Good morning, investors. Phil here, writing to you from Manhattan.

It surprises me how many investors I speak with still believe AI is an outright bubble, or that dot-com comparisons continue to hold weight.

A year ago, you could have organized the data in a way that supported that view, but it’s become dramatically harder to defend over the last six months.

The numbers tell the story.

Rotating valuations

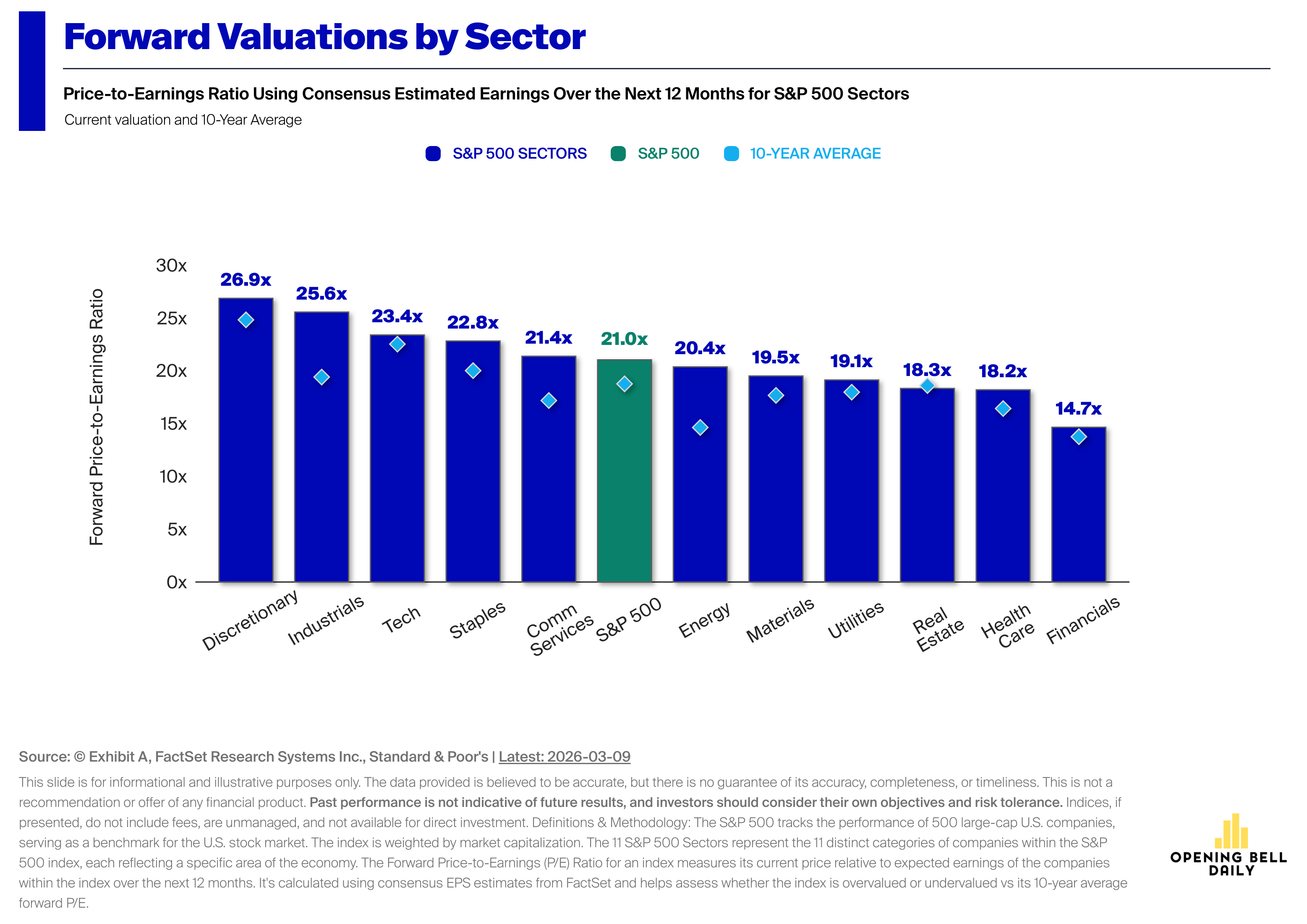

You can’t blame the Magnificent 7 for a pricey stock market anymore.

