The local share market lost ground after returning from a public holiday. NAB economists think the next RBA rate move is down.

Look back on the day’s financial news and insights from our specialist business reporters on our live blog.

Disclaimer: This blog is not intended as investment advice.

Tue 9 Jun 2026 at 4:46pm

Market snapshot

- ASX 200: -0.24% to 8,604 points (close)

- Australian dollar: +0.18% to 70.58 US cents

- Dow Jones: -0.2% to 50,786 points

- S&P 500: +0.3% to 7,405 points

- Nasdaq: +0.9% to 25,929 points

- FTSE: +0.1% to 10,373 points

- EuroStoxx: -0.2% to 621 points

- Spot gold: +0.2% to $US4,337/ounce

- Brent crude: -1.1% at $US93.2/barrel

- Iron ore: +0.65% to $US101.3/tonne

- Bitcoin: -0.18% to $US63,353

Prices current around 4:45pm AEST.

Live updates on the major ASX indices:

Tue 9 Jun 2026 at 5:13pm

Until tomorrow

That’s it for today. Thanks for joining us.

Thanks for sending in your many comments too (and to Phillip for kicking off the discussion).

The ABS will release its monthly building approvals data tomorrow, and its latest data on industrial disputes (which have been insignificant for 20 years).

Until then, take care of yourselves.

Loading

Tue 9 Jun 2026 at 4:59pm

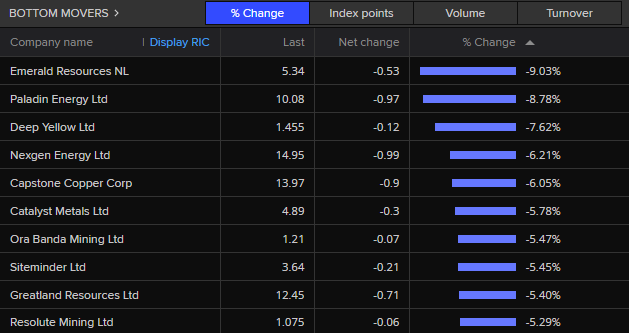

Best and worst performing stocks

Among the top performing stocks on the ASX200 today were Zip Co (up 14 cents, +5.88%, to $2.52), IDP Education (up 10 cents, +5.26%, to $2.1) and Eagers Automotive (up 90 cents, +4.32%, to $21.72).

Among the worst performers were Emerald Resources (down 53 cents, -9.03%, to $5.34), Paladin Energy (down 97 cents, -8.78%, to $10.08), and Nexgen Energy (down 12 cents, -7.62%, to $1.45).

Tue 9 Jun 2026 at 4:53pm

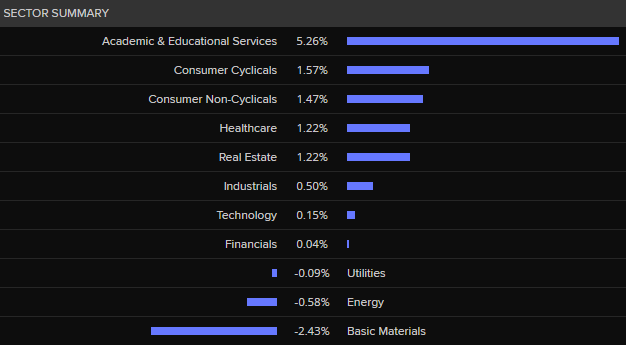

Sector summary

Eight out of eleven sectors gained ground today, but the ASX200 index was weighed down by losses in three sectors: utilities, energy, and basic materials.

Tue 9 Jun 2026 at 4:41pm

ASX sheds 0.24pc

With trading finished for the day, the S&P/ASX200 index has closed 20.9 points lower (-0.24%) to settle on 8,604.2 points.

Tue 9 Jun 2026 at 4:36pm

Barbeques Galore to close more than 60 stores, with hundreds of workers facing redundancy

The rolling story will be published here:

Tue 9 Jun 2026 at 4:26pm

Barbeques Galore to wind up after failing to find buyer

Barbeques Galore will wind up in coming weeks, with hundreds of workers facing redundancy.

The retail chain entered into voluntary administration in February, and today it announced it was unable to find a buyer or complete a recapitalisation.

