Which are the best buys among Alphabet (Google), Amazon, Meta Platforms (Facebook), Tesla, Apple, Nvidia, and Microsoft?

The “Magnificent Seven” stocks have made investors lots of money in recent years. This is an elite group of tech companies that are growing at double-digit rates and generating billions of dollars in profit to invest in growth initiatives, including artificial intelligence (AI) technology.

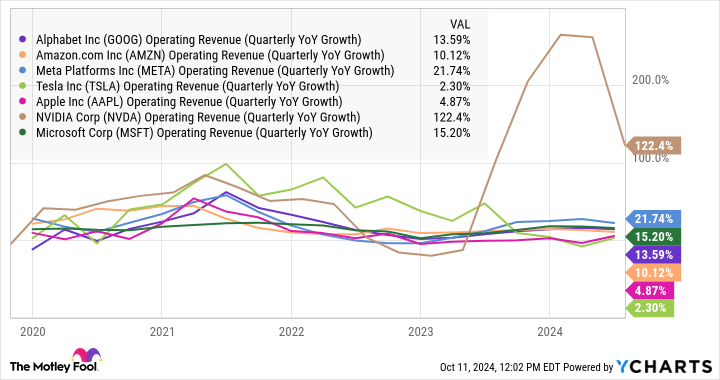

If you’re wondering which of these top stocks will perform best over the next few years, start by comparing their underlying business growth. Companies that deliver the highest growth in revenue and earnings will generally deliver the best returns over time.

Moreover, the two fastest-growing companies in the group right now happen to trade at reasonable price-to-earnings (P/E) ratios that could set up stellar returns. Here are the two Magnificent Seven stocks I would buy right now.

1. Nvidia

Nvidia (NVDA -4.69%) makes the essential computing hardware that’s required for processing and training sophisticated AI models in data centers. It has virtually cornered the market for AI accelerators, or graphics processing units (GPUs), which has driven Nvidia’s revenue growth to triple-digit rates and driven tremendous returns for shareholders.

Compared to the rest of the Magnificent Seven, Nvidia’s revenue growth tops the chart. The AI chip leader reported a 122% year-over-year revenue increase in the most recent quarter. While growth is decelerating from these lofty rates, analysts still expect Nvidia to post 42% revenue growth next year, which also beats the other Magnificent Seven stocks.

Data by YCharts.

Data centers will always need more powerful processors, and Nvidia has tremendous resources to invest in new technology to keep its lead. It has spent a whopping $45 billion in research and development over the years, directed toward making the most powerful GPUs. That investment has resulted in monstrous returns for shareholders.

Nvidia’s lead in AI chips is attracting competition. For example, large cloud service providers, which are Nvidia’s largest customers, are making their own custom AI chips. While these chips still aren’t a viable replacement for the horsepower of GPUs for AI workloads, investors should be aware that the market for AI chips is evolving and could present potential obstacles to Nvidia’s growth at some point.

The constant threat to Nvidia’s leadership explains why management has invested in expanding the business beyond GPUs. It acquired Mellanox in 2020, which basically turned Nvidia into more of a data center solutions company by expanding into networking hardware, such as high-performance ethernet adaptors and interconnect products. Nvidia’s networking revenue grew 114% year over year last quarter to reach $3.7 billion. The more this segment grows, the wider Nvidia’s competitive moat will become.

Nvidia has built a strong brand across several computing markets, including gaming, that people associate with high performance. The company’s upcoming Blackwell computing platform will provide a significant boost in AI performance for the most demanding workloads. Tesla, xAI, Amazon Web Services, and Microsoft are some of the top AI companies expected to adopt Blackwell in their data centers.

Analysts project Nvidia’s earnings to grow at an annualized rate of 36% in the coming years, which is also higher than the other Magnificent Seven companies. With the stock trading at a forward P/E of 34, based on next year’s earnings estimate, investing in Nvidia today could lead to market-beating returns in 2025.

2. Meta Platforms

Facebook and Instagram owner Meta Platforms (META -0.70%) is another fast grower that could significantly outperform its Magnificent Seven peers. The company has posted impressive growth this year, but its shares still trade at a reasonable valuation.

The digital-ad recovery over the last year helped boost Meta’s revenue by 22% year over year in the second quarter. This is the second-highest rate of growth among the Magnificent Seven. Meta is proving it can successfully enhance its advertising business with AI, where it has purchased loads of Nvidia GPUs to power its AI infrastructure.

The company introduced its Llama family of large language models in February 2023 and hasn’t looked back. Revenue growth has doubled, compared to a year ago, and it’s investing in new AI features, like Meta AI for its social media platforms, while keeping tight control of operating costs. Disciplined cost management helped drive earnings per share up 73% year over year in Q2.

AI improvements to Meta’s Advantage+ advertising tool is leading to better ad delivery and efficiency. The company says these new tools are driving a 22% higher return on ad spending for U.S. advertisers, which explains why the company is enjoying such strong momentum in revenue growth.

Meta is clearly going to benefit tremendously in the AI era. It has generated $49 billion in trailing free cash flow, which provides ample ammunition to be a leader in AI. Its technology investments, combined with 3.27 billion people who use its apps every day, should lead to plenty of growth in the $699 billion digital ad market.

Analysts forecast Meta’s earnings to grow at an annualized rate of 19% over the next several years, which currently ranks third among the Magnificent Seven. But its forward P/E of 23, based on next year’s earnings estimate, is also one of the lowest of the group, which should help the stock outperform the broader market. Assuming Meta meets these earnings estimates, the stock could double investors’ money within four years.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Ballard has positions in Meta Platforms, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.