Lots happened in terms of monopoly news this week, as usual. Household income is now officially declining, California’s assembly is scaring big law firms by passing a major antitrust bill, and there is a merger of two firms most of us haven’t heard of – CoStar and Zonda – who organize how real estate is priced and managed.

Before getting to that, I’d like to touch on two important shifts happening in the world of big tech and AI. Both are a function of the gruesome stock market rise we’re all watching, with the S&P and Dow Jones at record highs, even as the real income of Americans decline.

I’m writing about this situation for two reasons. The first is that Elon Musk’s company SpaceX is going public, in what looks like a case of market rigging. Surprisingly, AI is a big part of the story for that stock. And the second is corporate America is finally starting to see bills for the AI they are using, and they aren’t liking it. On this latter point, I got into a debate with Bloomberg’s Joe Weisenthal about how inefficient American AI firms really are, and it led us to a useful back-and-forth.

The subtext is that much of the increase in equity valuations, and thus our social hierarchy, is a result of the techno-optimism embedded in AI. And it does seem like a lot of Wall Street is desperately hoping there isn’t a bubble. Here are ‘strategists’ at major investment banks saying as much:

“Are there pockets of excess? Yes. There is crowding going on. We can get 15-20 per cent correction in individual stocks,” said Mike Wilson, chief US equity strategist at Morgan Stanley, adding: “There will be frothiness and then correction, but the market can keep marching forward.”

Ben Snider, chief US equity strategist at Goldman, added that “conditions that typically mark the end of bull markets” — such as “speculative mania, contracting profit margins” or Federal Reserve rate rises — are “absent”. “And that fuels my expectation that the recent market rally will continue.”

No one knows when a bubble pops, but I do think there are signs we’re in one.

We’ll start with Elon Musk’s company SpaceX, which in terms of what it does as a corporation, is extremely cool. Most tech firms are software driven or do some variant of advertising, largely because Wall Street doesn’t let them invest in anything real. SpaceX does something important and expensive. It sends stuff to low earth orbit.

And that’s because Musk is a unique figure, able to leverage Wall Street capital to actually bend metal, a sort of huckster who hires and respects engineers. Much of his wealth is a result of the fact that in the 2010s, somehow he cobbled together the capital to do something no one had done since the 1920s, which is to create a new U.S. car company, Tesla. He did the same thing for SpaceX, whose inexpensive satellite launch services have allowed all sorts of companies to send payloads into space.

SpaceX is a monopoly in this area, and while it pursues unfair business tactics to maintain that position, largely it is dominant because of operational skill. It has also leveraged its position in launch to send up thousands of satellites and create a communications network called Starlink, which provides high-speed data communications worldwide. It’s hard to overstate the importance of this system. The war in Ukraine runs on Starlink; it matters so much in terms of national security that Steve Bannon once called for it to be nationalized.

But just as SpaceX the company represents Musk the engineer, SpaceX the stock represents Musk the financial huckster. It’s so bad that the Financial Times calls the SpaceX IPO the “Enshittification of the Stock Market,” and More Perfect Union published an excellent video called “Did Elon Musk Just Rig the Stock Market?”

Here’s why. SpaceX is a bunch of real assets, but it’s also a holding company where Musk has stashed his less valuable stuff. Twitter is now part of SpaceX. So is xAI, which runs Grok.

Moreover, SpaceX released its financial data publicly so investors could analyze it before deciding to buy shares, and it was underwhelming. The investor documents are “a train wreck,” full of pie in the sky cult-style rhetoric about going to the stars, but the actual numbers show that only one part of the company – Starlink – is profitable. Beyond that, its numbers are just ok. The company lost $4.7 billion last year, its annual revenue rate is $18.7 billion, it is growing only modestly at 15% a year.

There is a lot of hair here. Its biggest revenue driver is not its rocket systems, but its ownership of Nvidia chips that it rents to Anthropic. That’s weird. At best, it is simply an AI commodity provider, no different than anyone else who owns a lot of chips. At worst, well, Michael Burry, the short-seller made famous in The Big Short, traced a complicated financial structure involving Grok taking part in a scheme to keep Nvidia’s AI chip sales numbers off-the-books, similar to Enron or special purpose vehicles during the financial crisis.

That’s not good. Moreover, Musk has also changed corporate governance rules so he is in total control, with no rights for anyone else.

