The stock market was not impressed as another dose of soft inflation data and a gentler tone from Fed Chair Warsh eased Fed rate hike fears.

- Wholesale prices fell in June, echoing the surprise drop in consumer inflation a day earlier

- Fed chair Kevin Warsh softened his tone, waving off the AI boom’s inflation as a passing, one-time bump

- Yet the Fed’s favored inflation gauge is still set to rise, and tomorrow’s retail sales may reveal a strained consumer

The bellwether S&P 500 keeps drifting, still pinned in the range that has held it since mid-May. Crude oil stalled after this week’s war-driven surge. The signal worth watching came instead from bonds and gold, which seem to be telling a more convincing story.

Bonds and gold sense a shift

A day earlier, Treasury yields had refused to fall despite a soft consumer inflation print, held up by hawkish remarks from Federal Reserve Chair Kevin Warsh. Today they gave way, with bonds re-engaging the bottoming process they have been attempting since mid-May.

Gold has been the steadier tell: through the renewed oil shock and Warsh’s tough talk, it flatly refused to sell off, holding its range near $4000/oz while the dollar and bonds wavered. That is starting to look prescient. The US dollar – impressively resilient a day ago – had a rough session and now looks like it may lose the uptrend it built since May.

A second soft report, and a softer Fed

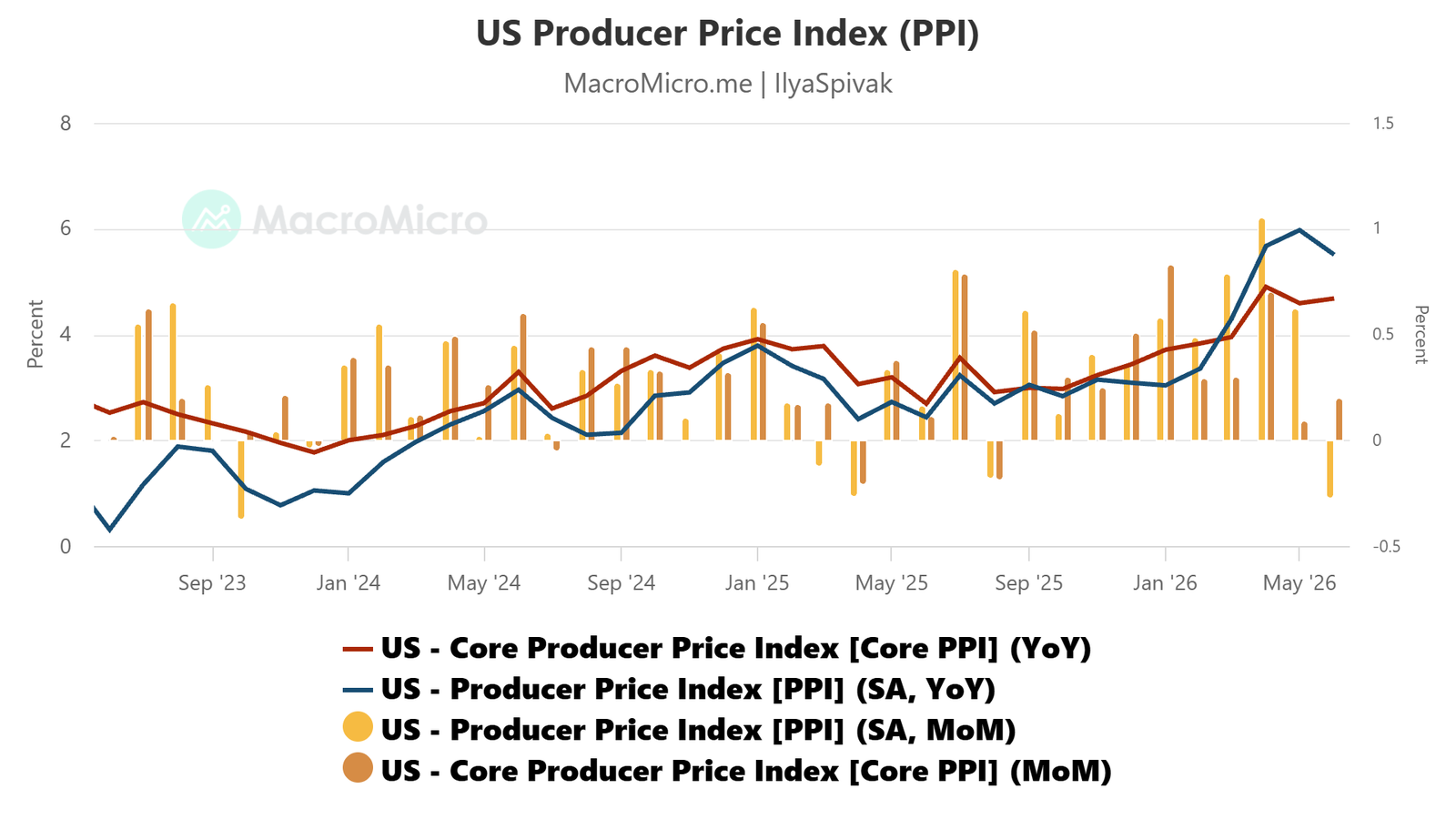

June’s producer price index (PPI) data, a measure of wholesale inflation, offered the markets a welcome surprise. The headline number showed prices fell 0.3% last month, the first negative print since last August, against expectations for no change. The core measure excluding food and energy costs rose by a milder-than-forecast 0.2%.

This echoed the previous day’s consumer price index (CPI) report, which also came in soft and marked the first monthly decline since 2020. For both data sets, a steep drop in energy did nearly all the work, reflecting crude oil’s more than 25% slide across May and June.

Just as telling was the shift in tone from Mr. Warsh. On the second day of his semi-annual congressional testimony, pressed on whether the AI buildout is itself inflationary, he waved the concern away, conceding it is driving prices higher, but casting that as a one-time adjustment that fresh supply, in the form of all those data centers that “hyperscaler” technology firms have pledged to build, will eventually resolve.

The fist-pounding on price stability remained, yet the markets perceived less urgency to hike interest rates than they were previously betting on. The tightening priced in for this year slipped to about 23 basis points (bps). That still leans firmly in favor of one 25bps rate hike, but recent hawkish confidence has slipped.

