Driven Brands currently trades at $13.57 per share and has shown little upside over the past six months, posting a small loss of 4.8%. The stock also fell short of the S&P 500’s 4.1% gain during that period.

Is now the time to buy Driven Brands, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Driven Brands Not Exciting?

We don’t have much confidence in Driven Brands. Here are three reasons why DRVN doesn’t excite us and a stock we’d rather own.

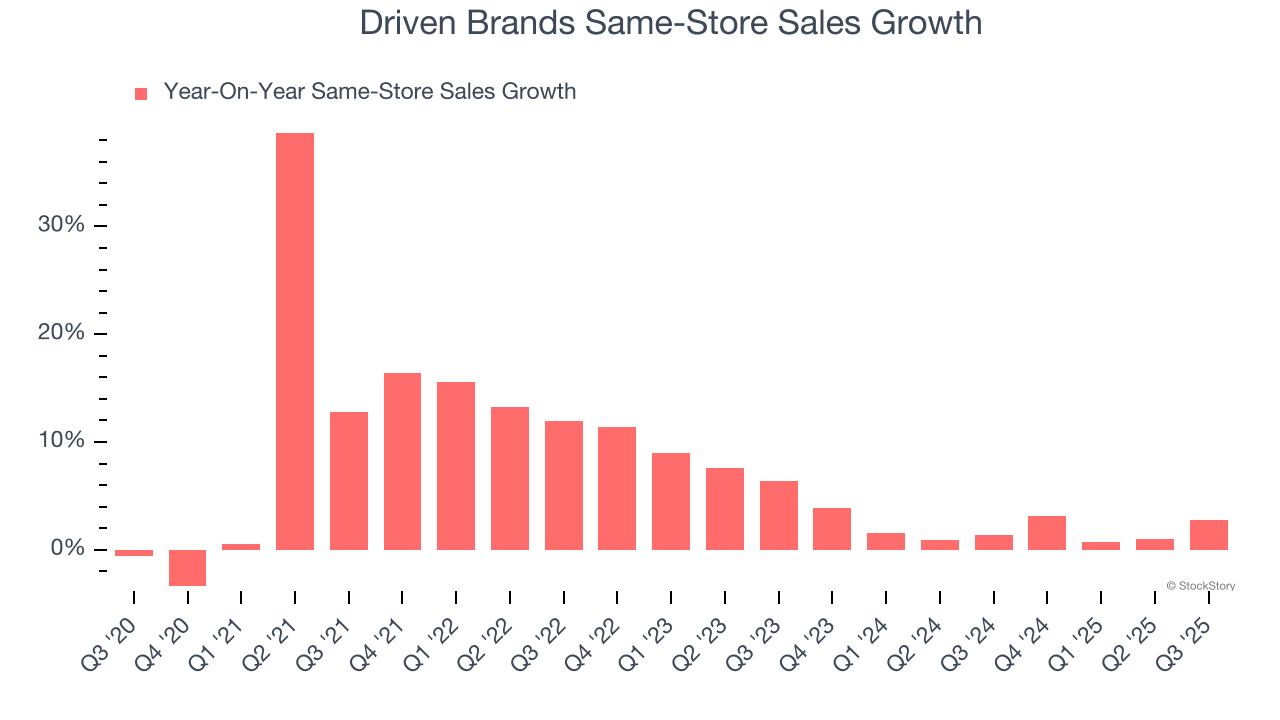

1. Same-Store Sales Falling Behind Peers

We can better understand Industrial & Environmental Services companies by analyzing their same-store sales. This metric measures the change in sales at brick-and-mortar locations that have existed for at least a year, giving visibility into Driven Brands’s underlying demand characteristics.

Over the last two years, Driven Brands’s same-store sales averaged 1.9% year-on-year growth. This performance was underwhelming and suggests it might have to change its strategy or pricing, which can disrupt operations.

