Decline in job mobility bad for productivity and economic dynamism

The decline in job mobility is generally considered a bad thing for the economy.

When people change jobs, economists assume that, in general, it will be to a higher paying role more suited to a worker’s skill set, thus boosting productivity across the economy.

“Outside the post-pandemic jump, job mobility has trended downwards over multiple decades,” notes job website Indeed’s Asia-Pacific economist Callam Pickering.

“Australian workers today are more conservative in the job choice and more loyal to their employer than was common decades ago. It also suggests that the economy itself is less dynamic than it once was.”

So why are we staying put with our current employer?

Pickering says it’s not because of a lack of opportunity.

“The recent decline in job mobility is perhaps a surprise given that the Australian economy continues to create an incredible number of jobs,” he continues.

“There are plenty of opportunities available for those who want a new job. And we know that changing jobs is often the best way to get a substantial pay rise, which seems useful in a cost-of-living crisis.

“That suggests that Australians are more concerned about the job market and are more likely to prioritise job security over new opportunities, even if they are more highly paid.”

So, unless someone’s got something already lined up, they’re less likely to jump ship in the hope of finding a better job.

Key Event

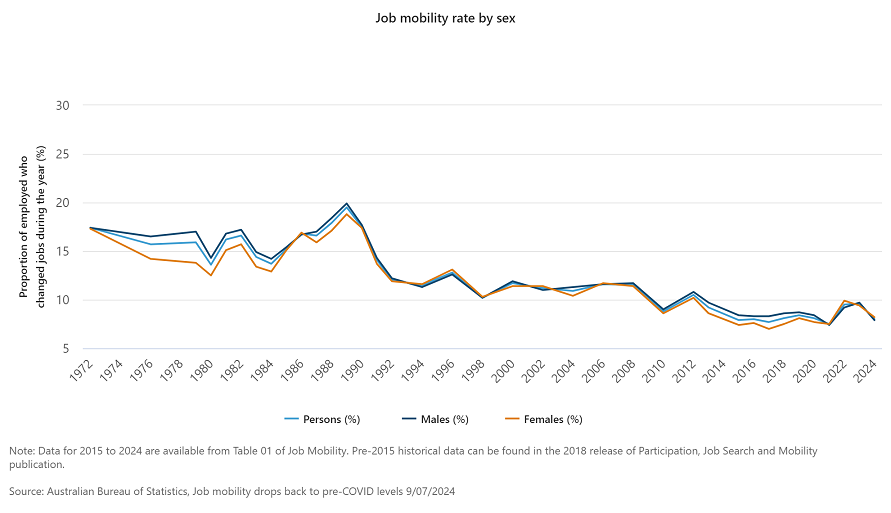

Job mobility falls back to pre-COVID levels as labour market gets tougher for workers

Some data out from the Australian Bureau of Statistics today highlights how things are becoming tougher for those looking for a job or to change jobs.

The data was collected in February and is an annual snapshot of labour mobility and “potential workers”.

First, on labour mobility, the proportion of workers switching jobs in the year to February 2024 fell for the first time in three years, slumping 1.5 percentage points back to about 8 per cent.

About 1.1 million people changed employer over that year, and the rate of job switching was back about pre-COVID levels.

Despite the reputation of younger generations flitting between employers, there’s been a structural downtrend in job switching since the late-1980s, with a further downward leg since the global financial crisis.

Younger workers have been a key driver of this trend, with 12.6% of 15 to 24-year-olds changing jobs, well down than the high of 15.9% in the pandemic and typical rates above 20% when you go back two decades.

It’s not surprising that workers are more reluctant to shift jobs, with more potential workers out there to compete against.

The ABS found there were 1.9 million “potential workers” in February 2024, up by about 100,000 from the same time a year earlier.

That’s despite only 555,000 being considered unemployed, which the ABS defines as available to start work and actively looking for it.

