![]()

Summary

- Powell’s recent press conference did not indicate a dovish stance on rate cuts in 2024.

- The stock market rally during Powell’s press conference was due to the 2:35 PM ET VIX melt that occurs at nearly every meeting.

- The immediate price action following the Fed meeting does not accurately reflect the market’s longer-term direction.

- Looking for a helping hand in the market? Members of Reading The Markets get exclusive ideas and guidance to navigate any climate. Learn More »

gerenme

People see and hear what they want. While Powell spoke softly at Wednesday’s press conference, the message was that rate cuts will take longer to come by in 2024, and longer will mean fewer rate cuts.

Powell has never been one to speak with harsh words. On top of that, market mechanics give this often false optical view that he is being dovish. But in reality, that is not what has happened.

The Fed went out of its way to include the statement note in the third sentence of the opening paragraph:

In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.

This is a pretty clear statement and not a dovish one.

However, because the equity market “rallied” during Powell’s press conference, the media projected the idea that Powell was making dovish statements to the public. That’s not what caused the stock market to rally at all. What caused the market to rally was the mechanical force of implied volatility declining as put hedges were being unwound.

This event-risk unwind happens so often that in a free commentary to all SA followers on Tuesday, the day before the Fed meeting, I noted that we would get the 2:35 volatility crush, sending the equity market higher.

It seems likely that once we get past the Fed, we could see that usual volatility crush at around 2:35 PM ET. That is typically when the S&P 500 rallies and everyone starts to comment about the market, with Powell having a dovish tone. Even though we know that the rally has nothing to do with Powell but the passing of the event risk as the VIX 1 Day drops like a stone and heads lower.