Why the relief may be premature

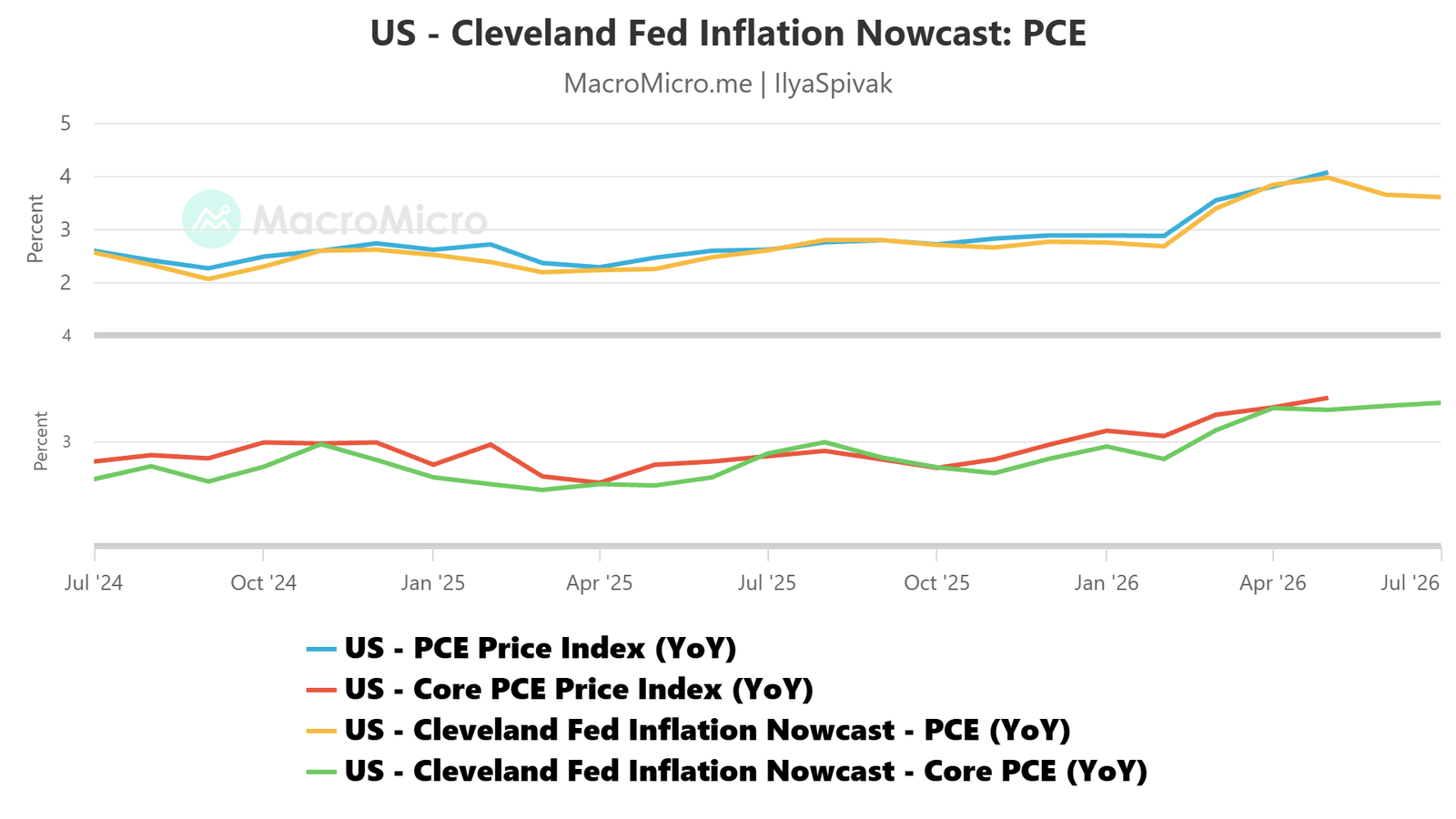

The trouble is that cooling inflation seems to be almost entirely an energy story, and the durable kind of price growth remains under the surface. The Cleveland Fed’s closely watched “nowcast” of the personal consumption expenditures (PCE) price index, the central bank’s favored inflation gauge, sees core prices rising in June and July.

That is the inflation that Warsh is trying to wave off, and it speaks to the shape of US growth. First-quarter gross domestic product (GDP) rose 2.1%, and the biggest contributor by far was lightning-fast growth in business investment, powered by the data center boom. Consumption – which makes up 68% of GDP, compared with investment’s five-times-smaller 14% – contributed barely anything at all.

Forcing so small an engine of demand to carry growth means running it hot. Indeed, its annualized growth rate surged above 10%. This has spun inflation that has landed in the core service sector, where the lion’s share of household demand resides. The boom keeping growth alive is squeezing the consumer that the economy ultimately leans on.

If that far larger growth engine retrenches even modestly from here, it could overwhelm the AI boom and drag overall growth into reverse. Australia, the Eurozone, and the UK show that pattern already: buoyant AI-linked factories yet shrinking economies as their dominant service sectors contract under the price squeeze.

The coming test: is the consumer cracking?

