holding steady and on pace for a fourth straight weekly gain on hopes of a lasting US-Iran peace deal. The idea is that any deal struck or further de-escalation in the conflict could reduce the risk of oil-driven inflation and the need for higher interest rates. Bullion was practically flat at US$4,795 an ounce as of 1.10pm AEST, having added nearly 1% this week.

Gold often does better when inflation starts to ease and investors think interest rates will come down. Lower interest rates make gold more appealing because there’s less income to miss out on by holding it, since gold doesn’t pay interest or dividends.

The precious metal has bounced back a bit lately, but it’s still almost 9% lower than where it was before the conflict began in late February. Early on, investors rushed to sell gold to get cash and make up for losses elsewhere.

RBA speaks on IMF Panel

The Reserve Bank’s chief economist, Sarah Hunter, has been sharing her thoughts on an IMF panel.

The topic of discussion was: Rethinking Macro Policy Frameworks for a Transforming, Shock Prone World.

I’ll paraphrase that for you: how do we analyse stuff in a really unpredictable world?

Here’s some of what she said on the panel:

“Many households now around the world, in Australia and in all countries, will be struggling with and grappling with higher fuel prices.

They will be making some really hard trade-offs.

And that could well, in many countries, slow growth down, put pressure on our unemployment rates and feed through into our labour market more broadly.

We’re certainly using scenarios more now than we have in the past.

The key question for me is, what are you trying to communicate with the scenario?

In a very sort of technical decision-making sense, it is a risk exercise.

It’s considering alternative different risks, different states of the world, and how monetary policy would respond under those different states.

That’s what our policy committees are having to grapple with.”

Oxford Economics lowers global growth forecast

Here’s an excerpt from Oxford Economics’s latest international macroeconomic note:

We have lowered global GDP growth forecast to 2.4%, reflecting prolonged shipping disruption and slower energy normalisation, with oil around US$113/barrel in Q2 pushing inflation higher and weighing on demand.

Several rate hikes remain on the cards

The Australia 3-year bond is currently yielding 4.66%.

The cash rate (short end of the yield curve) is at 4.1%.

It’s worth noting that despite woeful reading on both consumer and business confidence from Westpac and the NAB, the money market is still fully pricing in at least two more RBA interest rate hikes.

Australia’s 10-year Treasury bond is also back above 5%.

Economy to slow: Westpac

Westpac is forecasting the Australia’s economic growth to slow in the back half of this calendar year.

Here’s an excerpt from a note just now from senior economist, Pat Bustamente.

Westpac Now points to moderating growth even before the RBA’s rate hikes took effect on the economy, with recent confidence weakness not yet feeding through to activity but posing a growing downside risk.

Consistent with our first estimate, Westpac Now points to GDP growth of around 0.6%qtr in Q1 2026 (range: 0.55–0.75%qtr), lifting year ended growth to 2.8%yr.

Largest super fund, AustralianSuper, becomes substantial holder in Qantas

AustralianSuper has become a substantial shareholder in Qantas, acquiring a 5.27% stake (79.6 million shares) after investing more than $130 million during recent market volatility.

The fund capitalised on a 13% year-to-date share price decline triggered by soaring jet fuel costs linked to the Middle East conflict.

On Tuesday, the airline announced it has reduced domestic flight capacity in May and June due to higher fuel costs and the uncertainty of the Middle East war. Qantas also flagged as much as $800 million in extra fuel costs.

What does the Viva fire mean for petrol prices?

The Prime Minister visited the Viva oil facility earlier today, announcing it is still operating, but at a reduced capacity.

What should Australians expect in terms of fuel supply against the backdrop of the ongoing energy crisis? ABC’s Carrington Clarke and Alan Kohler break it down on the latest episode of Fuelcast, out now.

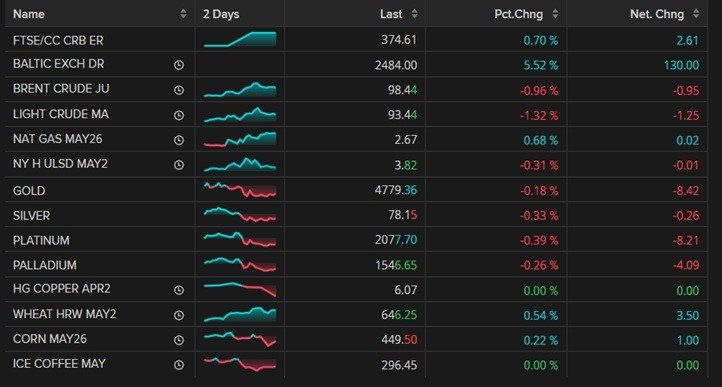

Oil price still elevated

The price of global benchmark Brent crude is well down from its peaks, but it remains elevated.

Here’s a list of commodities and their prices at 11:15am AEST.

ICYMI: Monday’s video finance report

Did you miss Alan Kohler’s/David Chau’s finance report last night? Don’t stress, we’ve got you. The numbers refer to yesterday’s data, so catch up on where we’ve been to get a steer on where you’re going today.

Worried about fuel? Don’t be

The ABC has a fantastic compendium page of where we’re at with our fuel situation.

It refines the news (sorry) for you.

People spending less, once you strip out fuel

I’m a huge fan of anonymised bank account data.

The Commonwealth Bank has their household spending indicator and Westpac has a Card Tracker Index.

Westpac’s head of Australian macro-forecasting, Matthew Hassan, says card activity points to “continued slowing” in things that aren’t fuel.