This stuff wouldn’t be bad if SpaceX were a modestly valued company, but Musk thinks he can bring it public at a value of $1.8 trillion. And that’s a crazy valuation for a company with less than $20 billion of revenue that is losing money and growing slowly. So what gives? How can Musk think he’ll be able to get so much for so little?

Well, that’s where the seediness comes in. First, just 5% of shares outstanding will go on sale to the public, meaning that most of the stock will be held by insiders, and the “float” can be manipulated up or down as need be. Second, the company is planning to sell 30% of its floated shares to retail investors, versus 10% for normal IPOs. The reason is that sophisticated investors can see the numbers make no sense, but retail investors love Musk and will buy no matter what.

But most importantly, the NASDAQ stock market just changed its rules around how it organizes its index of important firms, the NASDAQ 100, to allow SpaceX to get in early. Many index funds automatically mimic the Nasdaq-100, which means that NASDAQ is ensuring that huge amounts of investor capital will flow into the company. Virtually every investor in America will end up owning a piece, whether they like it or not. Companies used to have to trade for three months, now it’s just 15 days. And the company had to have at least 10% of its shares publicly trade, but that’s no longer a requirement.

And what that means is that the insiders, the early investors like Google, Marc Andreessen, Peter Thiel, and various Arab sovereign wealth funds, basically Musk’s gang of allies, will be able to dump their shares at a high value on America’s retirement accounts, aka all of us. And they may not care if it crashes later on.

I don’t know if it’s the top of the stock market, but it sure seems like a lot of insiders are betting that it is.

The second reason to think we’re going to see a change is because the bill for using AI in corporate America is finally coming due. And that could potentially slow the screamingly fast revenue increases sustaining the investment boom.

There has been a very obvious unanswered question since 2022. If AI companies are seeing demand explode, and they are losing massive amounts of money on trillions in investment, why don’t they raise prices? Isn’t that what price signals are for?

Over the past few months, the large AI companies have started to make this question less relevant, because they’ve been raising prices. Anthropic et al have limited their sales flat-rate subscriptions and are more assertive about charging by the amount of AI compute, known as “tokens,” a customer uses. Token-based billing started in Q1 2026, which means companies are seeing their first four months of the new regime. And this shift has had significant impacts on enterprise spending; one consultant told Axios of a client that “recently spent half a billion dollars in a single month after failing to put usage limits on Claude licenses for employees.”

As a result, last week, a number of companies, from Uber to Microsoft, announced they are rolling back the amount of tokens they are allowing their employees to buy. Think about it like this: right now, Google searches are free, but imagine if one day, you got a bill charging you for every Google search. Your usage patterns would change. And that’s what’s happening in corporate America. In the last few months. CEOs were happy to have their employees experiment with AI, but no longer.

This shift sounds minor, but it could rewire the economy.

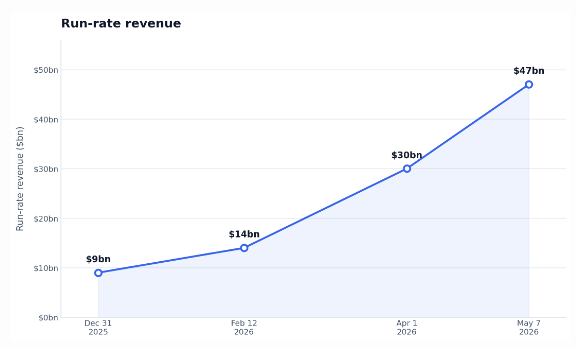

The amount of money we’re talking about is likely significant. The lead in this space, Anthropic, had a revenue rate at the end of 2025 of $9 billion. On Thursday, the company said that its revenue has increased to an annualized rate of $45 billion a year. No company has ever scaled this quickly. Part of what’s going on is there’s more use of its models, but price hikes are also embedded in this story.

And this dramatic upsurge in revenue answers the question of why these companies are willing to lose money – they were attempting to lock-in companies and consumers onto a specific AI stack, raising prices later.

Just as it’s important to distinguish between SpaceX the company and SpaceX the stock, it’s also important to distinguish between AI the technology and AI the financial phenomenon. The technology can clearly do very cool things.

But the marketing campaign during the below-cost pricing era was supremely annoying. There was metaphysical hand-wavey nonsense about eliminating all white collar jobs or creating a higher form of intelligence.

I saw this hype cycle almost every day on CNBC, I saw it in the policy world, I saw it in academia, in consulting firms, on Wall Street, hell, I saw it when Bernie Sanders said he was afraid these companies are creating God. Important validators like OpenAI CEO Sam Altman and Anthropic CEO Dario Amodei were making these hype-filled arguments, calling for a revolution in politics to accommodate AI, and so forth.