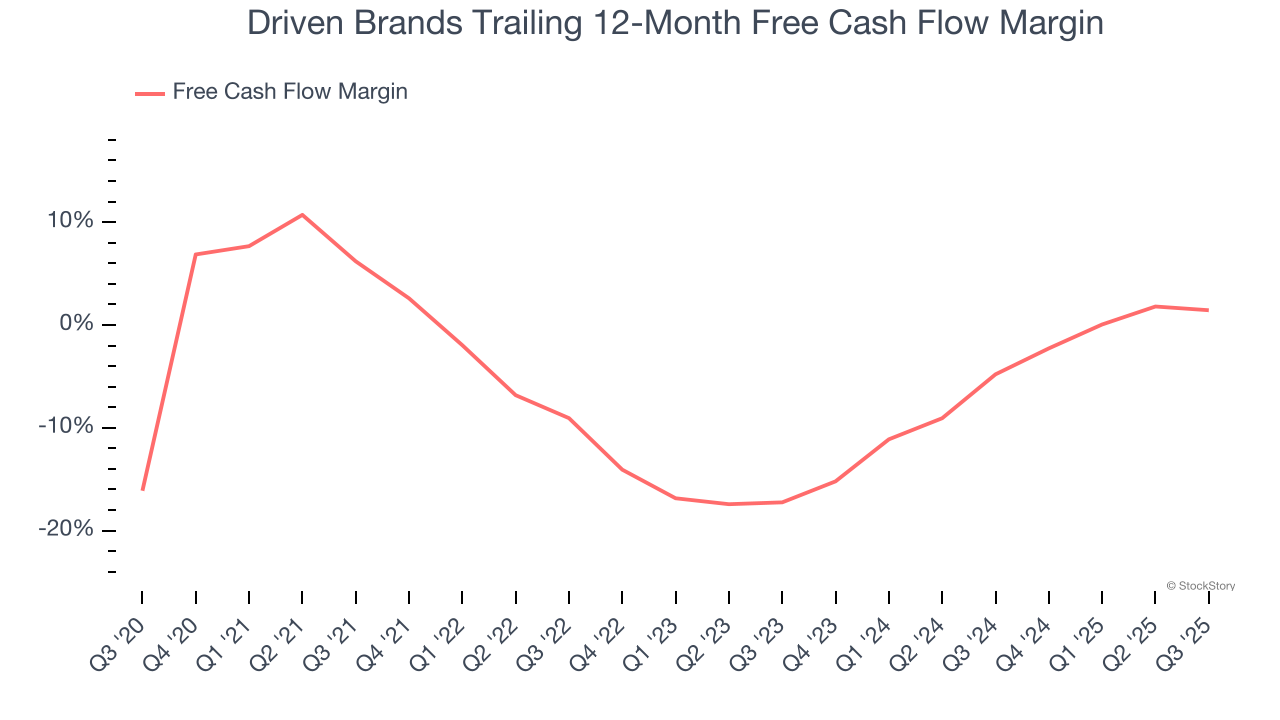

2. Cash Burn Ignites Concerns

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Driven Brands posted positive free cash flow this quarter, the broader story hasn’t been so clean. Driven Brands’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 5.6%, meaning it lit $5.62 of cash on fire for every $100 in revenue. This is a stark contrast from its adjusted operating margin, and its investments in working capital/capital expenditures are the primary culprit.

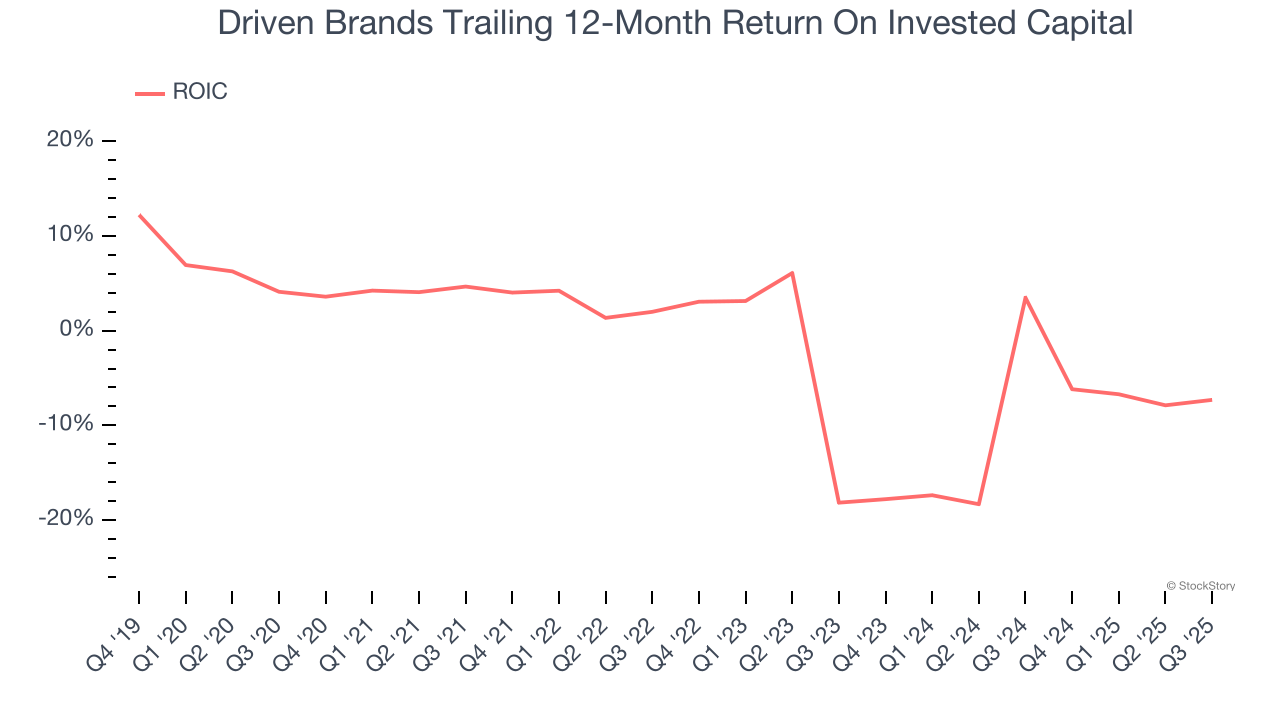

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Driven Brands’s five-year average ROIC was negative 3.1%, meaning management lost money while trying to expand the business. Its returns were among the worst in the business services sector.

Final Judgment

Driven Brands isn’t a terrible business, but it doesn’t pass our bar. With its shares trailing the market in recent months, the stock trades at 11× forward P/E (or $13.57 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We’re pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week – FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.