SmartRent has gotten torched over the last six months – since December 2025, its stock price has dropped 38.3% to $1.16 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy SmartRent, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is SmartRent Not Exciting?

Even with the cheaper entry price, we’re swiping left on SmartRent for now. Here are three reasons you should be careful with SMRT, plus one stock we’d rather own.

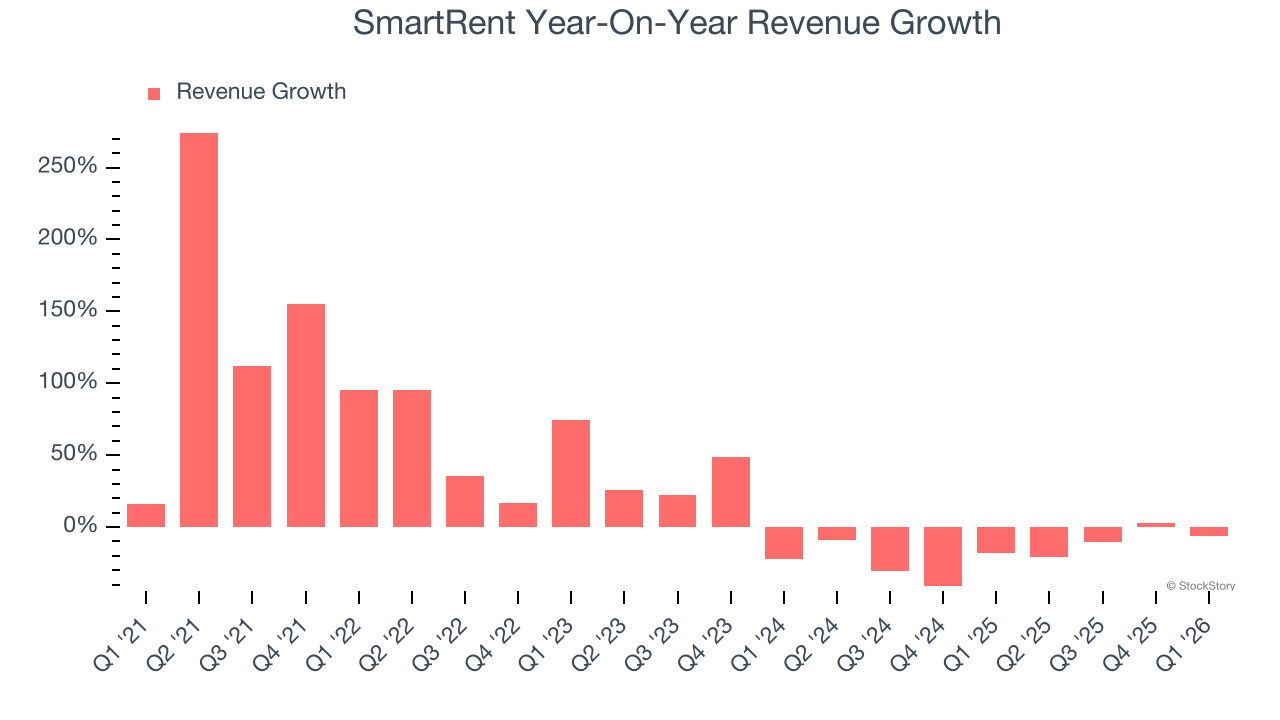

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. SmartRent’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 17.9% over the last two years.

