The excitement around artificial intelligence (AI) is fueling the markets to new heights. Both the S&P 500 and Nasdaq Composite have eclipsed new records in just the first few months of the year.

Much of these gains are thanks to the “Magnificent Seven” — a catchy moniker used to describe the world’s largest companies including Microsoft, Apple, Nvidia, Alphabet, Amazon, Tesla, and Meta Platforms. But savvy investors understand that there are plenty of other opportunities in the AI realm besides megacap tech.

One company that’s emerging as a leader is big data analytics software company Palantir Technologies (NYSE: PLTR). 2023 was a breakout year for the company as it released its fourth major product: the Palantir Artificial Intelligence Platform (AIP).

AIP’s smashing success helped accelerate Palantir’s revenue and profits — and investors took notice. But with shares up nearly 180% in the last year, is it too late to buy the company’s stock?

Wedbush Securities analyst Dan Ives thinks the stock has much more room to grow. His price target of $35 per share implies roughly 59% upside from the company’s current trading levels, as of market close on April 10.

Read on to discover why scooping up shares in Palantir could be a lucrative opportunity right now.

The rise of the Palantir Artificial Intelligence Platform

For many years, Palantir sold three core software products: Apollo, Gotham, and Foundry. But last April, it quietly announced its foray into artificial intelligence (AI) following the release of AIP. But AIP’s launch was largely overshadowed by the moves big tech was making — including investments in ChatGPT developer OpenAI and its competitors.

In order to spread the word about AIP, Palantir resorted to a creative lead generation strategy. Namely, the company began hosting immersive seminars called “boot camps.” During these sessions, prospective customers were able to demo Palantir’s various software platforms. The idea behind this was to show off Palantir’s tech chops in a tangible way while simultaneously helping business leaders identify and form a use case surrounding artificial intelligence (AI).

Since the beginning of this campaign, Palantir has hosted over 850 boot camps. Moreover, AIP customers have publicly demonstrated how the product is being used to uncover new insights across myriad applications.

While AIP has only been commercially available for about a year, its initial success is encouraging. Palantir increased its customer count by 35% year over year in 2023 and is making progress in the private sector. During the fourth quarter alone, the company grew its U.S. commercial revenue operation by a sizzling 70%.

The journey is just getting started

Sure, accelerating revenue is always nice to see. For Palantir, it’s particularly meaningful because the company has gotten some pushback from Wall Street skeptics over the years — many of whom see the company as too reliant on lumpy government deals with the U.S. Military and its Western allies.

However, AIP is proving that Palantir has legitimate tech capabilities that are attracting customers from a whole host of industries outside of the public sector. Considering big tech’s pulse within the overall AI landscape, Palantir is proving that it can compete with the biggest companies.

I see 2023 as the first chapter in a long story in the AI narrative for the company. It’s moving fast, and other behemoths in tech are eager to work with Palantir AIP. It’s well-positioned to continue generating robust revenue growth while maintaining a healthy profitability profile and strong balance sheet.

A premium valuation that’s well worth the price

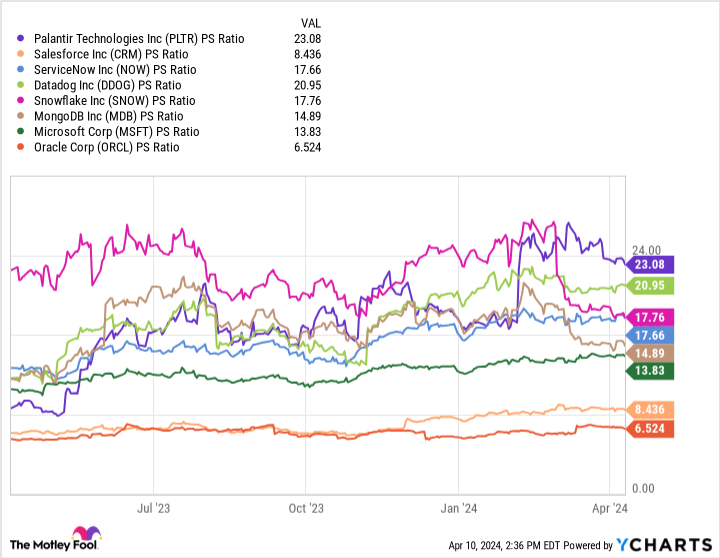

The chart below illustrates Palantir benchmarked against a cohort of other leading AI software-as-a-service (SaaS) businesses on a price-to-sales (P/S) basis. At a P/S of 23.1, Palantir is the most expensive stock among this peer set, based on that metric.

Palantir’s valuation multiples expanded dramatically following its jaw-dropping fourth-quarter earnings report in February. Since then, the stock has experienced some momentum and is only now starting to take a breather.

Further, it’s not just revenue growth that’s impressive for Palantir. The company’s entire financial picture is strong. The success of the boot camps has allowed Palantir to keep expenses in sales and marketing relatively low. As such, the company is consistently profitable — unlike many of its competitors.

In 2023, Palantir expanded its operating margin by 6%. This dropped right to the bottom line, as the company generated $730 million of free cash flow in 2023 — up more than threefold year over year.

With shares trading at such a premium compared to the competition, investors may be tempted to sell and book some profits. But I’d encourage investors to zoom out and look at the bigger picture.

While AIP has served as a catalyst for Palantir’s business and played an influential role in the excitement pushing the stock higher, the company’s shares are still down 40% from their all-time highs. Now is a terrific time to scoop up shares, as Palantir continues taking advantage of the long-term secular themes in AI.

Using dollar-cost averaging is a prudent strategy to initiate a position or add to an existing one. With so much potential upside, it’s hard to glance over Palantir.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $540,321!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 8, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Palantir Technologies, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Datadog, Meta Platforms, Microsoft, MongoDB, Nvidia, Oracle, Palantir Technologies, Salesforce, ServiceNow, Snowflake, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

A Once-in-a-Generation Investment Opportunity: 1 Top Artificial Intelligence (AI) Stock to Buy Hand Over Fist in April Before It Surges 55%, According to 1 Wall Street Analyst was originally published by The Motley Fool