Market snapshot

- ASX 200: +0.9% to 8,741 points (live values below)

- ASX 200 (Thursday): -0.2% to 8,666 points

- Australian dollar: flat at 71.96 US cents

- Wall Street: S&P500 +1.0%, Dow +1.6%, Nasdaq +1.0%

- Europe: Dax +1.4%, FTSE +1.6%, Eurostoxx 600 +1.1%

- Spot gold: flat at $US4,622/ounce

- Oil: Brent futures +0.9% to $US111.40/barrel, WTI futures +0.5% to $U105.59/barrel

- Iron ore (Thursday): +0.7% to $US107.80/tonne

- Copper (LME): -0.4% to $US12,989/tonne

- Bitcoin: flat at $US76,457

Prices current at around 10:15am AEST

Live updates on the major ASX indices:

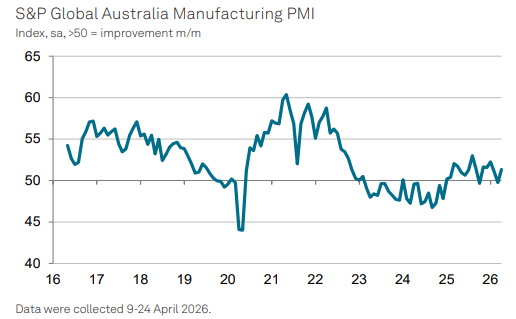

Australian factories hit by severe price and supply disruption

The latest measure of the pulse of Australia’s heartland shows severe price and supply disruptions in April due to the war in the Middle East.

The S&P Global Purchasing Managers’ Index notes that while manufacturing activity expanded in April after March’s contraction, pressures were mounting.

Seasonally adjusted, the PMI moved back above the 50.0 no-change mark in April, posting 51.3 from a reading of 49.8 in March.

However, S&P Global noted the above-50.0 reading for the headline PMI was largely due to a substantial lengthening of suppliers’ delivery times.

Longer lead times are typically associated with pressure on capacity due to improving demand, rather than supply problems.

Input costs increased at the fastest pace in over four years, and there were sustained reductions in output and new orders.

“After March, PMI data had highlighted the initial impacts of the war in the Middle East on the Australian manufacturing sector, the April figures highlight an intensification in those effects,” S&P Global economics director Andrew Harker said.

“The price and availability of fuel is of particular concern, with disruption to supplies feeding through to much more pronounced input cost increases and supply-chain delays compared to March.

“Sharply rising prices and supply disruption also impacted new orders and production, while a number of firms made efforts to build safety stocks by securing materials whenever possible ahead of further cost rises.

“This led to a first increase in stocks of inputs in seven months.”

The flow-on price impacts from the oil crisis are just beginning

While surging fuel prices spiked inflation higher in March, the RBA’s preferred trimmed mean measure of “core” inflation remained stable.

However, it won’t stay that way from April onwards as companies start passing on the higher cost of materials, transport and packaging being driven by the war in the Middle East.

Alan Kohler and Carrington Clarke break down the trends and examine the outlook in the latest Fuelcast.

ASX opens 0.9% higher

The ASX 200 has opened a solid, if slightly disappointing, 0.9% higher at 8,740 points (at 10am AEST).

The broader All Ordinaries is also up 0.9% to 8,966 points.

Futures trading had prices in a 1.5% gain today.

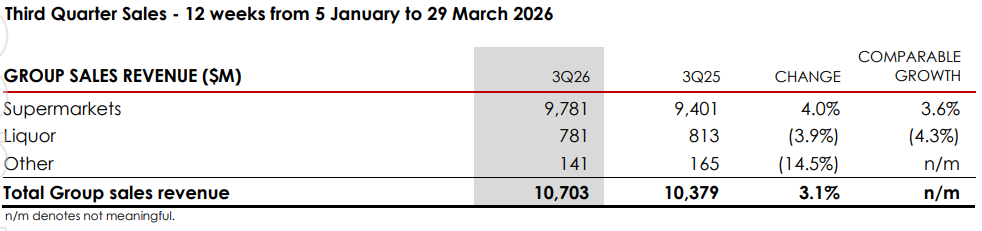

Coles sales rise

Coles posted a 3.1% rise in its third-quarter revenue, as loyalty programs and discounts drove a modest sales growth at its supermarkets.