It will shut its 62 company-owned stores in the coming weeks and work through “transitional arrangements” with 27 stores owned by franchises.

The receivers said staff would continue to be employed “during the receivership process” or made redundant as the winding up occurred.

Barbeques Galore had about 500 staff at the time of its collapse in February.

“All employees will be paid their full accrued redundancies and termination payments in the ordinary course of separation,” the receivers said in a statement.

Tue 9 Jun 2026 at 3:53pm

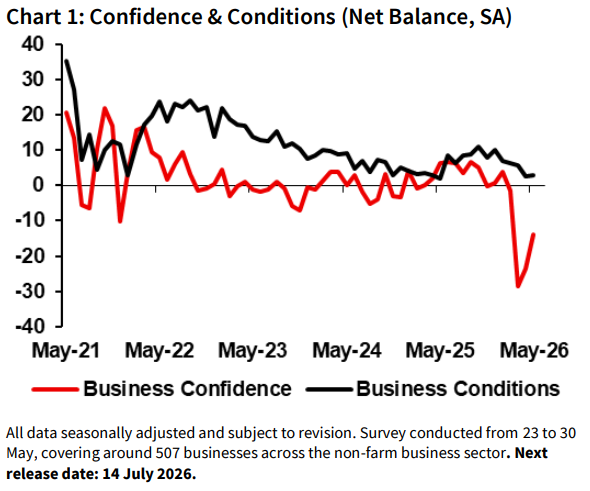

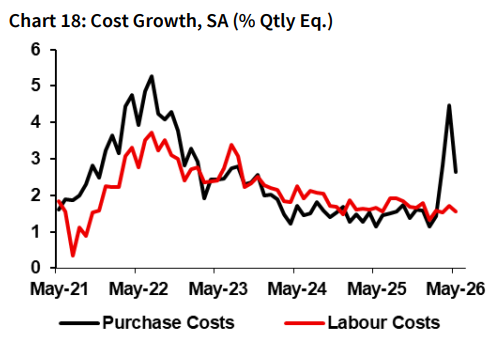

NAB business confidence survey shows confidence still in negative territory

NAB’s monthly business survey shows business confidence rebounded further in May (although it remained deeply in negative territory), and business conditions remained in positive territory.

“Nonetheless, with global uncertainty persisting, the domestic backdrop softening and cost pressures remaining elevated, confidence remains very weak and in negative territory across all industries,” the report says.

The survey was conducted from May 23-30, covering around 507 businesses across the non-farm business sector.

It says business conditions rose in wholesale, finance, property and business services as well as recreation and personal services industries.

Trend conditions were strongest in mining and finance, property & business services while manufacturing was the weakest industry.

It says price and cost growth eased in May but remained elevated – particularly purchase costs which signal the ongoing risks of the cost shock emanating from the Middle East still making its way through supply chains.

Tue 9 Jun 2026 at 3:42pm

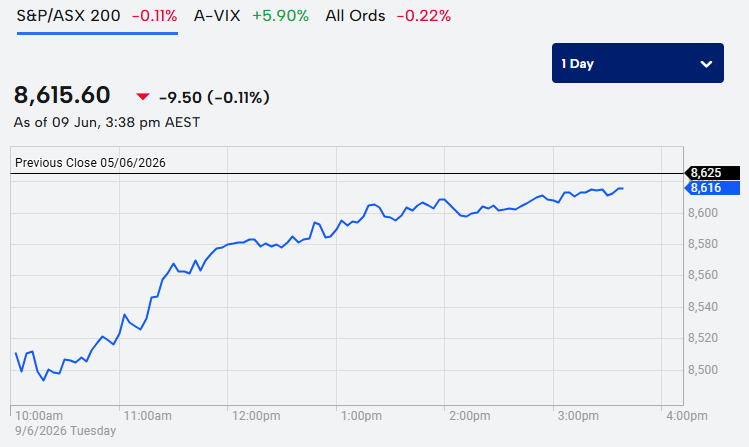

ASX down just 0.1pc

With roughly 20 mins of trading left today, the ASX200 has almost recovered its losses from the opening bell.

The index is now down just 9.5 points (-0.11%), to be sitting at 8,615.6 points.