“Of the people who wanted to work, just over 1 million people were available to start work straight away, and an additional 483,000 people were available to start within four weeks but not immediately. The remaining 330,000 people said they weren’t going to be available for more than a month,” the ABS head of labour statistics Bjorn Jarvis noted.

The ABS data show there were 810,000 people in February 2024 who wanted to work, were available to start either immediately or within four weeks, but did not actively look for work.

The main reasons given were because people were attending an educational institution (197,000 people, or 24%), caring for children (112,000 people, or 14%), or had a long-term health condition or disability (98,000 people, or 12%).

Key Event

Business conditions ease, but confidence bounces: NAB

Business conditions edged down further in the month, continuing the long running trend since peaking in late 2022, according to NAB’s Monthly Business Survey for June 2024.

Business conditions fell 2pts to +4 index points and are now below the long-run average.

The fall was driven by declines in employment (down 6pts to 0 index points) and profitability indices (also down 1pt to +2 index points) while trading conditions were broadly flat at +10 index points (unrounded).

“Business conditions continued their now long running easing trend in June,” said NAB Head of Australian Economics Gareth Spence.

“They are now below average, reflecting the slowing in the economy through late 2023 and early 2024.”

“Of note is the sharp decline in the employment index in the month. While its only one month’s read, the employment index is now below its long-run average and may be signaling that the broader slowing in the economy is flowing through more strongly to labour demand.”

However, business confidence – driven by a broad-based increase across industries – rose sharply in the month to its highest level since early 2023.

Business confidence was up 6pts to +4 index points driven by an increase in 7 out of 8 industries.

The jump was led by increases in manufacturing and wholesale while the remaining industries saw 6pts+ increases except for construction which declined 3pts.

In trend terms, the goods distributions sectors – wholesale and retail – remain weakest and the only two industries in negative territory at -7 index points.

“Business confidence rose relatively sharply in the month and is now back into positive territory and at its highest level since early 2023,” Mr Spence said.

“Other activity indicators were mixed in the month. Forward orders were flat at -6 index points (unrounded) while capex fell 5pts to 0 index points. Capacity utilisation edged up and remains well above average at 83.5 per cent.

“Forward orders remain well into negative territory and have been there for some time.

“The key driver of weak forward orders over recent months have been the retail and wholesale sectors, though manufacturing weakened further in the month and is also now very weak.”

Labour cost growth eased to 1.8 per cent in quarterly equivalent terms (from 2.3 per cent in May) and purchase cost growth also eased to 1.3 per cent (from 1.7 per cent).

Product price growth fell to 0.7 per cent overall (from 1.1 per cent). Retail price growth was broadly stable at 1.5 per cent, while recreation & personal services prices fell to 0.7 per cent (from 1.1 per cent).

“Encouragingly, the key price and cost growth measures reversed their increase from last month,” Mr Spence said.

“That said, retail price growth was broadly stable and is high despite the weaker activity outlook and confidence in the industry. However, also important for consumer prices on the services side, recreation and personal services price growth fell back to 0.7 per cent on a quarterly basis.”

“Overall, our take on the survey is that it continues to signal another soft quarter in Q2.”

Key Event

Telstra share price lifts as it hikes prices on its mobile pricing plans

Telstra customers are set to pay more for mobile plans after the telecommunications giant announced price hikes.

Telstra shares closed flat yesterday, but in late morning trade, were up 2.3 per cent to $3.74.

The change in pricing will be introduced for postpaid customers from August 27 this year. The change for prepaid customers will come into effect from October 22.

Customers will be out between $2 to $4 per month, with premium plans set to have the highest price jump from $95 per month to $99 per month.

Basic plans will rise from $62 to $65, essential plans will rise from $72 to $75, and bundle plans will increase from $50 to $52.

Starter plan prices will remain unaffected by the price hikes, with the monthly rate staying at $50.

Telstra noted that over the past five years, network traffic on its mobile network has increased by around 3.5 times and continues to grow by 20 per cent a year.