But it was a marketing campaign, which was paired with an important set of policy choices. The main thrust of U.S. policy since the beginning of this Trump administration has been boosting a specific compute-heavy AI infrastructure that is closed source and vertically integrated, aided by a hype cycle to justify losses. On Trump’s second day in office, for instance, he did a press conference announcing a $500 billion data center buildout with Softbank and OpenAI.

But the real story was that Google was engaged in below-cost pricing on Gemini to win the consumer AI space, and that Anthropic and OpenAI similarly had huge losses while they sought market power somewhere. These companies figured “we’re losing money like Amazon did,” the losses are real but the opportunity in a few years is massive, as they attach themselves to corporate America and bleed out more profit.

Why make such a big bet? On the podcast Odd Lots, Joe Weisenthal had a theory about big tech. These firms have 30% of the profits in the economy, he muses, they are asking themselves how to get the other 70%. AI was their way to do that. Or so they figured. (Anthropic and OpenAI as part of the big tech world, they are loose proxies for their investors Nvidia/Google/Amazon/Microsoft.)

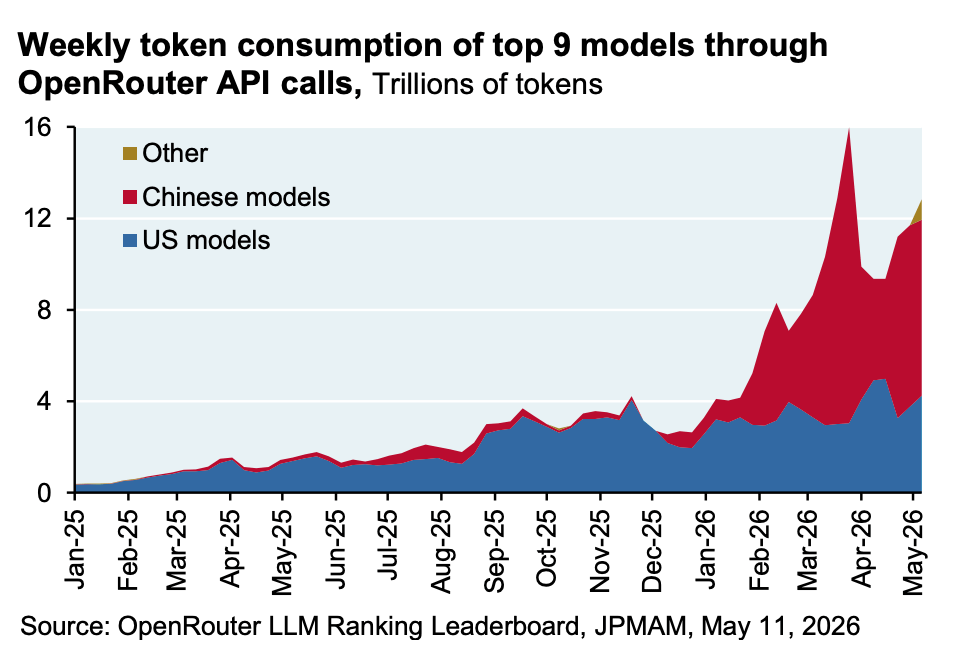

As I noted a few weeks ago, there has always been a nagging problem here, which is that the Chinese open source models have been almost as good as frontier models, which makes no sense unless compute isn’t as important as it’s made out to be. U.S. models have gotten more efficient too, but a key reason is clearly because they have to compete with Chinese models. Here’s J.P. Morgan’s Michael Cembalist making that point, showing that Chinese models are now out-competing American ones, at least by one particular token measurement channel.

Still, the real problem is that the industry was simply not organized around real market signals, it was cross-subsidized by various big tech monopolies in search and social advertising, business software, and cloud computing/ecommerce, plus tax subsidies and Wall Street lending. That’s what was filling the losses, a weird pro-monopoly industrial policy.

What seems to be happening is that pricing is right-sizing, or at least, Anthropic isn’t willing to endlessly underwrite the use of their tools by corporate America. As that happens, and companies start asking if there’s real return on investment in buying tokens, we’re starting to see a broader understanding that AI is just a business method, it isn’t some metaphysical achievement, and it has to be justified as something that creates more value than it costs. And now it turns out the Chinese approach is better for producing everything except market capitalization, as is the case for every other industrial sector.

