Tilray Brands‘ (TLRY +4.29%) track record over the past five years hasn’t been great, to say the least. The company has lost more than 90% of its value. Its shares are now trading at just under $5 apiece. Is the stock undervalued at current levels? Or is it a value trap?

Image source: The Motley Fool.

A tough road ahead

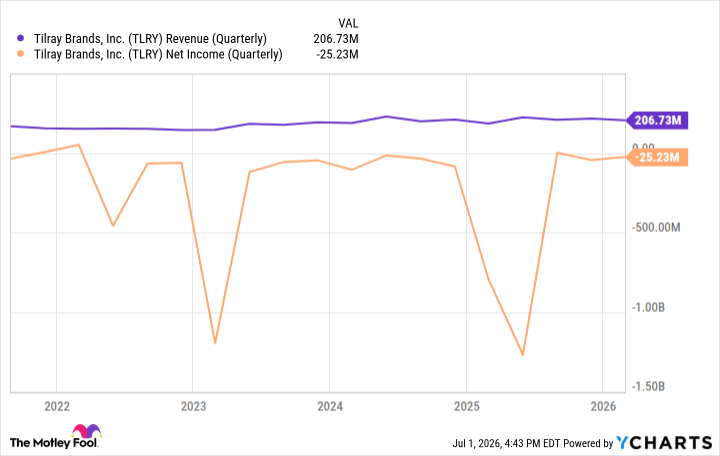

Tilray is a leader in the Canadian recreational cannabis market. But that hasn’t allowed the company to post solid financial results, especially as the sector has been challenging to navigate. The company’s organic revenue growth has been subpar — at best — for years. Meanwhile, Tilray remains unprofitable.

TLRY Revenue (Quarterly) data by YCharts

However, there could be a ray of hope for Tilray. The company has significantly diversified its business in recent years and reduced its reliance on recreational cannabis-related operations. Tilray’s business spans craft brewing — it is the fourth-largest craft brewer in the U.S. — the sale of hemp-based wellness products, and pharmaceuticals.

Further, recent developments in the U.S. could boost the company’s business. Products that contain marijuana and are approved by the U.S. Food and Drug Administration, as well as cannabis products regulated at the state level, have been classified as Schedule III substances, whereas they were previously in the Schedule I category. This change means that these products are deemed as having some medical benefits and as being less prone to abuse and addiction than those in Schedule I. This could open an opportunity in medical research, a niche where Tilray already has a footprint. Does any of this make Tilray stock a buy?

Today’s Change

Current Price

It’s worth noting that, even with a more diversified business, Tilray hasn’t consistently posted strong financial results. There have been some improvements, to be sure, but that’s not saying much considering how badly its cannabis business had been performing. Also, regulatory progress in the industry is no guarantee that Tilray can turn things around.

Even as governments become more friendly toward marijuana, there remain stringent rules and regulations that severely limit the market potential. That’s what happened in Canada, and it may happen in the U.S. as well. And even if it doesn’t, the large opportunity that friendlier cannabis laws will create will likely attract significant competition from companies with deeper pockets. In fairness, much of that applies to most pot growers.

It’s hard to find one whose business is remotely strong. But Tilray certainly isn’t the best one to consider investing in. That title, in my view, goes to Green Thumb Industries (GTBIF +0.00%), a consistently profitable multi-state operator with a strong presence in some of the most lucrative U.S. markets, including Florida. Tilray’s shares may look cheap, but the company will likely face more headwinds and continue losing value. Investors looking to capitalize on the industry’s growth potential should look elsewhere.