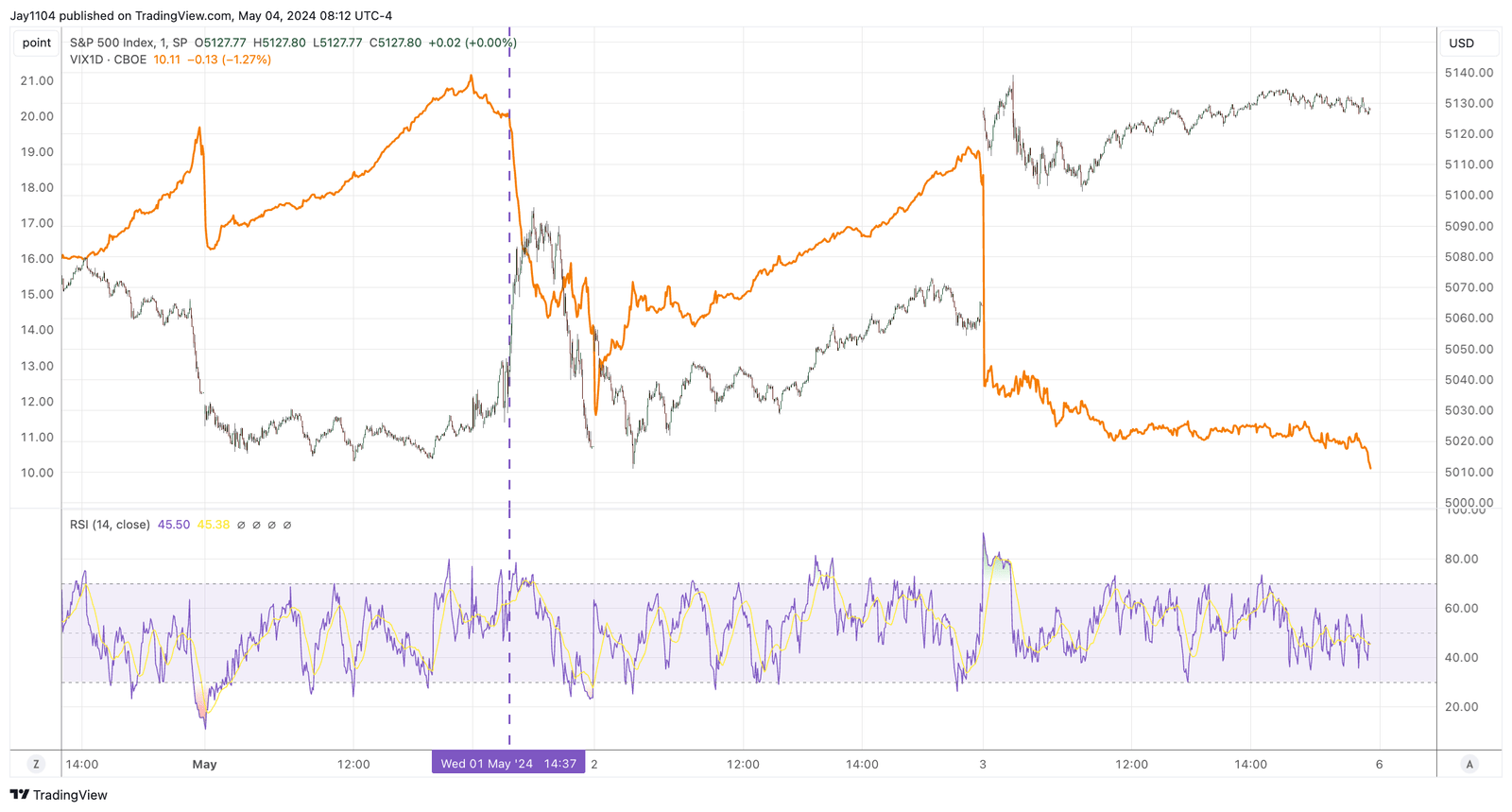

TradingView

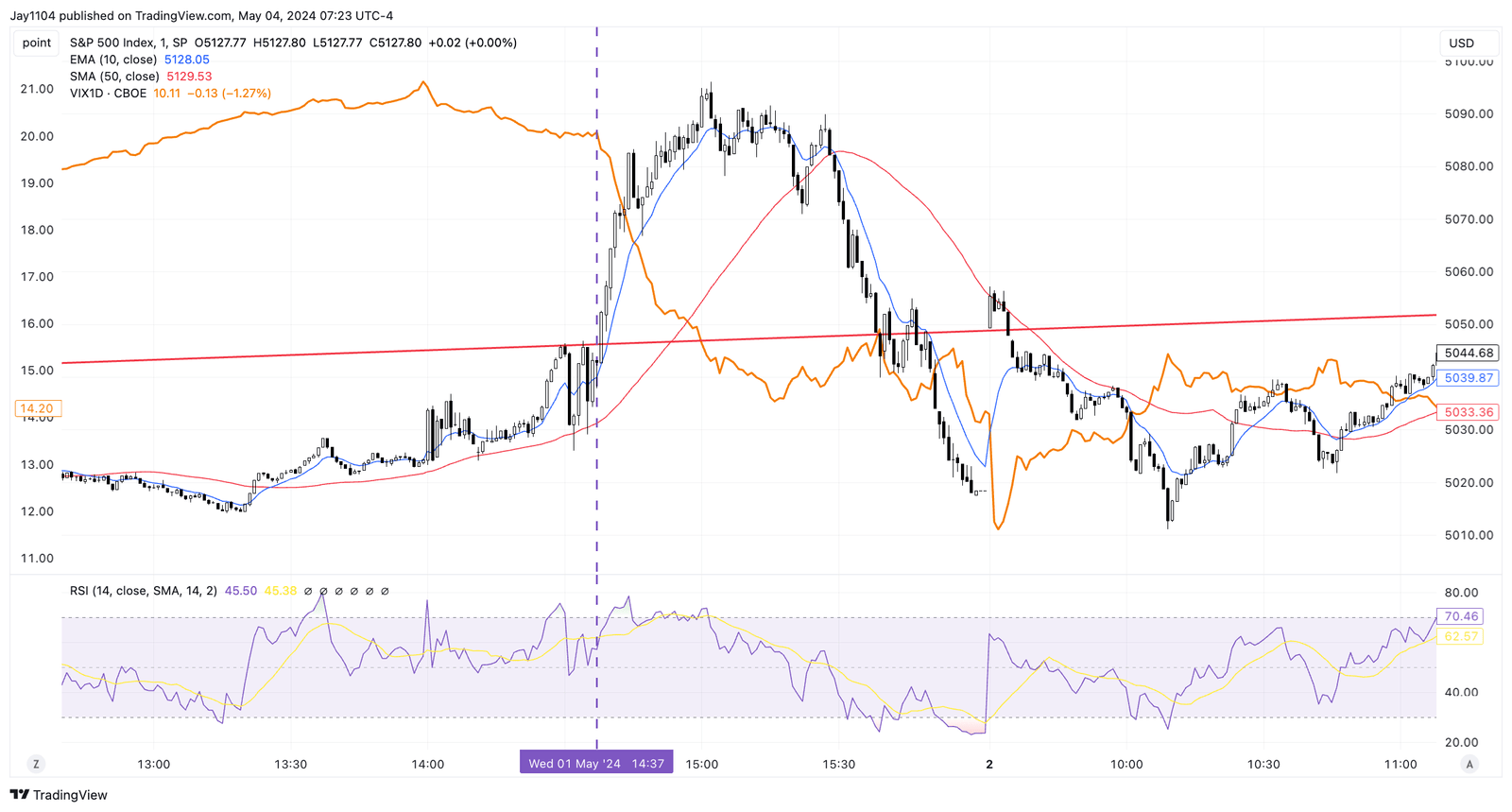

This event happens at almost every press conference, with the same happening at the March 20 press conference.