Supermarket sales revenue grew 4% to $9.78 billion during the period, as targeted weekly promotions and expanded low-cost ranges attracted shoppers.

Yesterday, its big supermarket rival, Woolworths, posted a 4.5% increase in sales but was hit by a series of broker downgrades for its troubles.

E-commerce sales for the segment also grew 24.8% to A$1.33 billion during the quarter.

Coles reported total group sales revenue of $10.70 billion for the three months to the end of March.

That was in line with consensus expectations but down compared with A$10.38 billion a year ago.

RBC analyst Michael Toner said the result was modestly ahead of his expectations despite liquor sales being “very soft.”

“Sales trends for supermarkets appear to have continued early into the 4Q, which is positive as we anticipate a narrowing of Woolworth’s market share outperformance versus Coles heading into the 4Q,” Mr Toner wrote in a note to clients.

“No explicit downgrade to earnings outlook relative to consensus is a positive.”

Aussie dollar pushes through 72 US cents

The Australian dollar, supported by a weakening Greenback and expectations of a rate hike next week, has pushed through the 72 US cents mark, its highest level since May 2022.

The Aussie dollar also rose by around 40 bps against the Euro to be trading near 0.6140 after the ECB left rates on hold overnight.

The US dollar fell around 0.9% against a basket of major currencies.

“AUD/USD was supported by stronger US and European equities and the lower USD,” CBA’s markets team wrote in a morning note.

“The next important domestic event for AUD/USD is next Tuesday’s Reserve Bank of Australia (RBA) interest rate announcement.

“Our Aussie economics team expect a 25bp hike next week. Markets are currently pricing around a 75% chance of a hike.”

Qantas extends cuts in flight schedule through to 2027

Qantas and Jetstar have extended the cuts and other changes to their flight schedules through to 2027 beyond the original cuts planned between July and September.

In a statement to the ASX, Qantas said the action was taken “to mitigate the impact of the conflict in the Middle East, including sustained high fuel costs and to respond to continued strong demand for travel to Europe”.

The previous cuts to domestic services reduced the Qantas/Jetstar group’s capacity by around 5 percentage points.

Qantas has redeployed aircraft to provide more flights between Australia and Europe, providing an additional 2,000 seats to and from Europe per week.

US GDP Q1 growth rebounds after shutdown, inflation on the march

US economic growth rebounded in the first quarter, supported by government spending that had been throttled by the extended federal government shutdown.

However, economists note that the increase is likely temporary as the war with Iran drives up gasoline prices and squeezes household budgets.

Rising energy prices are fuelling inflation after the latest Personal Consumption Expenditure figures, the Fed’s preferred measure of inflation, rose 0.3% in March, or 3.5% over the year, lifting the annual rate further above the Fed’s target even as wage growth continues to ease.

On figures released overnight from the Commerce Department’s Bureau of Economic Analysis, gross domestic product (GDP) increased at a 2.0% annualised rate in the three months to the end of March.

While a solid jump, it was below the consensus estimate for a 2.3% rise.

In the October–December quarter, economic growth slowed to a 0.5% pace as a contraction in federal government outlays lopped off 1.2 percentage points.

NAB’s Head of Rates Strategy, Ken Crompton, said the rebound in federal spending as shutdown effects unwound was a major support.

“Nevertheless, consumption growth has roughly halved since mid-2025 as real household incomes stagnate and the saving rate falls.”

However, there was more positive news in data showing US business investment grew by 10% over the year, driven by a 17% surge in equipment spending and a 13% rise in intellectual property products spending.

“Strength across these two categories mostly reflect the rapid rollout of AI-related infrastructure and models, with information processing equipment alone adding 0.8% points to first-quarter GDP growth and software a further 0.5% points,” Capital Economics North American Economist Thomas Ryan said.

