Service Corporation International (SCI) has been in focus after its latest quarter showed 4.4% year on year revenue growth, topping analyst expectations by 1.5%, while recent positive Wall Street coverage has added another layer of investor attention.

See our latest analysis for Service Corporation International.

The share price, which closed at $82.35, has had a 5.3% 30 day share price return and a 6.7% year to date share price return. The 5 year total shareholder return of 66.1% points to momentum that has been supported recently by quarterly earnings, fresh analyst coverage and a higher dividend.

If you are weighing SCI against other opportunities in consumer facing services, it can also be helpful to scan beyond one name and consider fast growing stocks with high insider ownership.

With the shares already up this year, a 19.7% intrinsic discount and analysts pitching higher price targets, the key question now is whether SCI still trades below fair value or if the market is already pricing in future growth.

Price-to-Earnings of 21.6x: Is it justified?

Service Corporation International is trading on a P/E of 21.6x, which sits above both its Consumer Services peers and the level our fair value work suggests.

The P/E ratio compares the current share price to earnings per share, so a higher multiple often reflects investors paying up for each dollar of profit. For a deathcare business with established operations in the US and Canada, that kind of premium usually implies investors expect steady profitability and cash generation to continue.

Here, the 21.6x P/E stands well above the US Consumer Services industry average of 16.9x and also above the peer group average of 13.6x. It is slightly ahead of the estimated fair P/E of 20x, a level the market could move toward if sentiment cools and earnings expectations do not change.

Explore the SWS fair ratio for Service Corporation International

Result: Price-to-Earnings of 21.6x (OVERVALUED)

However, a richer P/E and reliance on continued analyst optimism leave the shares exposed if earnings growth slows or if sector sentiment turns more cautious.

Find out about the key risks to this Service Corporation International narrative.

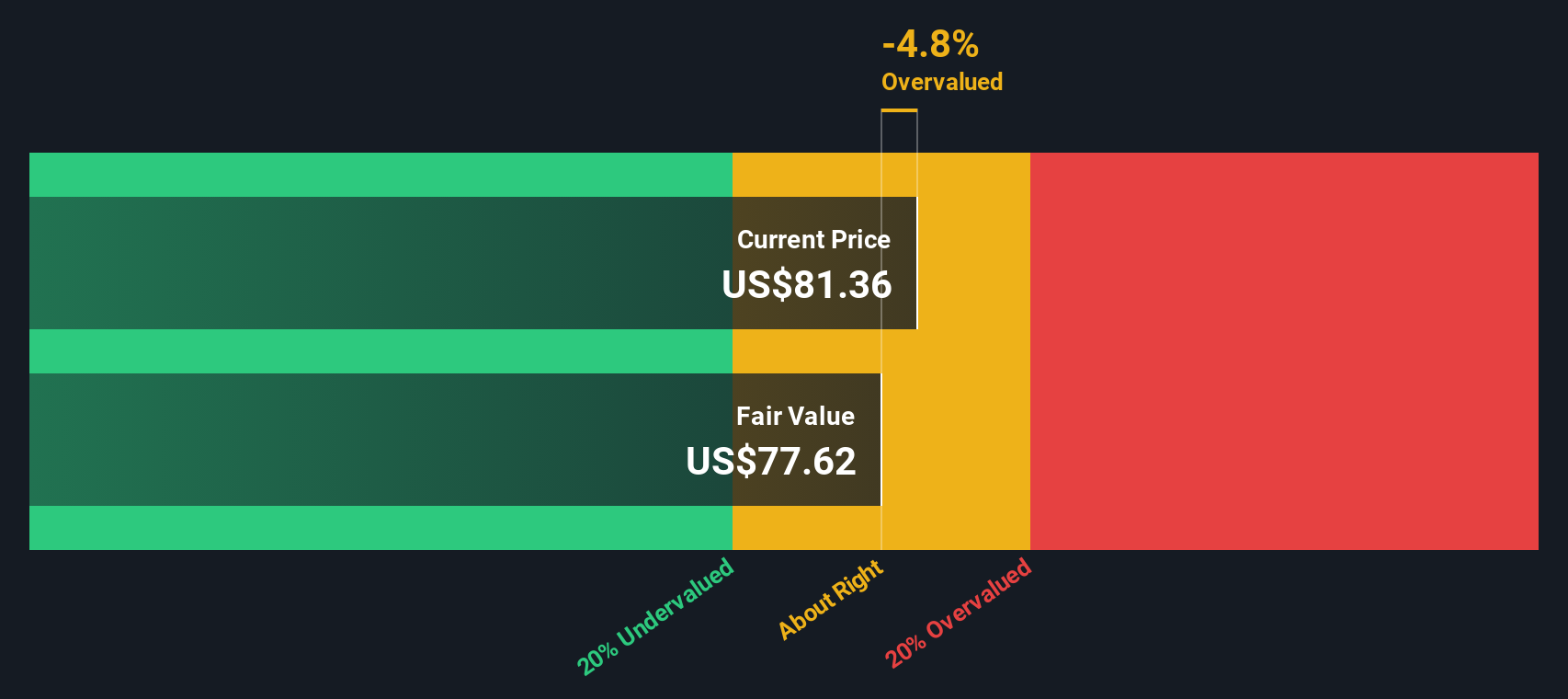

Another View: Discounted Cash Flow Suggests Upside

While the 21.6x P/E points to SCI looking expensive against peers, our DCF model paints a different picture. On that measure, the shares trade at about a 19.7% discount to an estimated fair value of US$102.53, which suggests the market price may be more cautious than the cash flow math.

For you as an investor, that tension between an expensive earnings multiple and a discount on our DCF work raises a simple question: which lens do you trust more when short term sentiment and long term cash generation do not fully line up?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Service Corporation International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own Service Corporation International Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own view against the data, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your Service Corporation International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. Use the screener to quickly surface other ideas that match your style.

- Hunt for potential mispriced opportunities by scanning these 874 undervalued stocks based on cash flows that align with your preferred risk and return balance.

- Target income focused ideas by checking out these 13 dividend stocks with yields > 3% that may complement a long term, cash flow driven approach.

- Get ahead of emerging themes by reviewing these 19 cryptocurrency and blockchain stocks that are tied to digital assets and blockchain technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com