To help manage this demand growth, the company invested $1.3 billion in mobile spectrum in FY 2024 to support more data and faster speeds.

As the company announced on May 21, its mobile plan will no longer be linked to an inflation-linked annual review.

“In making these price changes, Telstra has balanced cost of living pressures it knows some of its customers are experiencing, with its need to continue to invest to manage technology evolution and continued strong customer demand on its mobile network,” CEO Vicki Brady said in a statement to the ASX on Tuesday.

Telstra’s decision arrives after Optus hiked its postpaid mobile phone plans in May.

In May, Telstra announced it would sake about 10 per cent of its 31,000 strong workforce. More on that here:

Key Event

Consumer sentiment remains ‘deeply pessimistic’: Westpac

The Westpac–Melbourne Institute Consumer Sentiment Index dipped 1.1 per cent to 82.7 in July from 83.6 in June, with family finances again under pressure, and a big jump in interest rate rise expectations.

“Sentiment remains stuck in the same deeply pessimistic range that has dominated for two years now,” said Westpac senior economist, Matthew Hassan.

“The July update shows that fears of persistent inflation and further interest rate rises are again weighing more heavily on the consumer mood, offsetting any boost from the arrival of the stage 3 tax cuts and other fiscal support measures.

“While these measures came into effect from July 1, many consumers would not have seen any cash flow impacts so far given that payment cycles – for both incomes and for the electricity and rent expenses set to receive more cost of living support – are often fortnightly or monthly.”

The component indexes show the latest sentiment dip centered around family finances.

The sharpest fall was in the “family finances vs a year ago” sub-index, which dropped 8.4 per cent, giving back almost all last month’s promising 9.7 per cent lift.

At 63.5, the sub-index remains at “extremely weak levels”.

“Consumer expectations for their finances also deteriorated. The ‘family finances, next 12 months’ sub-index declined 4.5 per cent to 92.1, the weakest read since the end of last year,” Mr Hassan said.

“On a combined basis, the two sub-indexes tracking finances declined to their weakest level since November.”

Other components improved slightly, with consumers a little less pessimistic about the economic outlook and around attitudes towards spending.

The sub-index tracking assessments of the “economic outlook, next 12 months” rose 3.6 per cent to 81.4, while the “economic outlook, next 5 years” sub-index nudged up 0.5 per cent to 94.5.

The “time to buy a major item” sub-index lifted 3.1 per cent to 82.1 but remains well below its long-run average of 124.

The most striking move in the month was again around consumer views on the interest rate outlook.

The Mortgage Rate Expectations Index tracks consumer expectations for variable mortgage rates over the next 12 months.

It jumped 12.8 per cent in July, marking the steepest monthly rise since Westpac began running this question in every survey at the start of 2022.

The Index has surged 30 per cent in just three months, from a below-average read of 122.8 in April to 159.2 in July (the average historically is 143.8).

“That sudden hawkish turn is the sharpest we have seen in the last seven years,” Mr Hassan said.

“The detailed responses show about just under 60 per cent of consumers expect mortgage rates to rise over the next year.”

Key Event

Mining stocks among the best performers on the ASX

Many of today’s best performing stocks are in the resources sector.

Shares of Sims (+4.6%), Iluka Resources (+2.6%) and Arcadium Lithium (+2.4%) have risen sharply in morning trade.

Tech and communications stocks are also doing well, including Life360 (+2.2%) and Telstra (+2.1%).

On the flip side, today’s worst performers are uranium stocks Deep Yellow (-3.5%) and Boss Energy (-2.6%), along with the electronic payments company Block (-1.4%).

Key Event

ASX lifts 0.6 per cent, driven by tech and materials sectors

The Australian share market has begun its day moderately higher after Wall Street hit new record highs overnight.

The ASX 200 index was up 0.6% to 7,810 points, by 10:20am AEST (essentially clawing back much of yesterday’s losses).

Nearly every sector is trading higher, led by materials (+0.8%), tech (+0.8%) and financials (+0.7%).