TradingView

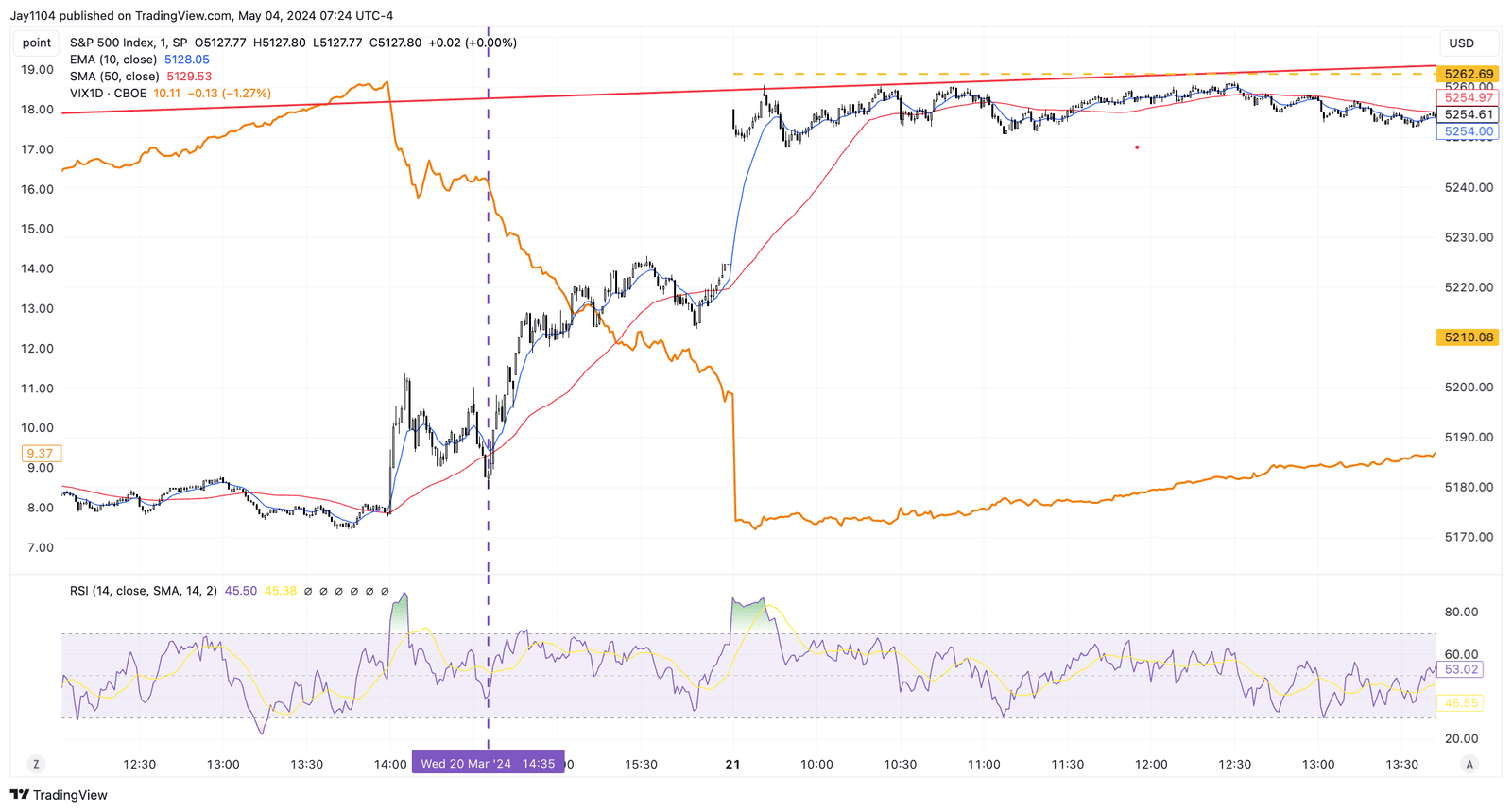

It also happened at the January FOMC press conference, but it didn’t last as long and had less of an overall impact.

