Quick Summary

- A Fed rate hike would not automatically be bad for stocks. History shows that since 1994, the S&P 500 has been higher six months after the first Fed rate hike in five of seven tightening cycles. The average six-month gain after a hike was 3.8 percent.

- The reason for the hike matters more than the hike itself. If the Fed is raising rates because the economy is strong, jobs are plentiful, and consumers are still spending, stocks can continue to perform well. But if the Fed is forced to hike aggressively because inflation is out of control, as in 2022, the market risk is much higher.

- Markets usually adjust before the Fed acts. Investors often price in rate changes ahead of the official announcement. That means a widely expected hike may cause short-term volatility, but it is rarely a complete surprise to the market.

- Strong corporate earnings remain the key support for stocks. S&P 500 earnings have been growing at an unusually strong pace, with roughly 20 percent expected growth over the next year. If earnings continue to rise, that can help offset the pressure of modestly higher interest rates.

For much of the year, Wall Street focused on when the Federal Reserve might cut interest rates. Now, investors are facing a new question: What happens if the Fed decides to raise them instead?

This scenario is no longer unlikely. At its June 2026 meeting, the Fed kept its short-term rate between 3.5 percent and 3.75 percent, but new projections suggest a hike could come later this year. The federal funds futures markets expect about a 0.42 percentage-point increase before year end, which is another way of saying there is a quarter-point hike baked into the cake, and there might even be another on top of it.

I get why that might sound worrying to stock market investors. Higher rates make bonds more attractive on a relative basis, increase borrowing costs, and can slow spending.

The history is less frightening than the headline

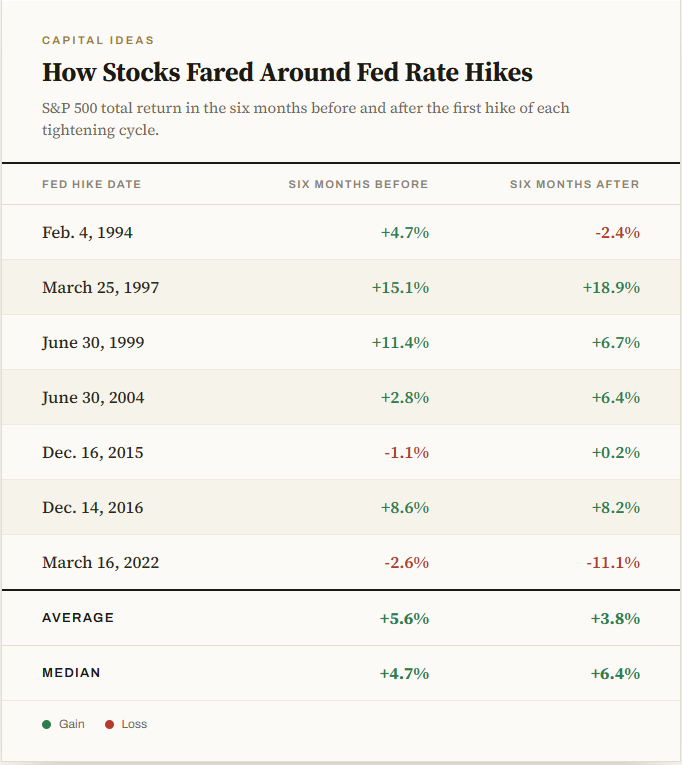

I looked back at Fed decisions since 1994, when they started announcing changes openly. Then I checked how the S&P 500 performed from six months before the announcement to the day of the hike and from the hike to six months after. Here is what I found. (These numbers show price returns only, not including dividends.)

In five out of seven cases, the S&P 500 was higher six months after a rate hike. The average gain was 3.8 percent, and the median gain was 6.4 percent. It turns out that a rate hike doesn’t always end a bull market.

The six months leading up to those hikes are also interesting. Stocks gained an average of 5.6 percent during that time. In other words, the Fed often began raising rates after the market was already going up. That makes sense because hikes are often a tool the Fed uses to slow the economy, which means things were humming along.

The two negative periods following a rate increase are worth noting. After the 1994 hike, stocks fell 2.4 percent. That is not great, but it is not a disaster either. The bigger drop came after the March 2022 hike, when the S&P 500 fell 11.1 percent over six months. The other five times, results ranged from flat to a gain of almost 19 percent.

But 2022 was not just about a single quarter-point hike. Inflation was at its highest in 40 years, and the Fed initiated an aggressive monetary-policy tightening campaign, raising rates by over four percentage points. It is important to consider the pace and rationale of rate-hike cycles.

Why stocks can rise while rates rise

A central bank, like the Fed, usually raises rates when consumption is strong, the job market is hot, inflation is too high, or some mix of these.

Strong demand and good employment can also help a company’s sales and profits. This creates a push and pull. Higher rates put pressure on stock prices, but a strong economy and rising profits can lift them. If earnings are strong enough, they can outweigh the effect of higher rates.

Also, markets do not wait for the Fed to act. Bond yields, mortgage rates, and stock prices often change as traders adjust their expectations. By the time the Fed announces a widely expected rate hike, some of the adjustments have usually already taken place. The announcement can still cause a sharp reaction for a day or a week, but it is rarely a surprise.

A small rate hike can also reassure investors that the Fed is serious about stopping inflation from getting out of control. That does not mean a hike is painless, but it can be less harmful in the long run than letting inflation rise and then having to take stronger action later.

The important difference is whether the Fed is gently slowing an economy that can handle it or hitting the brakes hard because inflation is out of control. Stocks can keep rising in the first case, but it is much tougher in the second.

The earnings engine is powerful

Corporate earnings momentum is excellent. S&P 500 earnings rose about 22 percent for the 12 months ending in the second quarter of 2026.

The positive outlook continues beyond the second quarter. The expected growth rate for the next year is about 20 percent, compared to a 10-year average of 8.6 percent. In a very strong year, earnings growth might reach 15 percent. So, 20 percent earnings growth is ambitious, but the last 12 months proved it is possible.

Corporate earnings are what drive the stock market. Interest rates affect how much investors are willing to pay for those earnings. I suspect any interest rate hikes, if any, will be very modest compared to 2022, so a 20 percent earnings growth rate can offset that risk.

The Fed can slow things down, but it does not have to stop the economy or the stock market completely. The point is not to be complacent, but to distinguish between a normal policy change and one that could really hurt profits and growth.

Allen Harris is an owner of Berkshire Money Management in Great Barrington and Dalton, managing more than $1 billion of investments. Unless specifically identified as original research or data gathering, some or all of the data cited is attributable to third-party sources. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Advisor’s clients may or may not hold the securities discussed in their portfolios. Advisor makes no representation that any of the securities discussed have been or will be profitable. Full disclosures here. Direct inquiries to Allen at [email protected].