For years, investors pointed to Big Tech as the reason for the S&P 500’s premium valuation, but the data now tell a different story.

As it turns out, technology is just one of two sectors — alongside real estate — trading below historical norms.

According to DataTrek Research, all other S&P 500 sectors remain above their five-year average valuation, with the benchmark itself trading at a 6% premium against its recent history.

Technology, meanwhile, currently hovers at a 9.3% discount against its last five years.

In other words, the market’s most frothy valuations have spread well beyond Silicon Valley.

The sector that takes the most criticism for driving froth and bubbles is actually cheaper than the rest of the market.

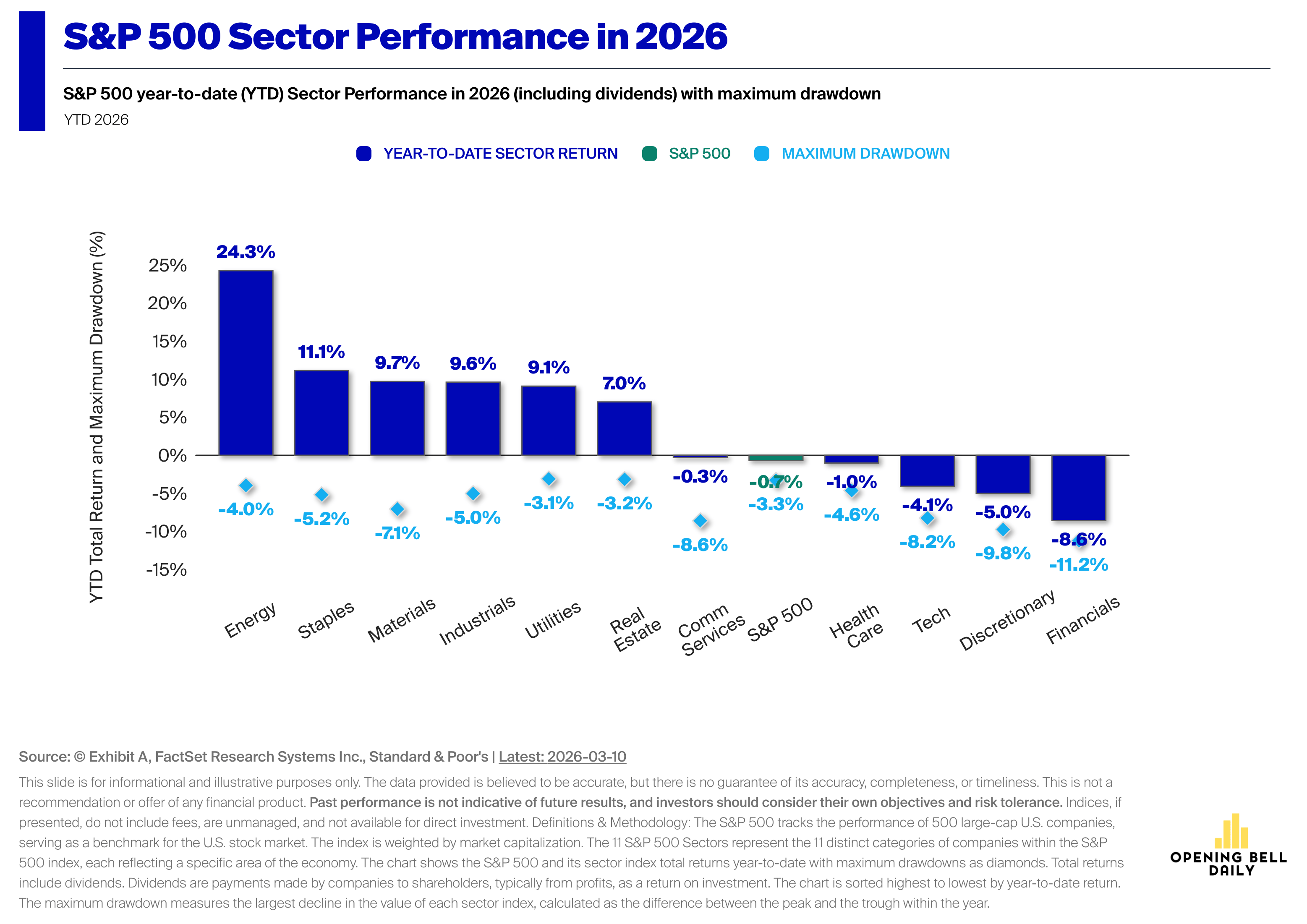

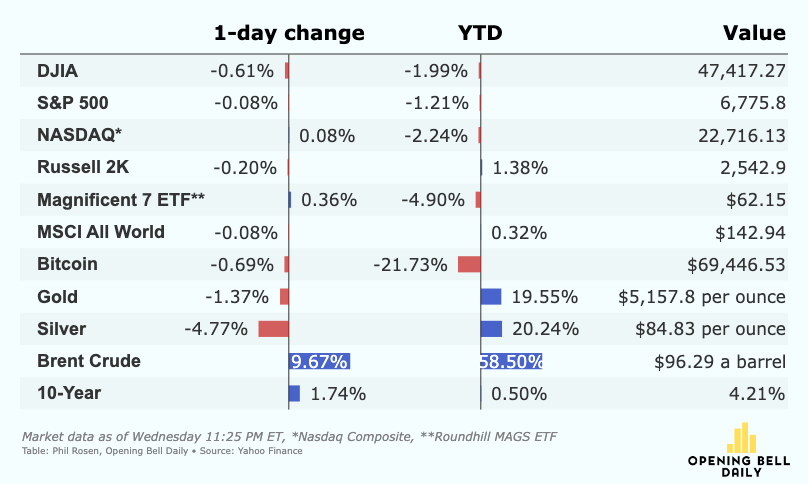

The S&P 500 remains negative year-to-date (Chart courtesy of Exhibit A)

Elevated multiples have instead rotated elsewhere.

Industrials, communications services, consumer discretionary and consumer staples all trade above their five-year averages, DataTrek’s report shows.

Commodity sectors like energy and materials, too, command richer valuations than just a few years ago.

Tech is still the third highest sector by forward valuations (Chart courtesy of Exhibit A)