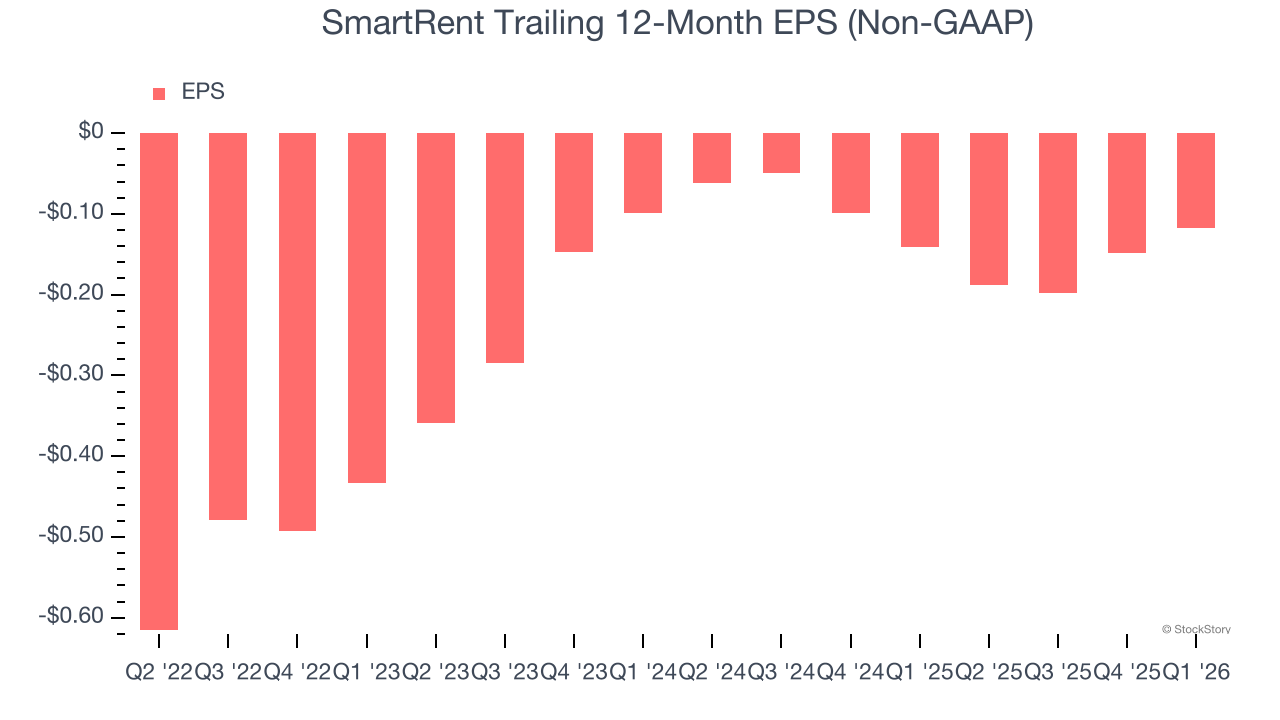

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

For SmartRent, its two-year annual EPS declines of 8.7% mark a reversal from its (seemingly) healthy four-year trend. We hope SmartRent can return to earnings growth in the future.

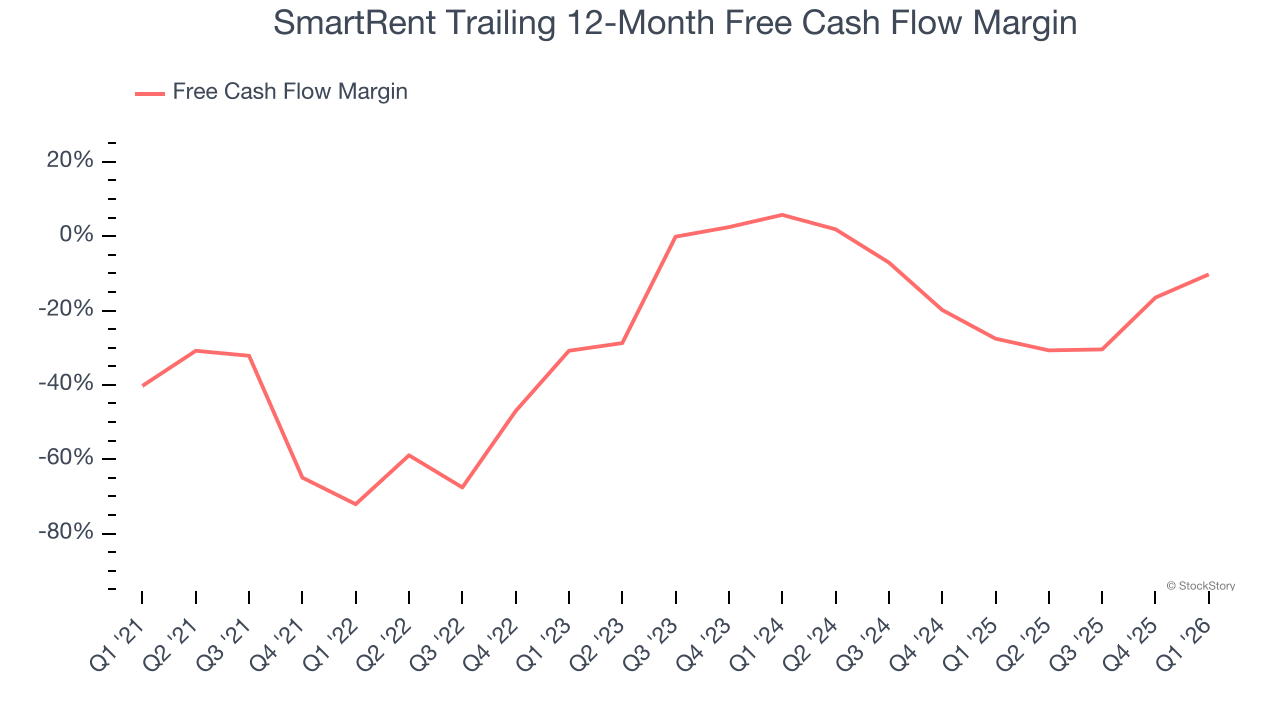

3. Cash Burn Ignites Concerns

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

SmartRent’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 23.4%, meaning it lit $23.36 of cash on fire for every $100 in revenue.

Final Judgment

SmartRent isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at $1.16 per share (or a forward price-to-sales ratio of 1.4×). The market typically values companies like SmartRent based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now – better opportunities lie elsewhere. We’d suggest looking at the most dominant software business in the world.

Stocks We Like More Than SmartRent

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.