Investors looking for a growth stock may be tempted to buy this company, but they shouldn’t ignore one key factor.

Data streaming platform provider Confluent (CFLT -1.62%) is seeing a remarkable turnaround in its fortunes on the stock market of late. After rising rapidly earlier in 2024, the stock started going downhill and was underperforming the broader technology sector recently, but it has made a huge jump since the beginning of October.

More specifically, Confluent stock is up 45% since Oct. 1 (as of this writing). This parabolic move, a scenario that refers to the rapid increase in the stock price of a company in a short time (identical to the right side of a parabolic curve), seems to have gained momentum following the release of the company’s third-quarter 2024 results on Oct. 30.

Confluent’s healthy growth seems sustainable thanks to a huge addressable market

Confluent’s Q3 revenue came in at $250 million, an increase of 25% from the same period last year, of which $240 million was from subscriptions. The company’s non-GAAP (adjusted) net income jumped fivefold on a year-over-year basis to $0.10 per share. The numbers were well ahead of Confluent’s Q3 guidance of $0.05 per share in adjusted earnings on $233.5 million in subscription revenue.

Even better, Confluent raised its full-year guidance and now expects to finish the year with $917 million in subscription revenue and $0.25 per share in adjusted earnings. It was earlier expecting $910 million in subscription revenue for the year along with $0.20 per share in earnings. The beat-and-raise quarterly report explains why Confluent stock jumped more than 13% on Nov. 1.

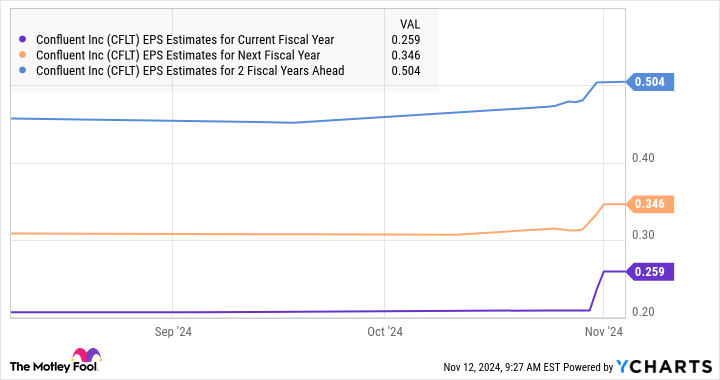

The updated guidance means that Confluent is on track to deliver 20%-plus revenue growth in 2024, while its earnings would increase significantly from last year’s reading of $0.04 per share. Even better, Confluent is expected to maintain impressive earnings growth levels for the next couple of years as well.

CFLT EPS Estimates for Current Fiscal Year data by YCharts

What’s more, analysts forecast its earnings will increase at a compound annual growth rate (CAGR) of 125% for the next five years. The reason why Confluent is expected to clock such eye-popping growth is because of the huge total addressable market (TAM) it is sitting on. The company’s TAM stood at $60 billion at the end of 2022, a number that’s expected to hit $100 billion in 2025.

Confluent’s cloud-based data streaming platform allows customers to connect, process, and govern their data in real time as compared to the traditional method of first storing data in silos and processing it in batches later on. The good part is that Confluent’s data streaming platform has been gaining solid traction among customers.

The company witnessed a 16% year-over-year increase in its customer base in Q3, ending the quarter with 5,680 customers. More importantly, Confluent’s dollar-based net retention rate stood at 117% last quarter. This metric compares the annual recurring revenue (ARR) of Confluent’s customers at the end of a quarter to the ARR from the same customer set in the year-ago period. So, a reading of over 100% in this metric is an indication that Confluent’s existing customers increased their spending on the company’s offerings.

Confluent, therefore, is not only attracting new customers but also winning a bigger share of their wallets. As such, the company seems to be on the right track to make the most of the multibillion-dollar end-market opportunity it is sitting on.

But what about the valuation?

As I mentioned, Confluent expects to finish 2024 with $0.25 per share in earnings. Assuming the company does hit that mark, it is now trading at 109 times 2024 earnings (using the current share price). Moreover, the earnings forecast of $0.35 per share for next year will put its forward earnings multiple at 78.

These multiples are expensive when you consider that the tech-heavy Nasdaq-100 sector has a forward earnings multiple of less than 31. Of course, Confluent’s bottom line is growing at an incredible pace, and it may be able to justify its expensive valuation, but the company will have to ensure that it maintains its outstanding levels of growth.

Yahoo! Finance puts Confluent’s price/earnings-to-growth ratio (PEG ratio) at just 0.62 based on the 125% annual earnings growth that it is forecast to deliver over the next five years. A PEG ratio of less than 1 indicates that a stock is undervalued with respect to the growth it is expected to deliver. So, investors looking for a growth stock can still consider buying Confluent, though they need to remember that it will have to continue clocking high levels of bottom-line growth to sustain its parabolic move.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool recommends Confluent. The Motley Fool has a disclosure policy.