TradingView

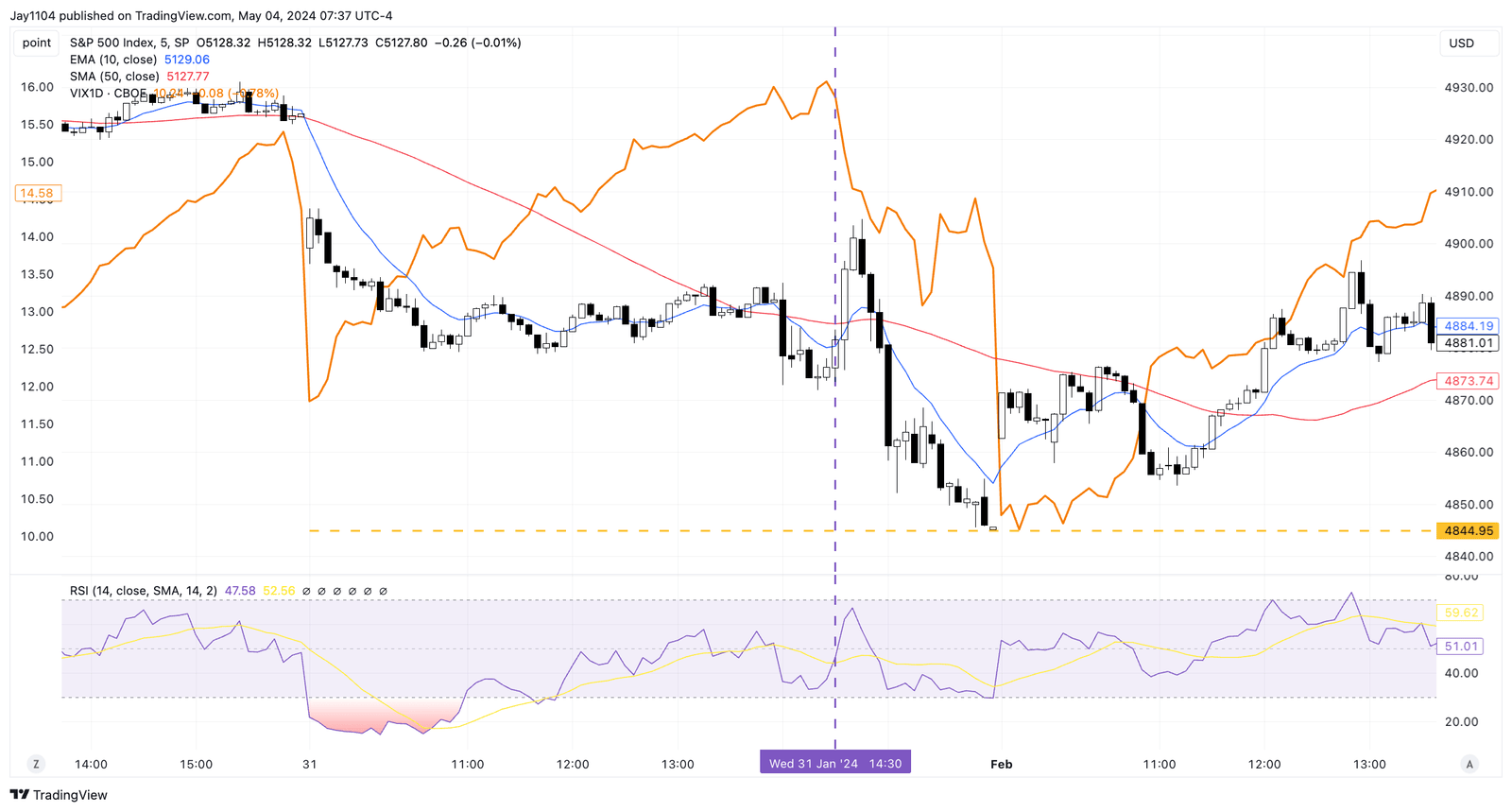

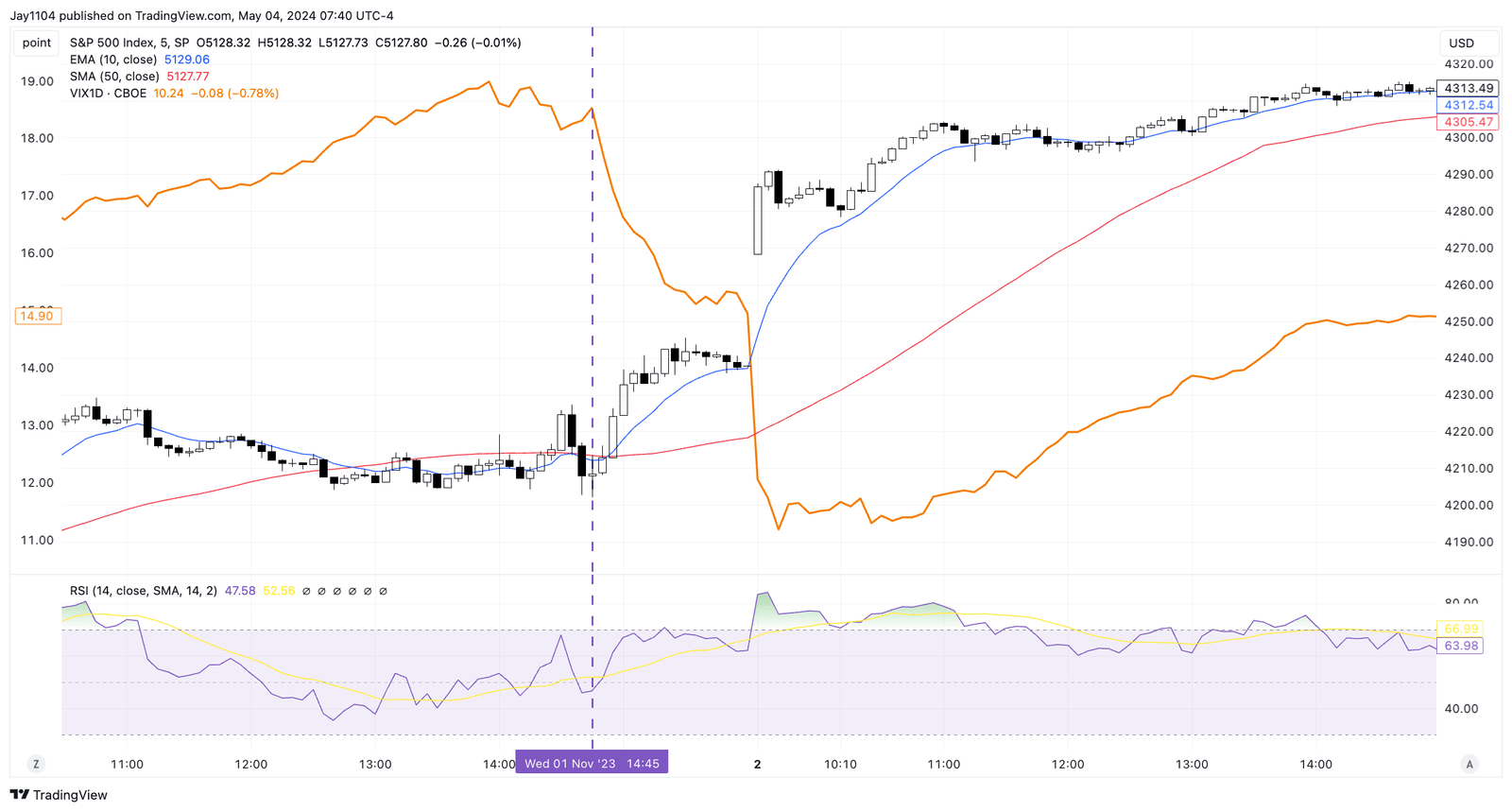

It also happened at the November 1 FOMC meeting, but it started about 10 minutes later, at 2:45 PM ET.

