Lots in the news, as usual. The big event was the liquidation of Spirit Airlines, which shows that pressure from the Iran war is going to rearrange our weak institutions. I wrote about that yesterday. Lots of other stuff is happening, a slew of big mergers, Amazon got sanctioned by a judge for destroying evidence, and the Michigan Attorney General is going after private equity in youth sports.

But before getting to the whole round-up, I want to make a few observations on why I think the stock market is being manipulated. I had an interesting conversation with a Wall Street analyst, and he pointed out something unsettling. This week, four of the most important companies in the stock market – Google Meta, Amazon, and Microsoft released earnings. All four companies delivered their numbers not just on the same day, but, as Bloomberg noted, “within the span of two minutes.” That, my contact said, is very weird.

Here’s why. Wall Street analysts are given responsibility by sector, so one analyst at a bank will look at all telecom companies, a different one will look at all trucking and rail, a third will examine AI/big tech, and so forth. The same analyst or team responsible for understanding Microsoft is often also responsible for Meta, Amazon, and Google. And there is simply no way he or she can analyze four earnings releases on the same day, let alone at the same time. And yet they still have to tell their clients what those earnings mean.

The net result is that these analysts have to take what the companies say at face value, without more analysis. The investment narrative is thus more easily controlled by big tech. Within a few days, the smarter players have figured out what the results mean, but by then the conventional wisdom in the markets are set.

Now, there are endless back-scratching relationships between the big banks and the big tech firms, and these analysts are in general super friendly to big tech. So it is unnerving how big tech still feels the need to confuse even their closest allies.