Tue 9 Jun 2026 at 3:38pm

A case of herding

I’m finding the negative commentary about bank economists interesting – Instead of criticizing them because they are employed by the banks…maybe the better criticism is the predictability of the commentary (ie you don’t need to read they commentary, you know what they are going to say from the piece of data). Leaving aside that most of the exposure I get to the commentary is via what published here…I would to value what they are saying way more if there was more diversity of the view. It seems like for the most part, its a cut a paste with little deviation from the herd. I’d like to see…yes x data pointed this way, but cut happened here and we need to see the affect over there is before Y happens (I studied economics so I know that its a string that once pulled doesn’t end)

– allan

Thanks Allan. That’s getting to a deeper point. They all work with similar economic models, so their views don’t deviate much from each other.

Tue 9 Jun 2026 at 3:33pm

How do jet fuel changes actually affect airfares?

New research from Adelaide University, published in Research in Transportation Economics, takes a look at different types of jet fuel shocks to see what effect they have on airfares in Australia.

It says jet fuel is one of the airline industry’s biggest costs, typically accounting for 25 to 40% of total operating expenses.

It says in Australia, where about 90% of jet fuel is imported, understanding how airfares respond to fuel price shocks is particularly important.

The researchers analysed Australian domestic airfare data from the Bureau of Infrastructure and Transport Research Economics, and they separated jet fuel price shocks into three categories:

- Supply shocks

- Aggregate demand shocks, and

- Jet fuel-specific demand shocks.

And they found something interesting: fuel supply shocks, which can be caused by events such as wars, natural disasters or disrupted supply chains, were found to have little direct impact on domestic ticket prices.

“This was one of the more surprising findings,” said Dr Yifei Cai from Adelaide University’s College of Engineering and Information Technology.

“Many people would expect airlines to immediately pass fuel cost increases on to passengers, but our results suggest airlines can often smooth these effects through fuel hedging, long-term supply contracts and other operational strategies.”

By contrast, they say, aggregate demand shocks, which are usually linked to periods of economic growth, were found to increase business class and restricted economy fares.

“When economic conditions are stronger, travel demand tends to increase, particularly among business travellers,” Professor Zhang said.

“That gives airlines more room to raise prices in these fare classes.”

The third category, jet fuel-specific demand shocks, had more complex effects. These shocks can occur when market participants begin buying or hoarding oil because of fears about future shortages, geopolitical risks or climate-related disruption.

The research found these shocks can reduce business class fares in the short term, as uncertainty dampens corporate travel budgets, while increasing discount fares as more travellers seek cheaper tickets.

“Oil-specific demand shocks are particularly destabilising because they can trigger sharp price increases without corresponding changes in actual supply or global demand,” Dr Cai said.

“Overall, the findings highlight that airfare responses are shaped not only by fuel costs, but also by passenger behaviour and broader macroeconomic conditions.”

Tue 9 Jun 2026 at 3:21pm

The conversation continues

“It is difficult to get a man to understand something when his salary depends upon his not understanding it.” – Upton Sinclair (and variously attributed to other people in various forms).And with regards to the purported independence of a large proportion of people employed today, every HR person, everyone selling alcohol or cigarettes, every quality auditor, every marriage celebrant, all have to convince themselves at some level that they are doing something useful, or that they are accepting money for doing something bad and thus their independence is compromised. And every fund manager who takes two per cent a year for managing money when they know the client might be better off in an ETF or bank account … (No, I cannot claim I have never accepted money to do some job which filled me with such doubts.)

– Bof

Thanks Bof.

Regarding the independence of a large proportion of people employed today, in that sense we’re all a little corrupted.

My favourite Upton Sinclair book is The Brass Check (1919). Highly recommended. It’s about how corrupt the media is.

“American Journalism is a class institution, serving the rich and spurning the poor,” he wrote.

Tue 9 Jun 2026 at 2:46pm

ABC Business Daily now live

Today’s episode of ABC Business Daily is live.

Ian Verrender, the ABC’s chief business correspondent, is the guest on this episode.

Elon Musk’s SpaceX is finally about to go public at the end of this week. Is there any risk behind the sky-high SpaceX hype?