TradingView

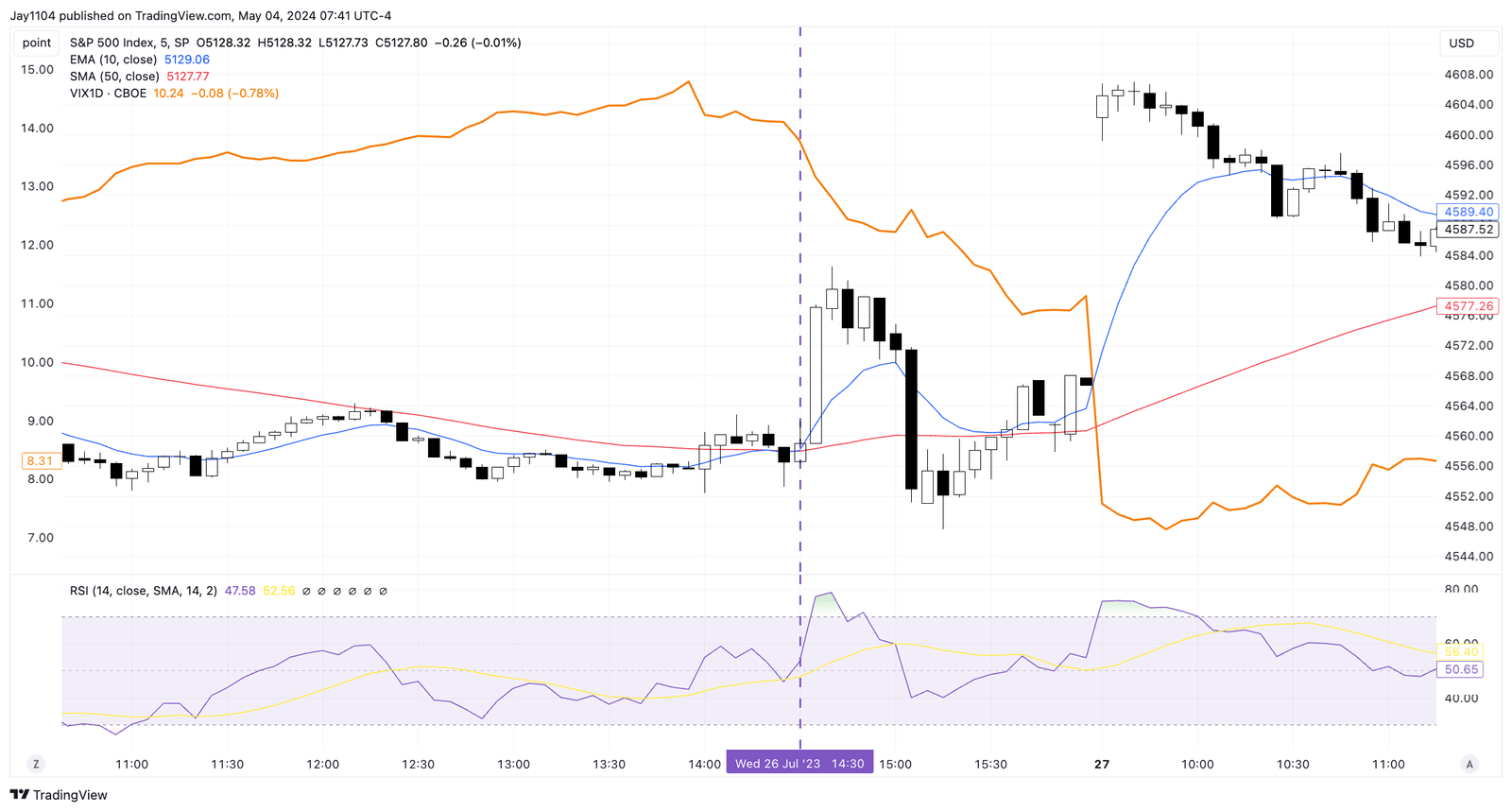

The July 26 FOMC meeting also demonstrated this implied volatility crush, starting at 2:30 PM ET.

