The stock market is surging. Economic data has been coming in better than expected, and many influential companies have been posting robust financial results that are flashing positive signals and sending valuations higher. With expectations that the Federal Reserve will begin cutting interest rates this year, the stars could be aligning for a sustained bullish run.

But even though the new bull market has helped send share prices to record levels for some high-profile companies, there are some great stocks out there that still trade far below their previous valuation highs. If you’re looking for investment opportunities that can help you get in position for a bull run, read on to see why two Motley Fool contributors identified these artificial intelligence (AI) growth stocks as top buys.

An AI stock that still has big upside

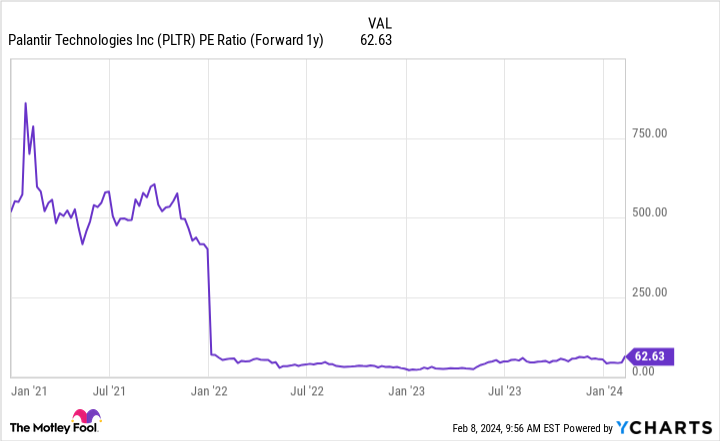

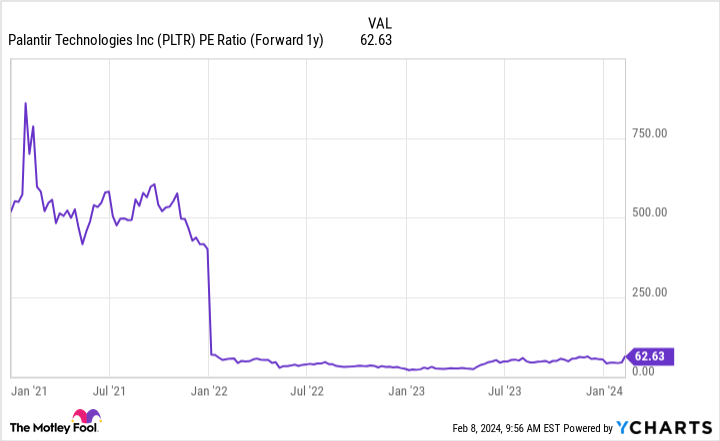

Parkev Tatevosian (Palantir Technologies): Thanks to strong business results and excitement for AI stocks, Palantir Technologies‘ (NYSE: PLTR) stock is soaring. Nevertheless, it presents an attractive opportunity for long-term investors looking for a growth stock at a reasonable valuation. Even after tripling in value over the past year, Palantir stock remains down 38% off all-time highs hit in early 2021.

Palantir is one of the leading service providers in AI software that enhances operations for enterprises and institutions. Palantir’s sales rose roughly 275% between 2018 and 2023, increasing from $595 million to $2.23 billion. Part of the reason for that growth is the company has made strong inroads with government institutions. Palantir’s next growth wave will arguably come from providing more services to the private sector and to smaller businesses. Palantir’s services are best-in-class. The challenge has been demonstrating that its services can work for smaller-sized businesses. It has had some success in this regard by sponsoring boot camps where it brings in companies to provide opportunities to talk with its experts and see real-world examples of what its services can provide using its relatively new artificial intelligence platform (AIP). If Palantir can work to lower its service costs, it can open a more significant opportunity for the AI pioneer.

In the meantime, Palantir is demonstrating how economies of scale is helping its revenue increase and its operating losses decrease. Operating losses hit $625 million in 2018. In 2023, the business posted full-year operating income of $120 million.

Even with the huge price runup over the past year, Palantir stock still trades at a significant discount to valuations from a few years ago, and it offers big upside potential. At a forward price-to-earnings ratio of approximately 63, Palantir stock still looks cheap on a historical basis.

Don’t overlook the role data is playing in the AI revolution

Keith Noonan (Snowflake): Advanced processing power and well-honed algorithms are key ingredients in the AI revolution, but AI systems won’t actually produce much value if they’re not being trained on the right data. With that in mind, Snowflake stands out as a smart pick-and-shovel play for investors looking to capitalize on the rise of AI.

Snowflake (NYSE: SNOW) is a leading provider of data warehousing software and analytics tools. The company’s Data Cloud platform makes it possible for users to combine and analyze data that is generated across Amazon, Microsoft, and Alphabet‘s otherwise walled-off cloud infrastructure services. This makes it possible for the company’s customers to train AI systems and make operational decisions based on a much wider range of relevant data.

Recent earnings reports from Amazon and Microsoft show that AI is powering strong demand for cloud infrastructure services. While Snowflake’s share price has seen some positive momentum in conjunction with the encouraging numbers reported by these two cloud titans, the company’s stock still has explosive potential. The company’s share price is still down roughly 44% from its peak, and the market could be underestimating emerging tailwinds for the business.

On Feb. 28, Snowflake will report results for the fourth quarter of its 2024 fiscal year, which concluded at the end of January. The company expects product revenue to grow roughly 29.5% year over year and reach approximately $718.5 million in the period. Meanwhile, full-year product revenue is projected to come in at $2.65 billion — up 37% annually.

Snowflake is already posting impressive sales momentum, but the company is also still in the early stages of rolling out AI-focused services that should help drive long-term growth. The software specialist is expanding the availability of services that will help its customers build artificial intelligence applications, organize unstructured data that would otherwise be unusable, and improve the performance of large language models.

For its 2029 fiscal year, Snowflake expects to post a non-GAAP (adjusted) free cash flow margin of 30%. It also expects product revenue of $10 billion. That suggests product sales will grow at a roughly 30.4% compound annual growth rate over the next five years — actually accelerating from the growth that the business guided for in last year’s fourth quarter.

With the stock still down big from its high even though the broader market is in a bullish mode, investors have an opportunity to build a position in Snowflake at prices that leave room for very strong returns.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 5, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keith Noonan has no position in any of the stocks mentioned. Parkev Tatevosian, CFA has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, Palantir Technologies, and Snowflake. The Motley Fool has a disclosure policy.

A Bull Market Is Here: 2 Artificial Intelligence (AI) Growth Stocks Down 38% and 44% to Buy Right Now was originally published by The Motley Fool