The only sector to fall in morning trade is utilities (-0.3%).

Finance report: Kamala Harris’s odds of becoming next US president have improved

If you need a refresher about what happened on markets yesterday, here’s Alan Kohler’s finance report from the 7pm News.

Basically, the All Ords fell 0.7% yesterday as lower oil and iron ore prices weighed on resources stocks.

As usual, Alan included some nifty charts. One of them shows US Vice-President Kamala Harris is now seen as more likely than Joe Biden to get the top job, according to betting markets.

However, they trail well behind Donald Trump.

Key Event

Accused scammer Hassan Mehdi admits deleting crucial messages, accuses police of lying in $1.7m fraud case

A man accused of setting up a sham company used to steal $1.7 million from Australian scam victims has admitted deleting crucial messages and accused police of lying about messages they found on his phone.

The stunning testimony was given by Hassan Mehdi during days of tense cross-examination in a civil lawsuit in the NSW Supreme Court.

Mr Mehdi maintains his innocence but was pressed on whether he’d changed his story after the ABC broadcast new information, and whether he’d intentionally deleted messages, backdated documentation or withheld evidence of a bank account.

He’s a Melbourne-based Pakistani man who founded a business called Supercheap Security in 2021 and later created a bank account with NAB.

For more, here’s the story by Michael Atkin:

Key Event

Paramount Global and Skydance Media agree to multi-billion-dollar merger

Skydance Media and Paramount Global have agreed to merge, the companies announced late on Sunday, in the hopes of “energising” Paramount’s offerings.

Many of you may know Paramount as the studio behind The Godfather, Breakfast at Tiffany’s and a huge list of other films. It’s also the owner of Network 10 (the home of shows like MasterChef and The Project), and the streaming service Paramount+.

And in case you’re wondering, Skydance is a film production company founded by David Ellison (the son of Oracle co-founder Larry Ellison).

His company was Paramount’s financial partner on several major recent movies (including Top Gun: Maverick, Mission: Impossible — Dead Reckoning and Star Trek Into Darkness).

The merger is quite complex and involves a few steps.

Firstly, Skydance and its deal partners will purchase a company called National Amusements (which holds the Redstone family’s controlling stake in Paramount) for $US2.4 billion in cash.

Skydance will then merge with Paramount, offering $US4.5 billion in cash or stock to shareholders.

It will also provide an extra $US1.5 billion for Paramount’s balance sheet.

Shares of Paramount fell 5.3% to $US11.18 overnight. (Those are the ‘Class B’ shares, which don’t come with any voting rights).

The ‘Class A’ shares are owned by the Shari Redstone and her family (through their company National Amusements).

For more info, you can read the ABC’s article here:

Why the Australian dollar is at a 33-year high against the Japanese yen

Have you ever wondered why the Japanese yen is so weak? (It’s sitting at its lowest level in more than 30 years against major currencies).

You may also be surprised to hear the Australian dollar is near a six-month high against the greenback — and that there is increasing pressure for the Reserve Bank to lift interest rates next month.

Well you don’t need to wonder for too much longer.

I spoke with NAB’s head currency strategist Ray Attrill last night (during my stint as the guest host of The Business), and he helped answer all those burning questions!

You can listen to his full insights here:

Why the global fossil fuel sharks are circling Australia’s gas export industry

For an industry entering its sunset years, Australian gas certainly is attracting an enormous amount of attention and money.

Last week, that great laggard of the investment world, Santos, was rumoured to be in the sights of two of the world’s biggest fossil fuel outfits, Saudi Arabia’s Aramco and the UAE’s Abu Dhabi National Oil Company, in a potential $25 billion break-up.

Late last year, Australian giant Woodside approached the group as well, proposing an $80 billion merger that would have catapulted the pair into the top tier of global petrochemical giants. But the deal went nowhere.

And for much of 2023, two huge North American investment groups sought to capture Origin Energy in a $20 billion deal that would have split the Australian energy giant.