“Much of the demand for AI-related goods is being met from abroad, explaining the 1.3% point drag from net trade, while inventory building made a modest positive contribution.”

The US economy’s growth pace likely supports financial market expectations that the Federal Reserve will hold interest rates steady, possibly into 2027, as long as there is no deterioration in the labour market.

On Wednesday, the Fed left its benchmark overnight interest rate in the 3.50%–3.75% range, noting rising concerns about inflation.

“Core inflation is moving in the wrong direction as far as the Fed is concerned, helping to explain why some regional bank presidents want the FOMC to drop its easing bias,” Mr Ryan said.

“We expect the Fed to remain on hold this year, in line with current money market pricing.”

Atlas Aretia tells shareholders to take no action on IFM takeover bid

The board of the ASX-listed toll road operator Atlas Arteria has told its investors to take no action on the $6.9 billion takeover bid from the big supernation backer, IFM.

The board said it did not solicit the offer and IFM did not give it any advance notice of it.

IFM owns around 35% of Atlas Arteria and has two representatives on its board.

Atlas Arteria says the $4.75 cash per security offer represents less than a 10% premium to the last closing price before the bid was launched.

“The offer is subject to many conditions, including conditions which involve third party consents, approvals or waivers,” the board said.

Atlas Arteria says it will send out a “Target’s Statement” to investors, but in the meantime, it has established an Independent Board Committee to assess the bid.

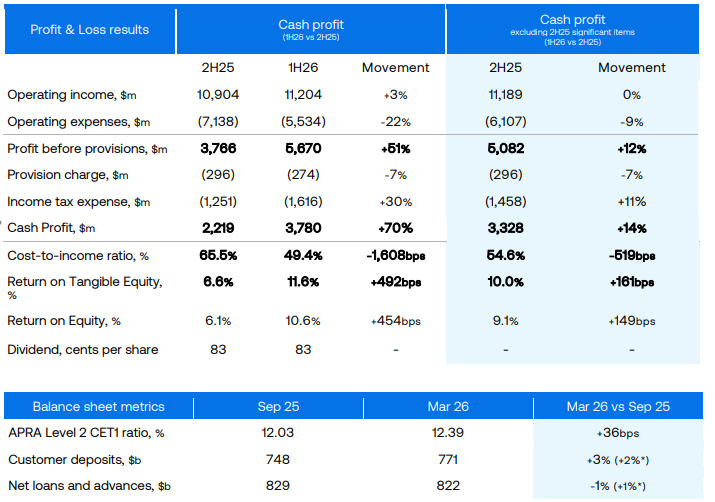

ANZ CEO says impact of the war has so far been “minimal” on the bank

ANZ CEO Nuno Matos says the bank’s solid first half result shows the transformation plans are running at pace and the bank is well positioned to deal with the challenges ahead.

“The impact of the current crisis on ANZ’s credit, capital and liquidity has been minimal to date,” Mr Matos said.

“Much of the potential impact of this crisis remains ahead of us, but the longer the flow of oil is constrained, the greater the chance the crisis shifts from primarily an inflation challenge to much more a supply and growth challenge.”

Mr Matos says, so far, the bank has not seen a material change to the overall borrowing behaviour of customers.

“We have not seen any material increase in new customers entering hardship or receiving assistance.

“However, the situation remains dynamic, and we are prepared for a range of outcomes.

“Reflecting this raised risk in the external environment, we have increased our collective provisions, with our coverage up 4 basis points.”

ANZ H1 profit jumps to $3.65 billion

ANZ has posted a big jump in first half statutory net profit to $3.65 billion after slashing its operating costs.

In cash earnings, the bank’s preferred metric, first half profit hit $3.78 billion.

That’s a 70% jump in cash earnings in the second half of 2025 and 14% higher than the prior corresponding period.

The bank slashed operating expenses by 22% from $7.1 billion to $5.5 billion.

Provision charges fell 7% over the period, despite earlier warnings of potentially softer credit quality.

The interim dividend stayed parked at 83 cents per share.