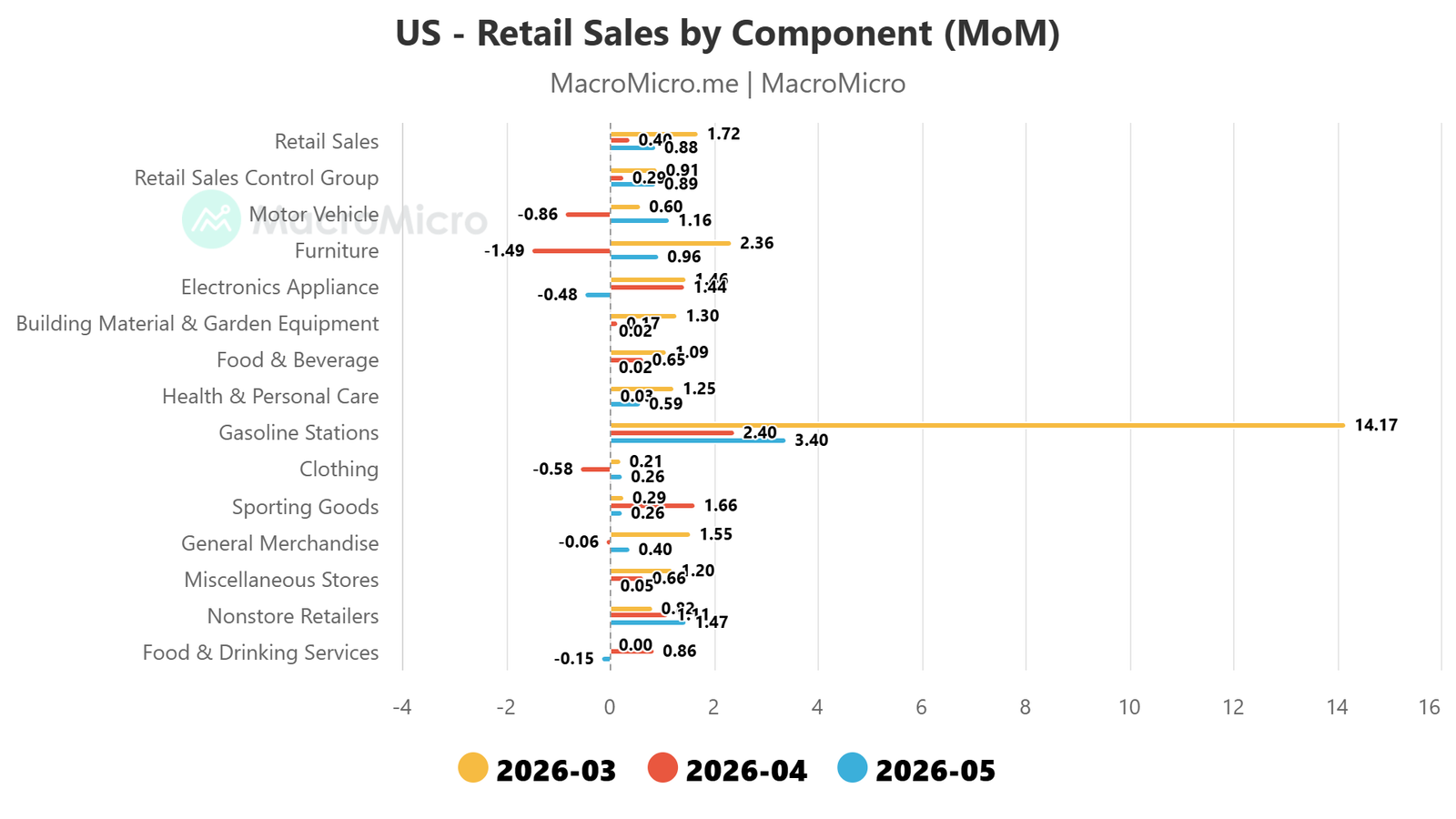

That makes the incoming US retail sales report a key input to watch. Spending is expected to slow to 0.2% month-on-month from 0.9% previously, the weakest since January. Some of that softness is harmless: retail sales are not adjusted for inflation, so cheaper fuel alone could drag the figure lower.

The catch is that gasoline prices have not fallen nearly as far as crude, since a shortage of refined product has kept pump prices elevated even as the feedstock prices eased. So, the consumer may not get all of the relief that crude oil prices imply. If that comes along with weakness in cyclical and discretionary categories like food and drinking services, that may point to something more worrying than somewhat cheaper gas.

That is the fault line running beneath a calm-looking market. If consumers appear to be getting more defensive after the noise from oil prices is factored out of the equation, then a potent cyclical threat is menacing the economy. Warsh’s hope that AI-linked inflation eventually solves itself will look like wishful thinking if it is already fueling demand destruction.

That would recast the narrative: a Fed fixated on prices while the consumer buckles would be slow to cut, exactly the delay that lets a downturn take hold. That may be why gold refuses to fall and why bonds ultimately chose to listen to the soft inflation data. The market may be starting to look past the question how many rate hikes are ahead to whether the real move turns out to be a cut, forced by an economy that rolled over.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

© copyright 2013 – 2026 tastylive, Inc.