The ABC’s chief business correspondent Ian Verrender explains what is behind this renewed global interest in Australian gas:

Will shoppers pay the price with an interest rate hike from the RBA?

Australia’s struggling retail sector has been given a glimmer of hope, with rolling sales encouraging shoppers to spend — but economists warn that it may come with the price of another interest rate hike by the Reserve Bank.

The recent jump in retail spending, boosted by clothing and footwear retailers offering big discounts and earlier-than-usual sales seasons, has increased expectations of an interest rate hike in August as the entire retail sector navigates a cost-of-living crunch.

Official figures released by the Australian Bureau of Statistics last week showed retail spending rose by 0.6 per cent in May, while spending only increased by 1.7 per cent for the year.

Most of the increase was in clothing and footwear, with customers being enticed to spend their cash with retailers offering big discounts and longer — or more frequent — sales.

For more, here’s the story by Kate Ainsworth and Daniel Ziffer:

Key Event

ASX to rise, Wall Street advances to its highest levels ever (again)

Good morning! I’ll be guiding you through the latest business and economic news.

The local share market is expected to begin its day slightly higher (with ASX futures up 0.3%).

The Australian dollar is marginally weaker at 67.4 US cents.

In economic news, some interesting economic data will be released in a few hours.

One of them is about consumer confidence (which has fallen to extremely pessimistic levels, according to Westpac and the Melbourne Institute).

And the other is about business confidence, which (according to NAB) is sitting at more optimistic levels, relatively speaking.

Those figures will provide some clue on how the economy will track for the rest of the year.

More record highs on Wall Street

It’s likely to follow a (mostly) positive session from Wall Street, during which the S&P 500 and Nasdaq Composite hit new record highs overnight (even though they rose by just 0.1% and 0.3% respectively).

US markets were driven higher by tech stocks, including Nvidia (+1.9%), Intel (+6.2%) and Advanced Micro Devices (+4%).

The Dow Jones index, however, slipped by 0.1%, while European markets were flat.

Essentially, investors are in “wait and see” mode. They’re resisting the urge to make big bets until they’ve heard from Federal Reserve chair Jerome Powell, who will deliver his semi-annual testimony to US Congress on Tuesday and Wednesday (local time).

They’re waiting for Powell to provide more clarity on how soon an interest rate cut might happen.

Traders have increased their bets that the US central bank will cut rates in September.

The odds have risen to 73.6% (up from 72.2% on Friday, and 59.8% a week ago), according to CME Group’s FedWatch tool.

Markets are also waiting for the US to release its latest consumer price report (on Thursday, local time).

Economists are anticipating headline inflation in the US will to slow to 3.1% (in the year to June).

And later this week, some major banks (ie. Citigroup, JP Morgan and Wells Fargo) will release their June-quarter financial results. So there’s a lot to look out for!

Oil and gold slump

In commodity markets, oil futures fell sharply after Hurricane Beryl shut US refineries and ports along the Gulf of Mexico.

Also, hopes for a ceasefire deal in Gaza appeared to reduce worries about global crude supply disruptions.

Brent crude dropped 1% to $85.68 per barrel.

In precious metals, gold slipped 0.9% on bets the Fed would start cutting US interest rates in September.

Market snapshot

- ASX SPI futures: +0.3% to 7,771 points

- ASX 200 (Monday close): -0.8% to 7,763 points

- Australian dollar: -0.2% to 67.35 US cents

- Wall Street: Dow Jones (-0.1%), S&P 500 (+0.1%), Nasdaq (+0.3%)

- Europe: FTSE (-0.1%), DAX (flat), Stoxx 600 (flat)

- Spot gold: -1.4% to $US2,359/ounce

- Brent crude: -1% at $US85.68/barrel

- Iron ore: -1.7% to $US108.50/tonne

- Bitcoin: -0.2% to $US56,524

Prices current to 7:30am AEST.