TradingView

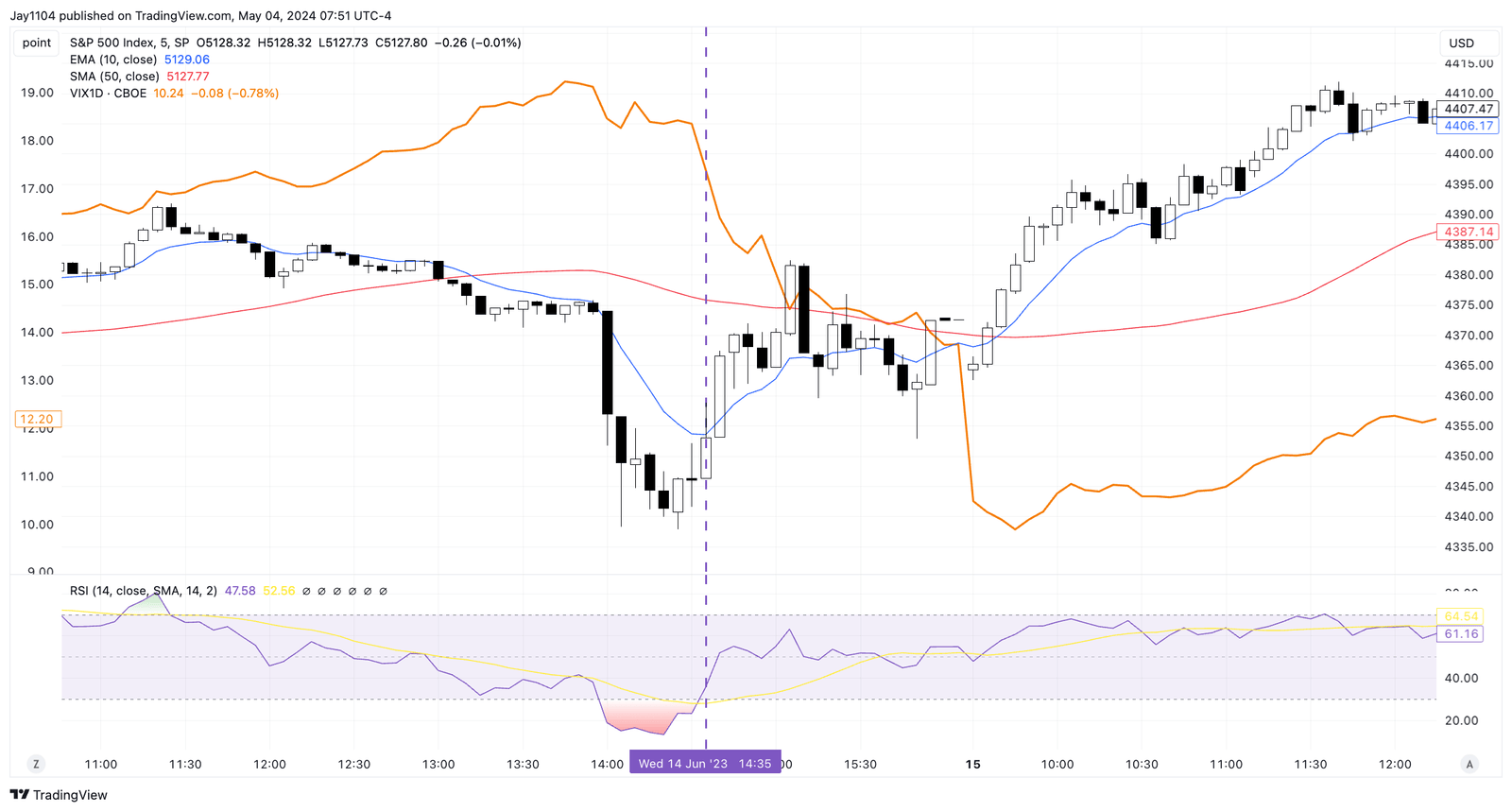

It happened again on June 14, 2023, starting at 2:30 to 2:35 ET range.

