Barclays launched coverage on WESCO International (NYSE:WCC), highlighting the company’s expansion potential in data centers, industrial automation, and its technology-driven push for operational improvement. The coverage brought more investor attention to WESCO’s evolving business model.

See our latest analysis for WESCO International.

WESCO’s digital initiatives and fresh analyst attention have drawn eyes to the stock, but investors have already been rewarded with a 20.4% total shareholder return over the past year and a massive 360% total return over five years. While the shares pulled back 6.2% in the last day, the broader momentum points to long-term confidence building behind WESCO’s evolving business model.

If you’re curious about what else is gaining traction in the industrial world, now is a great opportunity to broaden your search and discover fast growing stocks with high insider ownership

With analyst optimism and recent digital transformation fueling investor enthusiasm, the key question now is whether WESCO’s growth prospects are undervalued by the market or if investors have already priced in the company’s future momentum. Could there still be a buying opportunity, or is all the good news already reflected in the share price?

Most Popular Narrative: 13.6% Undervalued

With the most widely followed narrative suggesting WESCO’s fair value sits at $241, the recent close of $208.29 is being viewed as a meaningful discount. This spread encourages a closer look at the assumptions and catalysts shaping analysts’ bullishness.

Massive acceleration in data center spend, especially from hyperscale and AI-related builds, is driving outsized growth (+65% YoY in Q2; outlook increased from +20% to +40% for 2025). WESCO has deep end-user relationships and an expanding role in both white space and gray space of data centers. This positions the company to capture a multi-year expansion in its addressable market, which could lift revenue growth, operating leverage, and backlog visibility.

What is supercharging this valuation? Forecasted margins are pointing higher, revenue is climbing in strategic areas, and earnings estimates are typically reserved for fast-growth sectors. Hungry to see the precise financial leaps expected and the number that sets this target apart? Dive into the narrative for the full story.

Result: Fair Value of $241 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, industry-wide pricing pressure and delays in large-scale data center projects could still threaten WESCO’s margin growth and investor expectations.

Find out about the key risks to this WESCO International narrative.

Another View: What Does Our DCF Model Say?

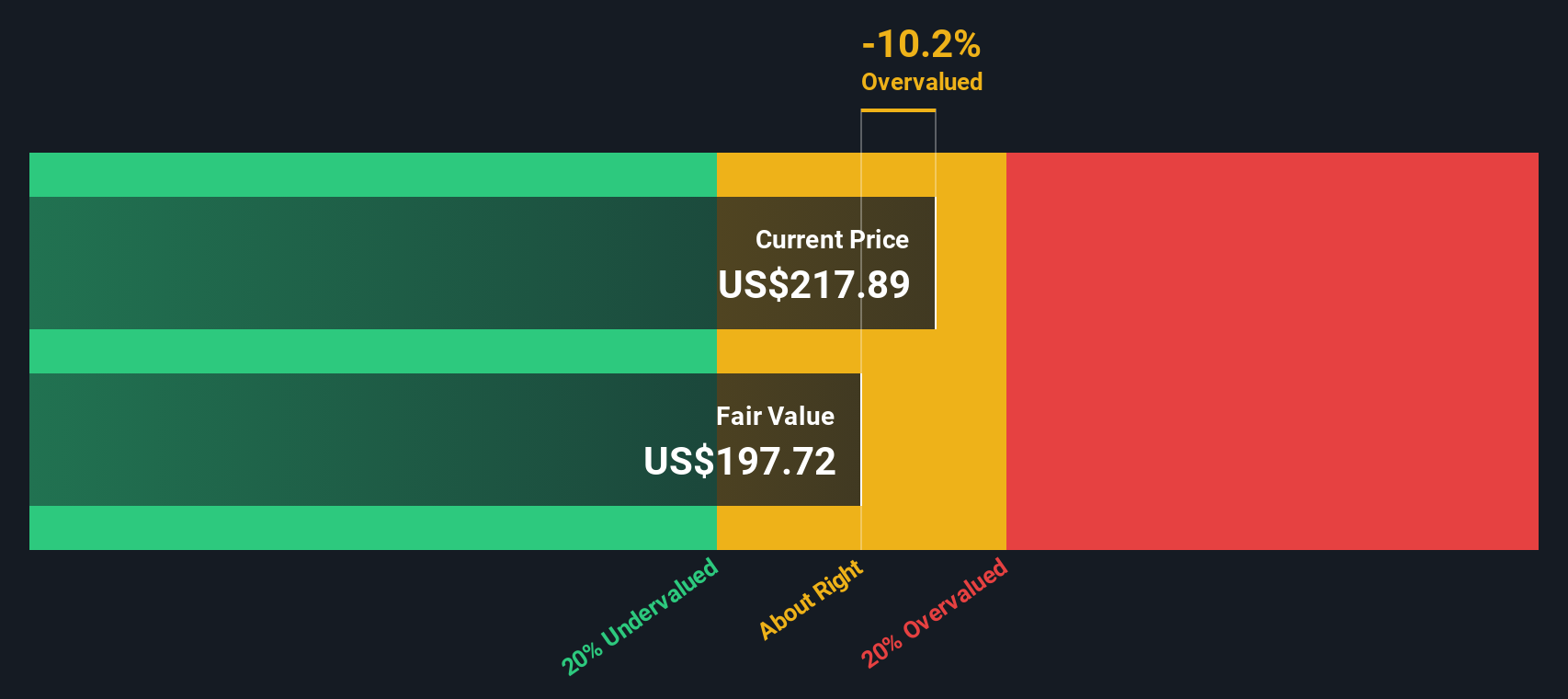

While analysts see WESCO International as undervalued using future earnings estimates, our DCF model presents a different perspective. According to the SWS DCF model, WESCO’s shares are trading above the calculated fair value, indicating less potential for upside if cash flow assumptions are not met. It raises the question of whether optimistic price targets are already fully reflected in the current price.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out WESCO International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own WESCO International Narrative

If you want to dig deeper, explore the numbers for yourself and quickly shape your own investment story based on the data in just a few minutes. Do it your way

A great starting point for your WESCO International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors always keep their edge by staying alert to where the next big moves are happening. Take the next step and check out these powerful opportunities before the market catches on.

- Boost your portfolio’s income potential and tap into reliable cash flows by checking out these 19 dividend stocks with yields > 3% with yields above 3%.

- Take advantage of the rapid rise of artificial intelligence by reviewing these 24 AI penny stocks that are reshaping key industries and driving future growth.

- Capture deep value opportunities you might be missing by seeking out these 891 undervalued stocks based on cash flows that the market hasn’t fully appreciated yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if WESCO International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)