Over the last six months, Freshpet’s shares have sunk to $50.60, producing a disappointing 19.6% loss – a stark contrast to the S&P 500’s 6.9% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Freshpet, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Freshpet Not Exciting?

Despite the more favorable entry price, we’re swiping left on Freshpet for now. Here are three reasons why FRPT doesn’t excite us, plus one stock we’d rather own.

1. Fewer Distribution Channels Limit Its Ceiling

With $1.14 billion in revenue over the past 12 months, Freshpet is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

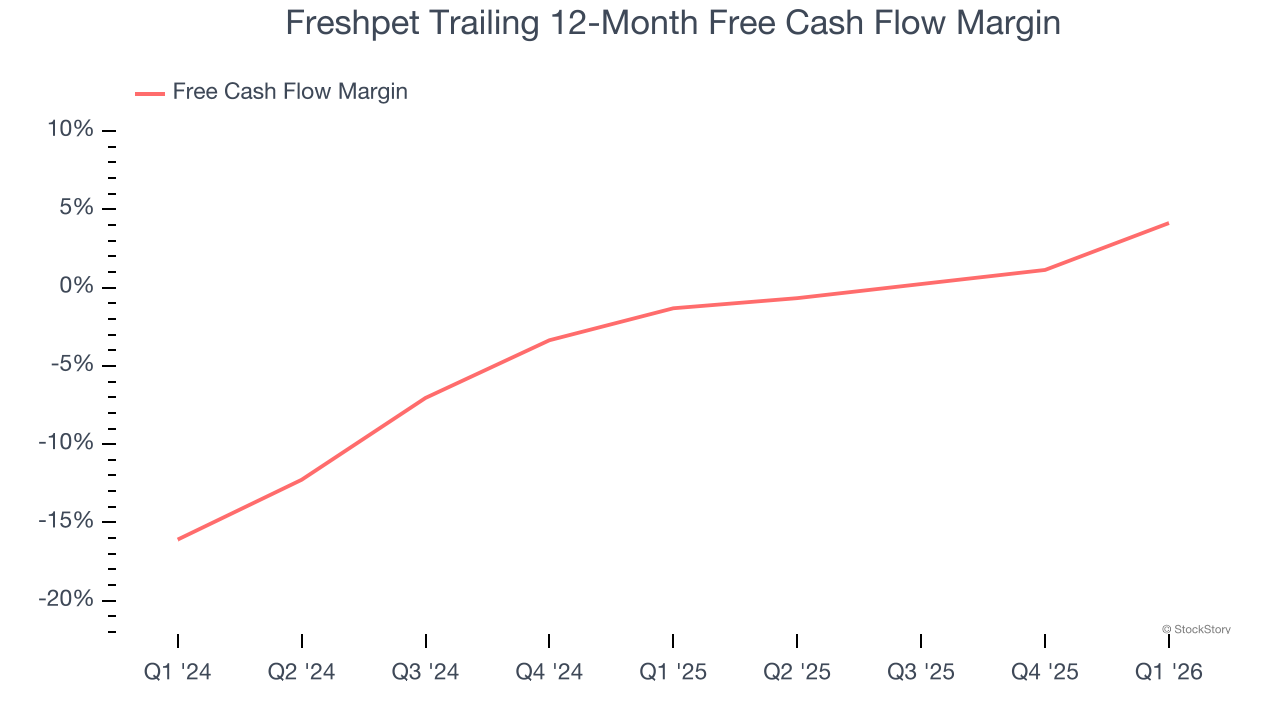

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Freshpet has shown weak cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.6%, below what we’d expect for a consumer staples business.

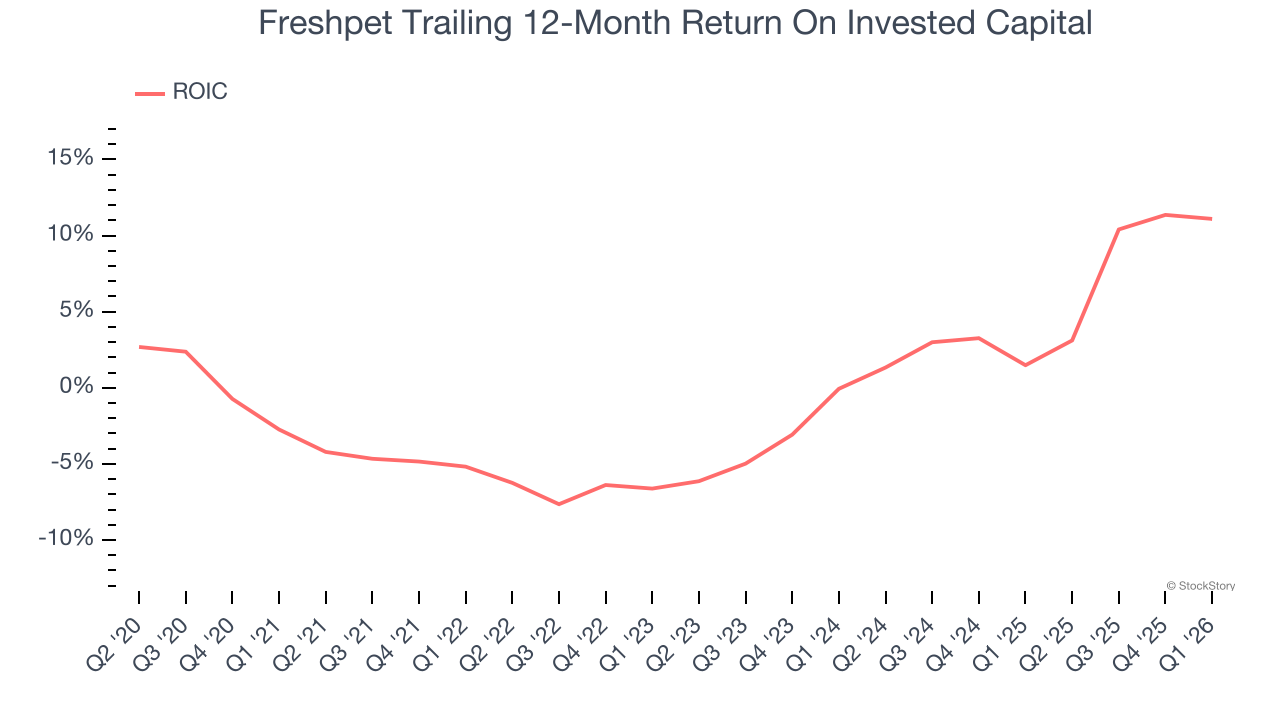

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Freshpet historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.1%, lower than the typical cost of capital (how much it costs to raise money) for consumer staples companies.

Final Judgment

Freshpet’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 34.3× forward P/E (or $50.60 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in – we think other companies feature superior fundamentals at the moment. We’d suggest looking at one of our top software and edge computing picks.

Stocks We Like More Than Freshpet

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.