TradingView

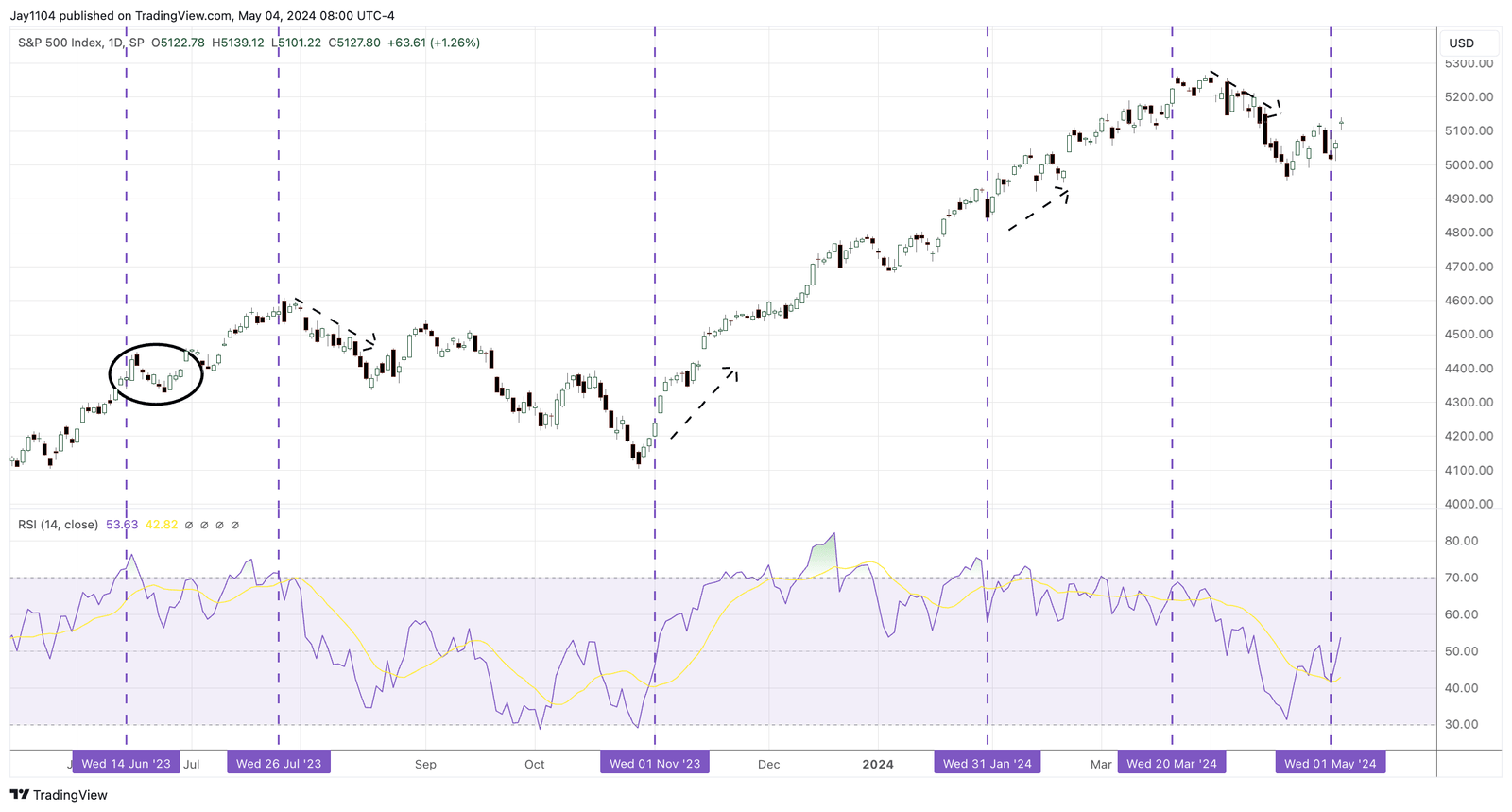

So while not every Fed meeting has provided this implied volatility crush, which helped to ramp stock indexes, giving us that “Powell is Dovish” appearance, it has happened in 6 of the past eight meetings starting in June 2023, with the crush not happening in September or December of 2023.

Additionally, where the equity market was a week later didn’t often reflect the “dovish” tone of the meeting results. In two of the meetings, despite the initial rally, the market was lower in the coming weeks, while in two, it was higher, and in 1, it had moved sideways. We are still waiting to see what happens following this meeting.

This 2:35 PM ET volatility crush has been happening consistently for some time, even before the middle of 2023, so trying to assess the market’s direction in the moments following the meeting or taking the price action during the meeting is a waste of time. It has no bearing on the general direction of the market that will come in the following weeks.

TradingView

The wise thing, at least based on experience, is not even paying attention to the market’s price action the day of, or for that matter, in the days immediately following, the Fed meeting. Much of the initial price action is likely concerned with positioning around such an event. Large institutional players may be unable to “press a button” to unwind trades gone wrong or book profits. It could take a day or two to unwind a trade completely.

Couple that with the ramp-up of implied volatility ahead of the job report on Friday and the implied volatility crush that followed the job report, and it gives the appearance of a market reacting positively to a dovish Fed and a “Goldilocks” job report. But you saw the typical 2:35 volatility crush on Wednesday, and Friday was the job report crush. It is even why stocks can rally following a hotter-than-expected CPI report.

Again, it is why, in a write-up, the day before the April Jobs report it becomes easy to predict price action that is likely to follow:

The VIX1D and the S&P 500 moved higher today. However, after tomorrow’s job report, the VIX1D will probably crater again. So again, a move higher in the S&P 500, regardless of the data, seems probable given the implied volatility reset that will be needed. Once IV resets, the market will trade “normally” again.

This happened when the S&P 500 rallied on Friday and flatlined for the rest of the trading day once the VIX 1-Day stopped falling following the April job report.