And we’re a week out from the RBA’s next rate decision, but economists at Australia’s big four banks can’t seem to agree on the RBA’s next move. Why?

Tue 9 Jun 2026 at 2:34pm

What’s their focus?

Even if the board has no editorial power over the economist department, surely we can agree they have an incentive not to say things that endanger the bank because no bank=no pay.I think (speculation admittedly) their main role is to reassure borrowers. “It’s all going to be ok darling, just keep paying your mortgage!”

– Jesse

Thanks Jesse. That’s an interesting point. What could they say that would endanger their bank? I guess they could start pumping out research that severely criticised the level of market concentration that Australia’s big banks enjoy?

But their stock-standard economic forecasts for inflation and interest rates etc don’t do that. Those forecasts are based on the regular flow of economic data that contributes to the quarterly National Accounts, the monthly unemployment rate, wages and profit data, the terms of trade, and everything else. They’re focused on aggregate demand, potential output and the output gap, and what it all means for inflation and rates. They’re looking at the world in the same way as the Reserve Bank. That’s their focus.

I guess more broadly, the economics teams wouldn’t want to talk down the economy unnecessarily, given how “confidence” (and animal spirits) is such an important factor in consumer and business psychology. But we also need to have the strength to face the reality of what’s potentially coming, so that we can prepare for tougher times ahead if we need to. So, that’s the fine line they’re trying to walk.

Tue 9 Jun 2026 at 1:57pm

You have been warned

And you’ll never see a bank’s economics team forecast or call a recession until we’re deep in it. They wouldn’t have a job for long if they did.

– Josh

Thanks Josh. That’s not true. This is what Westpac’s economics team wrote last week:

“The significant headwinds from the [Middle East] conflict will be more fully reflected in the second quarter of 2026, with the possibility of a quarterly contraction which would be the first quarterly decline since the GFC (excluding COVID),” they warned.

If we accept the simplistic definition of a recession as being two consecutive quarters of negative growth, then Westpac’s economics team is warning about the possible start of a recession.

HSBC’s economics team has also been saying that the risk is rising that there may be two consecutive quarters of negative growth soon.

Tue 9 Jun 2026 at 1:47pm

A question of independence

Thank Gareth. They do get paid by their bank don’t they? Yeah, real independent.

– Josh

Thanks Josh. They do get paid by their bank. But think of it this way. The economics teams at major banks are competing against each other to produce the most reliable set of economic forecasts.

They want investors and traders to subscribe to their research output. If you’re an investor who wants access to that information, to inform your thinking about inflation and interest rates and everything else, which bank would you choose?

I’d choose the bank that seems to have the most reliable forecasts, with the most insightful analysis. So they have an incentive to produce forecasts that are correct.

That’s very different from producing forecasts that the CEO of their bank may want to see.

Tue 9 Jun 2026 at 1:39pm

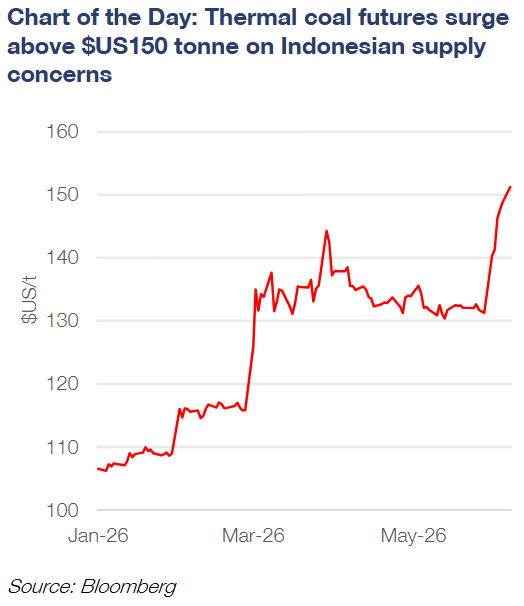

Thermal coal futures surge above $US150 a tonne

John Oh, CBA’s sustainable and energy economist, says thermal coal futures have surged above $US150/tonne on concerns about Indonesian supply.

He says in late May, Indonesia’s government announced plans to centralise exports of palm oil, thermal coal and ferroalloys.