Wall Street hits fresh highs despite Meta’s tumble, ASX set to rebound

Wall Street’s three key indices all made solid gains overnight with both the S&P 500 and Nasdaq hitting fresh record highs.

- Dow: 1.6%

- S&P 500: 1.0%

- Nasdaq: 1.0%

Despite the war and surging energy costs, April saw the S&P 500 record its biggest monthly percentage gain since November 2020, while the Nasdaq’s monthly gain was its largest since April 2020.

The Dow’s monthly advance was its biggest since November 2024.

There were mixed results among the so-called Magnificent Seven stocks reporting overnight.

Apple jumped 10% after its post-close Q1 earnings beat market expectations. Amazon rose 0.8%.

Meta and Microsoft slid 8.7% and 3.9%, respectively, on concerns over artificial intelligence-related expenditures.

However, the big winner of the session was from the old-school industrial sector with construction equipment maker Caterpillar up 9.9%.

Drugmaker Eli Lily gained 9.8% after upgrading its earnings forecast for a weight loss drug.

European markets also enjoyed a solid bounce (Eurostoxx 600 +1.1%) after the ECB kept rates on hold.

The positive mood looks likely to flow through to the ASX with futures trading at 6:30am AEST pointing to a 1.5% gain on opening.

In commodity markets, oil futures slumped after hitting four-year highs.

Global oil benchmark Brent crude futures rose as high as $US126.41 a barrel, the peak since March 9, 2022, but settled down $US4.02, or 3.4%, to $US114.01.

“It’s massive movements, like intraday movements, as much as we usually have in months,” SEB Research analyst Ole Hvalbye told Reuters.

“It’s a mess… it’s very difficult to calculate and try to make up some fundamental view on this.”

“The market is realizing there might have been a bit of an overreaction yesterday,” senior analyst with Price Futures Group Phil Flynn said, noting that hedge funds were selling positions to lock in gains at the end of the month.

Others noted the retreat in US dollar strength on Thursday also put downward pressure on oil.

That weakness in the Greenback saw the Aussie dollar jump 1.5% to be trading at around 72 US cents.

Gold also benefited from the US dollar weakness to be up almost 2% to $US 4,622/ounce.

With Reuters

Market snapshot

- ASX 200 futures: +1.5% to 8,801 points

- ASX 200 (Thursday): -0.2% to 8,666 points

- Australian dollar: +1.2% to 71.98 US cents

- Wall Street: S&P500 +1.0%, Dow +1.6%, Nasdaq +1.0%

- Europe: Dax +1.4%, FTSE +1.6%, Eurostoxx 600 +1.1%

- Spot gold: +1.7% to $US4,616/ounce

- Oil: Brent futures -3.3% to $US114.09/barrel, WTI futures -1.1% to $U105.70/barrel

- Iron ore (Thursday): +0.7% to $US107.80/tonne

- Copper (LME): -0.4% to $US12,989/tonne

- Bitcoin: +1.0% at $US76,445

Prices current at around 7:00am AEST

Good morning

Good morning and welcome to another day on the ABC markets and finance blog.

Stephen Letts from ABC business team limbering up for a blow-by-blow coverage of the day’s events, where every post is hopefully a winner, but none should be construed as financial advice.

It’s been a busy night with more record closes on Wall Street despite megacaps Meta and Microsoft being crunched on their earnings updates

In short, the ASX is priced for a solid rally after sliding for seven consecutive sessions.

ASX 200 futures (at 6:30am AEST) are pointing to a gain of 1.5% on opening.

We’ll get ANZ‘s first half results shortly.

The big banks have all been raising bad debt provisions in recent weeks as it becomes clear that the US-Iran war is likely to drag on, driving up inflation and choking supply chains.

The ANZ result will give investors the first detailed insights into what this means for the “big bank” profits in the medium term.

Brokers are tipping cash earnings of around $7.3 billion.

S&P Global will also release its Purchasing Managers’ Index (PMI) reading for April.

The monthly house price data has just landed showing growth is slowing nationally, while house prices in the biggest markets of Sydney and Melbourne fell in April.

As always, the game’s afoot, so let’s get blogging.

Loading