TradingView

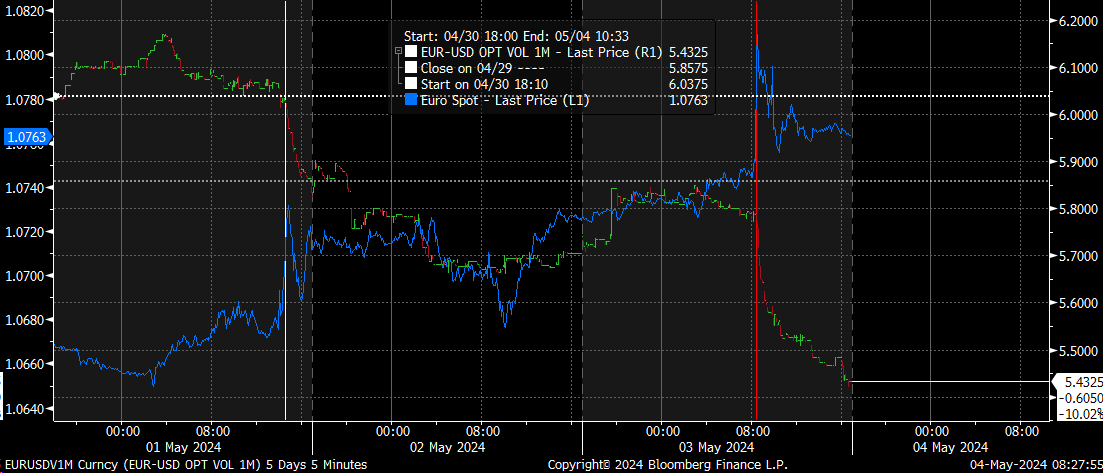

Unfortunately, this doesn’t just happen in equities. Implied volatility resets happen across asset classes, such as the EUR/USD currency pair, which also saw a 2:35 PM ET volatility crush on May 1 and another volatility crush on May 3 following the job report.

Bloomberg

This tells us that one should not be so quick to conclude macro events as if they mean something significant. All that takes place is a reset in implied volatility levels, as hedges and bets on market directions are being unwound, resulting in flows shifting around those events. This means that the outcome of those events is likely to be seen in the following weeks.

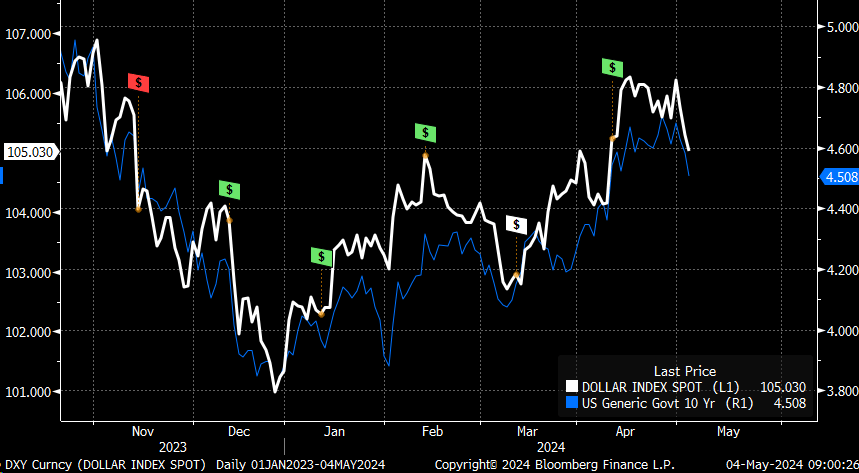

It is then that you realize that the December CPI report shocked markets, marking a turning point in the projected number of rate cuts.

Bloomberg

The hotter January CPI report caused the equity market to flatline since the middle of February.

Bloomberg

That rate and the dollar have surged since the February CPI report in March, while the strong dollar and higher rates caused the equity market to struggle.

Bloomberg

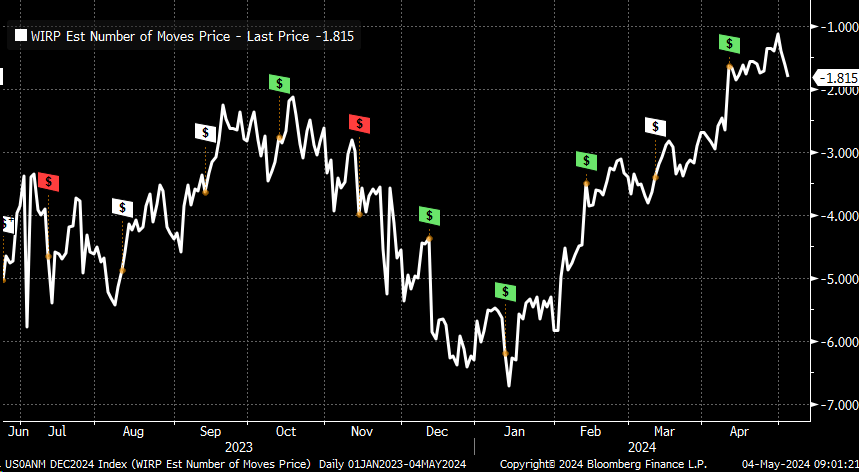

Or that the swaps market has seen fewer than two price cuts since the March CPI report.

Bloomberg

Yep, tell me more about it.

Judging the outcome of an event is not a wise idea in the immediate moments that follow. This market is far more complex than it would seem on the surface, and often, the knee-jerk market reactions tell us nothing about the longer-term trends that are likely to develop, which is what most of us long-term investors care the most about.

Join Reading The Markets Risk-Free With A Two-Week Trial!

(*The Free Trial offer is not available in the App Store)

Reading the Markets helps readers cut through all the noise, delivering daily video and written market commentaries to prepare you for upcoming events.

We use a repeated and detailed process of watching the fundamental trends, technical charts, and options trading data. The process helps isolate and determine where a stock, sector, or market may be heading over various time frames.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Charts used with the permission of Bloomberg Finance L.P. This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.