Under the plan, exports would be channelled through the Danantara Sumberdaya Indonesia (DSI), a government-appointed body. Full implementation is expected to begin in January 2027, with producers obliged to submit export-related documents to the DSI from the beginning of June.

Oh says under-invoicing allegations in Indonesia (i.e. producers under-reporting export volumes resulting in lower tax revenues for the government) have been a key driver of the policy announcement.

But he says the short timeframe between the late May announcement and the early June obligation requirement has contributed to thermal coal delivery delays out of Indonesia, heightening concerns around supply disruption.

“After hovering between $US130/tonne and $US135/tonne for most of May, thermal coal futures have surged to $US151/tonne, the highest level since the beginning of the Middle East conflict,” he says.

“The recent rally has been driven by Indonesia’s plans to centralise exports of key commodities including thermal coal.

“With Indonesia accounting for 45-50% of internationally traded thermal coal supply, recent delayed deliveries out of Indonesia have heightened concerns around ongoing supply disruption.

“It’s worth noting with minimal disruption to physical thermal coal trade from the Strait of Hormuz closure, higher coal demand was driven by higher gas prices incentivising greater gas-to-coal switching from the power sector. This saw prices rise as high as $US144/tonne (i.e.23% above pre-war levels) in late March.”

Tue 9 Jun 2026 at 1:18pm

Economics research teams

Banks are ‘packing it’ in 1980s parlance.They are desperate to jawbone the RBA into lowering rates, despite the massive inflation issue.Their balance sheets are cracking, and they again want to be saved rather than fess up.

– Josh

Thanks Josh.

Just fyi, the economics research teams at Australia’s major banks aren’t part of the banks’ executive teams. They have no control over their bank’s business or investment decisions, nor what the bank does with interest rates for home loans.

The bank’s executive leadership may listen to what the economics teams are thinking about the world, but they don’t tell their economics teams what to write/publish (including their interest rate forecasts).

Tue 9 Jun 2026 at 12:53pm

On one hand, on the other hand

So summing up the NAB note . ‘We could be right or we could be wrong’. Very informative. I could tell you that and I have no economic credentials!

– Phillip

Thank you Phillip, for your contribution.

Tue 9 Jun 2026 at 12:30pm

NAB thinks the next RBA move in the cash rate is ‘down’

NAB’s economics team has circulated a note with very interesting points about the cash rate, house prices, credit growth and inflation.

Here’s what they say:

- We no longer expect the RBA to hike by 25 basis points in August, and now see the cash rate peaking at the current rate of 4.35% for the cycle. The next move in the cash rate is likely to be down, but the timing is uncertain. To highlight shifting risks to the RBA outlook, we have brought forward our expected easing from H2 2027 to Q2 2027 – which now sees the cash rate end 2027 at 3.6%.

- We are minded to view the proposed changes to taxation arrangements for housing and other asset classes as an exogenous tightening of financial conditions.

- Tighter financial conditions will be reflected in both a slowing in house price growth and housing credit growth. Consequently, we have made downward revisions to our forecasts for both of these variables.

- Both Q1 GDP data and the NAB business survey suggest momentum in the economy has slowed, meaning that growth has likely peaked for the cycle. Should activity data weaken more quickly than anticipated, the RBA will cut earlier than we currently forecast.

- However, we are cognisant that there is still considerable uncertainty around the outlook, both with respect to activity and inflation. Indeed, it is possible that consumption outcomes are stronger than we forecast. Additionally, it is possible that the housing downturn is not as impactful on activity as we think.

- On the prices side, we are still forecasting above target core inflation through to mid-2027. This outlook is not dissimilar to that of the RBA, as outlined in last month’s SoMP [Statement on Monetary Policy] and is likely to keep the RBA watchful around pass through from higher input costs to final prices.

- We have been worried about a broad and rapid dissemination of inflationary pressures, but the recent slowing in momentum in the economy may short-circuit this dynamic somewhat. If so, margins will compress and weaker labour market outcomes are a risk.

- In summary, we have greater conviction that the next move in rates is down, but less conviction on the timing. In contrast, the AUD front-end is still priced for hikes. If we are correct on the direction of the RBA cash rate, there is scope for decent moves in AUD and front-end rates as the market adjusts to a more dovish view.