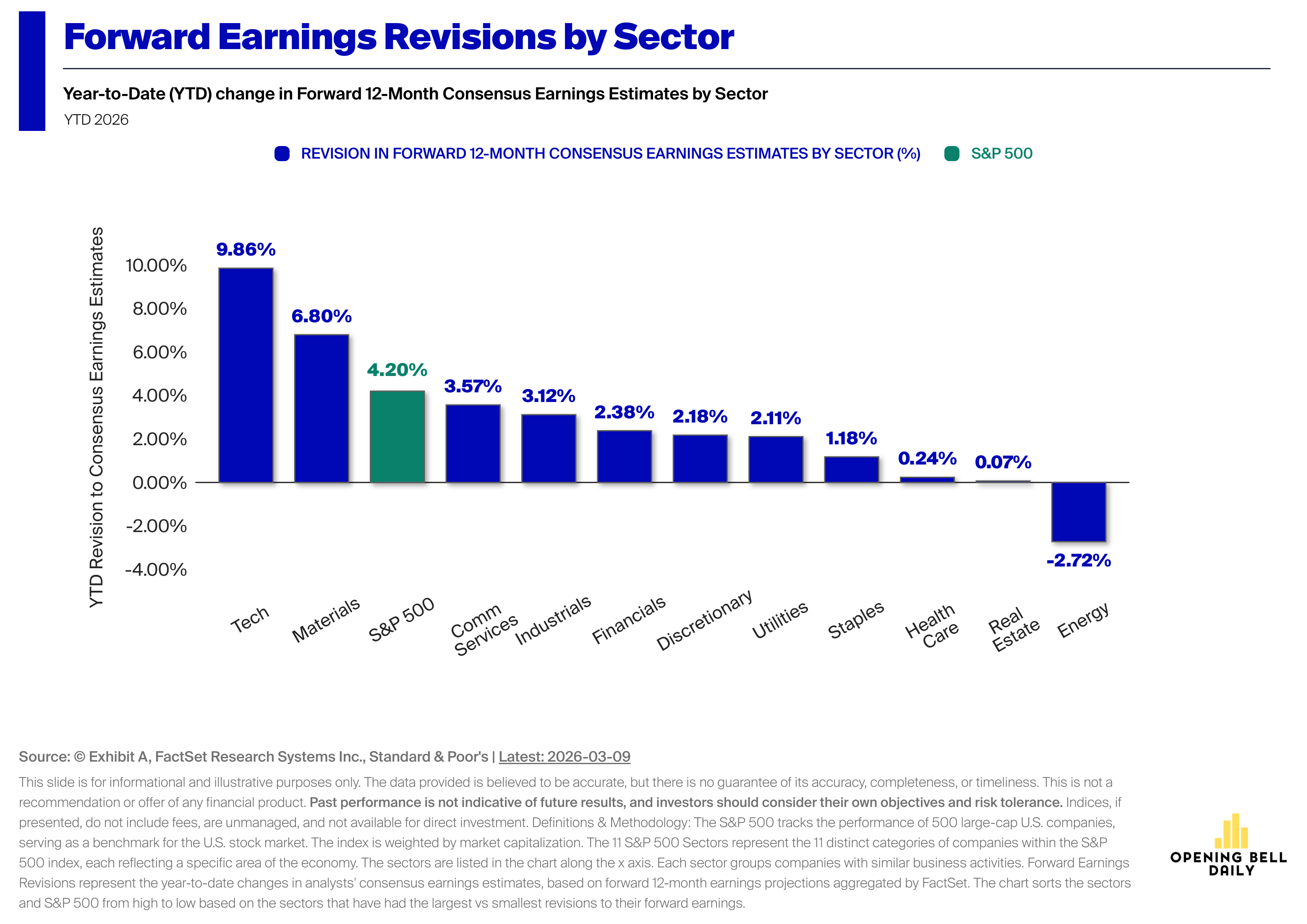

The wrinkle here is that even as valuations remain elevated, analysts have started to trim earnings expectations for the start of 2026.

Revenue forecasts, though, have actually climbed across most sectors.

Energy sees the weakest forward earnings revisions (Chart courtesy of Exhibit A)

That combination implies companies anticipate steady demand but rising costs, which could ultimately compress profit margins.

To put it plainly, the market — even with cheap Big Tech — is still relatively expensive even as near-term expectations deteriorate.

📈 Brent crude returned to $100 a barrel overnight. Oil prices climbed once again late Wednesday even after the IEA announced the largest emergency release of crude reserves in history. (CNBC)

🇺🇸 President Trump vowed to finish the job in Iran. He shrugged off rising oil prices and said the release of reserve crude will help ease prices at the pump. Markets, however, remain volatile. (Bloomberg)

🏆️ The Best Ideas Club portfolio is up 30% in 12 months. That dominates the S&P 500’s 18% return in the same period. We send one high-conviction stock pick per week to members, who also gain access to our AI-powered investment dashboard. Unlock our market-beating portfolio.

-

The White House launched Section 301 trade probes into Mexico, China and EU (CNBC)

-

Iraq’s state oil marketer said two tankers were attacked in Iraqi waters (Bloomberg)

-

Software’s worst sell-off in decades looks overblown (Opening Bell Daily)

-

Netflix will acquire Ben Affleck’s AI company for as much as $600 million (Bloomberg)

-

Costco customers sued Costco in a proposed nationwide class action seeking refunds for tariffs (Reuters)

🗓 March 12, 2020: Global markets suffered one of their most violent sell-offs ever as the COVID-19 pandemic spread rapidly across the world, with the S&P 500 shedding nearly 10%.

📩 Want to get in front of 200,000+ investors who get this newsletter and the 350,000 professionals who can access it on Bloomberg Terminals? Reply to this email and tell us why we should work together.