There are significant questions about how useful the underlying technology really is, but those questions are actually not what matters when it comes to equity values. It’s quite possible the tech is great, but won’t deliver for its investors. Light bulbs have great value, but are super cheap in financial terms because there’s a lot of competition.

And fundamentally, trillions of dollars in data center investment eventually have to be justified with real cash purchases of tools by someone somewhere. Whether AI is useful is a different question from whether those particular data center investments can be justified at current valuations. Anthropic’s insane scaling of revenue is a positive sign for the industry, because it means that companies are buying a lot of AI tokens. But even so, $45 billion is not remotely enough to justify the investments we’ve seen. And it’s quite possible AI is great, but commodified.

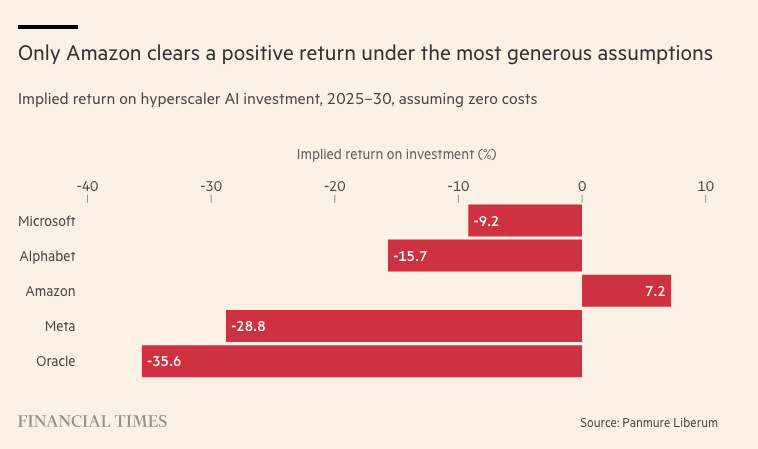

One UK investment banker published his projections in the Financial Times, and found some pretty sanguine outcomes.

As the hype dies down, so will the air cover for why big tech firms are putting trillions into data centers. This money has gone to everyone who makes anything adjacent to data centers, and it has a certain economic consequence. Recently, memory commodity producers Micron, SK Hynix, and Samsung all became worth $1 trillion, joining chipmakers Nvidia and Broadcom. Automaker Ford’s stock recently jumped, because of the possibility that its battery endeavors can be used for data centers. Stocks such as Intel and Dell have been on screaming tears. And of course, there’s SpaceX, as I noted above.

But in a sense, the entire AI narrative is a bit like selling huge amounts of picks and shovels as everyone rushes to the mines, and then betting there will be gold when they all start digging. Much of the stock market is made up of investor speculation that pick and shovel companies are about to hit the motherlode. But we don’t actually know how much gold there is, or even if there is any gold at all. So far, every powerful and rich person has insisted that there’s so much gold we can’t imagine it all, and anyone who thinks otherwise is a Luddite Marxist loser.

But that era, now that companies actually have to pay for tokens, is over. It’s time to pay for the picks and shovels. And if there isn’t an unimaginable amount of real value from end consumers that they are willing to buy in terms of tokens, then the collapse of this entire ecosystem, with its massive overcapacity, will be stunning and quite scary.

Both the SpaceX IPO and the AI repricing are moments where we see the real cost of our corrupted system of law. Securities rules are meant to prevent the kind of predatory activities in which Musk is engaging, not just because they are bad for the weak and disorganized, but because they can crash an entire economic system. The Securities and Exchange Commission was formed after the 1929 crash, for a reason.

Similarly, we used to have rules preventing massive loss-making to acquire market power. If we had a legal regime that forced actual market signals in AI to function, then we would have asked questions about real value years earlier, before sinking trillions into data centers. Instead, we have chosen as a society to prioritize the interests of vertically integrated dominant firms or their proxies, and they right now are betting all of their free cash flow on a particular approach. But it is a bet, it is not a sure thing. And as pricing right-sizes, well, we’ll likely see that it’s a losing bet.

And now, the rest of the monopoly news round-up, with some cool stories. The California state assembly passed a strong antitrust bill, which surprised me. And it could portend much stronger monopolization law going forward. Plus, the Pope goes anti-AI and anti-monopoly, some important mergers in the real estate space, a Delaware judge says that corporations get the right to vote in elections, and the Speaker of the House argues that Congressmen need to supplement their low salaries with insider trading. I mean, why not?

That and more, in our very dumb timeline, after the paywall.