“Monthly growth has been very choppy, the fuel price spike and lift in volumes driving a 1.9% gain in the March month but the temporary halving in fuel excise tax contributing to a pullback in the first two weeks of April, the latest week tracking a monthly decline of 0.5%.

“Non fuel activity rose 0.5% in the March month but is tracking a monthly contraction of 1.1% as at mid-April. While the card data is adjusted for regular seasonal patterns, including Easter, some of the softness in April may be a residual holiday-related drag.

“The softening in non-fuel card activity continues to mainly centre on international spend (some of which may be due to cancelled overseas travel) and discretionary services (particularly accommodation and recreational services) but is starting to become more apparent in discretionary goods as well, particularly housing-related categories.

“The slowing continues to be broad-based, reflecting the common drivers around both fuel and non fuel spend. Overall, the 1.2%qtr rise in card activity in the March quarter is likely to be flat or down slightly once adjusted for price effects.

“The Q1 CPI, due April 29, will give a better sense of how activity has tracked in real, inflation-adjusted terms. Note that the total spending measures in the Q1 national accounts (due June 3) will be somewhat firmer due to effects from the roll-off electricity rebates.”

S&P 500 at record highs despite Middle East uncertainty

Here’s the take of Kyle Rodda from capital.com about the overnight moves on the US market:

- Wall Street climbs despite oil rally, crude prices gap lower at Asian open

- Global markets approach the weekend on a cautiously optimistic note

The “war trades” are breaking down somewhat as the strong correlation between oil prices and everything else weakens.

That’s indicative of a less volatile market, which is of course indicative of less uncertainty, with equities trading with an air of confidence that geopolitical risk is diminishing.

The ceasefire between Iran, Israel and the US continues to hold and even broaden, with the contentious issue of whether Lebanon falls within the agreement settled by a deal overnight for a 10-day detente.

Crude prices rebounded overnight despite this, with oil flows still suffocated by the US’s meta blockade of the Strait of Hormuz.

Gold and the currency complex moved accordingly. However, the positive headline risk pushed Wall Street to fresh highs as investors take a punt that the war is over, and the resulting energy crisis will soon be resolved.

The week ahead

The mooted deadline to the US-Iran ceasefire elapses mid-week. Meanwhile, Tesla is the first cab (or Robotaxi) off the rank for this quarter’s earnings amongst the Magnificent Seven cohort.

Can the two biggest insurers in WA merge?

The competition watchdog has taken its investigation of a possible merger between insurer IAG and RACI (owned by the Royal Automobile Club of Western Australia or RAC) to the next level — a Phase 2 assessment.

Here’s ACCC Chair Gina Cass-Gottlieb:

“This acquisition would combine two of the biggest insurers in WA.

“RACI is WA’s market leader both in motor vehicle insurance and in home and contents insurance.

“We consider the acquisition could substantially lessen competition in both the supply of motor vehicle insurance and the supply of home and contents insurance in Western Australia.”

The ACCC says it is also considering the impact of the acquisition in relation to smash repair services.

It “has not reached a conclusion on the issues and will continue to consider the acquisition” during the next phase of testing it.

Zip Co rockets on profit announcement

Shares in digital payments company Zip Co have soared 14% in early trading.

Financial results for the third quarter of the 2026 financial year show upgraded guidance, with cash earnings (before tax, depreciation and amortisation) at $65.1 million, up 41% from the same period a year earlier.

Its revenue margin fell and bad debts rose, but it expanded its operating margin to 19.4% (up from 16.5%) and grew transaction volumes too.

ASX 200 opens marginally lower

The flagship ASX 200 index that tracks the value of the largest 200 listed companies in the country is down -0.15% on opening, shedding 16 points to 8,938 points.

ICYMI: Aussie dollar at 4-year-high

I usually only cover currency movements when I’m doing the 7pm finance report, and it generally makes my eyes roll as I think:

“I’m never going to be able to go on an overseas holiday again”.

But David Taylor’s read on the dollar has some interesting notes about where our money is headed, relative to our key trading partners.

Read it here:

Defence spending heading to 3% of GDP

The government has announced it’ll be spending an extra $53 billion on defence over the next decade, bringing total spending to 3 per cent of gross domestic product (GDP).

Loading…

Top interview last night with Strategic Analysis Australia head of research Marcus Hellyer, who says that, despite the announced increase in funding, it’s not enough and “defence will need to do some, quote, reprioritisation … and that’s basically bureaucratic speak for some things will be cut or some things will be cancelled.”

He says some Australian companies could be impacted by cuts, but there is a lot of talent in Australia.

He advocates investing more in autonomous systems, “the so-called small, the smart and the many, those things that we’re seeing on every battlefield around the world at the moment … Australia has companies that are world leaders in many of those systems and it’s been one of the big mysteries of the defence budget over the last few years that we haven’t invested in those companies.”

He says that’s changing: “To my mind, again, it’s way too slow.”

Twiggy’s Meta battle rolls on

Billionaire Andrew “Twiggy” Forrest is in court in the US, taking on one of the biggest companies in the world, Meta.

He says the Facebook owner hasn’t done enough to stop scam ads that use his likeness to dupe people into crypto scams.

Here’s an update on the case.

Sneaker company becomes AI infrastructure company

Hold on, didn’t that happen yesterday?

Yes. But in case you missed it, Allbirds will become NewBird AI and move seamlessly from being a sneaker company to an artificial intelligence company.

This is not a joke, although it kind of is.

This explainer article from the BBC is worth a read, in the latest cycle of AI hype, because I think we might be able to look back on it as a marker when things got weird, at best.

Note: I have also started an AI infrastructure company. I have no expertise in the field or concrete plans. Please DM me for my bank details.