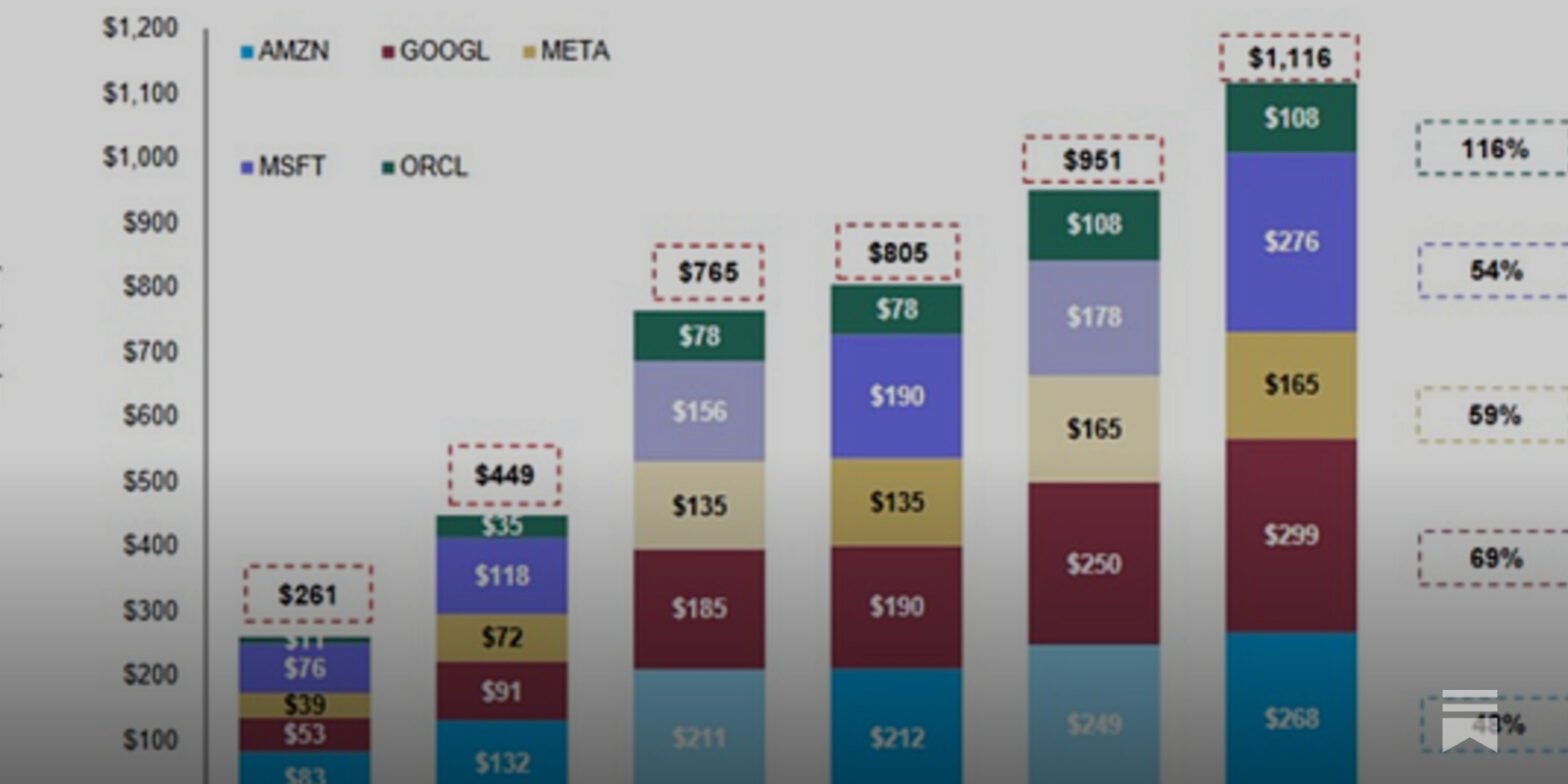

Anyway, what happened this time on earnings? Well the big tech hyperscalers all said they are going to spend a kajillion quintillion dollars on data centers, and their free cash flow is virtually gone. Morgan Stanley is projecting $1.1 trillion of capital investment from the big four, plus Oracle. (Larry Ellison says “hey guys wait up!”)

As Jordan Terry noted, “They can’t deploy that much capital, we don’t have the infrastructure to support it, does nobody check these things?” No, no they don’t.

I’m increasingly skeptical that all of this compute is even necessary. As AI scientist Gary Marcus notes, there are fundamental limits on how much scale can really do for reasoning, though scale is what finance is good at. I heard Marcus speak a few weeks ago, and I was impressed. But I don’t know AI technology except on a superficial level. The reason I trust Marcus is because he put his money where his mouth is; he tried to bet $1 million with Elon Musk that Musk’s projection AI would be smarter than humans by 2025 would be wrong. Musk didn’t respond.

What clinched my view that compute is being oversold, though, are some comments by Nvidia CEO Jensen Huang. One of Nvidia’s partners, Anthropic, has a really nifty new AI model, Mythos, that scared all the big important financial people because of how powerful it is. Well, Huang was asked on a the Dwarkesh podcast why he wants to export chips to China, considering China could build something as powerful as Mythos and potentially threaten America. His response was as follows:

First of all, Mythos was trained on fairly mundane capacity, and a fairly mundane amount of it. By an extraordinary company. The amount of capacity and the type of compute it was trained on is abundantly available in China.

Leave aside the China geopolitics, think about what Huang is saying. The best model out there was trained on “fairly mundane capacity.” So what, exactly, is all this compute really for? I mean, even the Pentagon is saying that companies are often using Chinese open source models, so it’s clear the giant compute advantage the U.S. has isn’t translating into performance.

One possible answer is that these companies are not actually selling AI, they are selling tokens, aka cloud computing. So the more inefficient their model, the more revenue they get from corporate America buying their cloud computing. It’s a bit like oil companies making cars – of course they want to make gas guzzlers, not Honda Civics. And once American companies are locked into one AI system, it’s hard to move to something cheaper and more efficient. I don’t know if that’s true, but the one big spender on data centers that doesn’t have a cloud computing arm – Meta – was punished by the market.

There’s other stuff that feels really sketchy. For instance: “The S&P 500 is removing long-standing profitability requirements — the ‘enshittification’ of the index. This change potentially turns the index into a ‘dumping ground’ for Private Equity to offload unprofitable, highly leveraged companies onto retail index investors.”

And that’s not even speaking to the weakening consumer spending numbers, and oh yeah, the war in Iran spreading an energy shock worldwide, that is going unaccounted for by the markets. Anyway, a lot of people are feeling unsettled. Count me as one of them.

And now, the rest of the monopoly round-up. Some fun stories. Amazon got sanctioned by a judge because Jeff Bezos was destroying documents, Apple took a stinging loss, oil giants refuse to drill for oil because they prefer cash flow, and economic data is coming out uglier and uglier. Read on for more.