January 20, 2026, marked the completion of President Donald Trump’s first year (Year 1) of his second term. As investors consider the outlook for the stock market in President Trump’s second year (Year 2), it’s important to assess historical patterns of the four-year Presidential cycle, current conditions, and sentiment to set expectations for the year ahead.

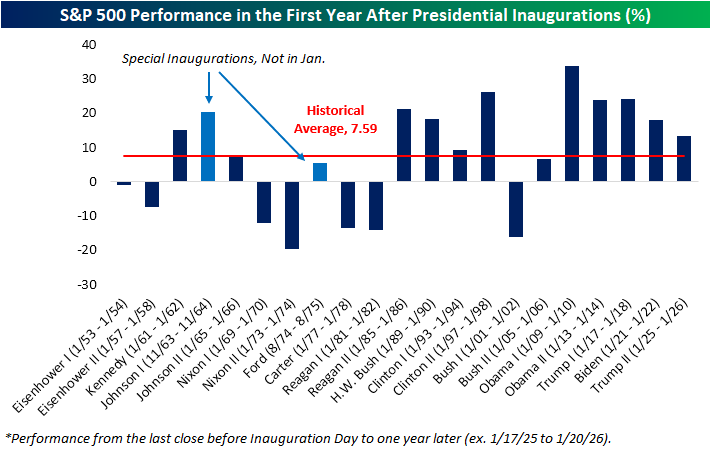

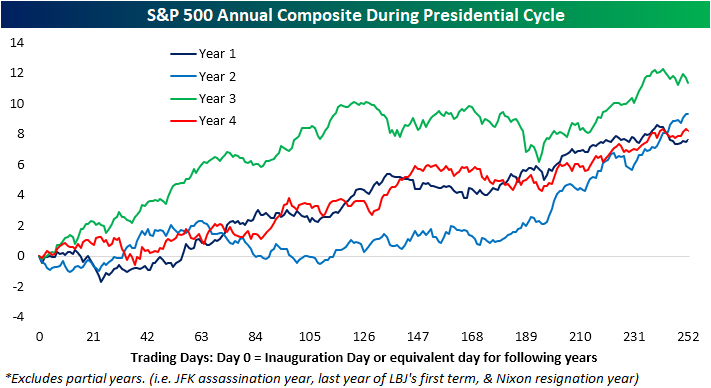

As far as the stock market is concerned, it was not a bad 12 months. The S&P 500 rose 13.3 percent. That beats the 7.59 percent average of the first year of the four-year presidential cycle, according to Bespoke. However, it significantly trailed the 24 percent return in Trump’s first term. Also, it was the worst return for a Year 1 in two decades (since Bush Jr.’s second term).

Positive gains in the first year of a president’s first term have become common, with only one down year in the last 44 years. That one down year was during the dot-com bubble implosion in 2001.

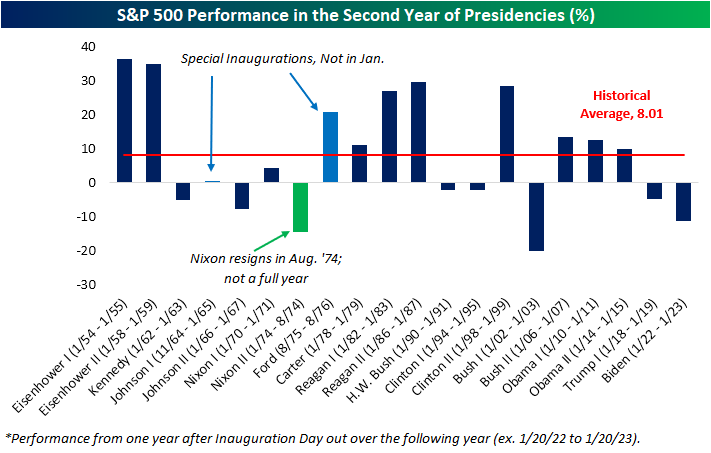

The stock market has also performed well in Year 2 of the four-year presidential cycle (which is how we would classify the stretch from January 20, 2026, to January 20, 2027). The average return of the S&P 500 during Year 2 was 8.01 percent. However, while there was just one negative Year 1 in the last 40 years, Year 2 has experienced four declines.

Four down years out of 10 occurrences does not feel hopeful to me. Those four down years were caused, in part, by:

- In 1990, there was a small recession;

- In 1994, the Federal Reserve raised interest rates to fight inflation;

- In 2018, the Fed tried to normalize interest rates, raising the federal funds rate by one percentage point over nine months; and

- In 2022, the Federal Reserve again raised interest rates to fight inflation.

I do not expect either a recession or higher interest rates in the next 12 months. Also, Scott Little’s LinkedIn post makes me feel more hopeful for a positive Year 2.

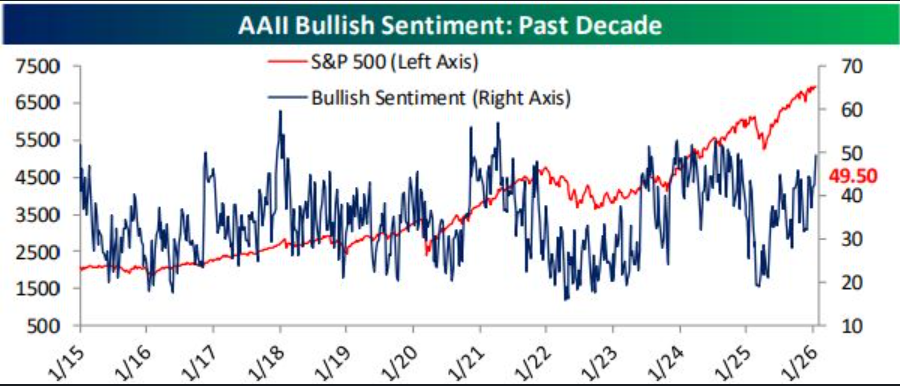

Scott looked at the American Association of Individual Investors (AAII) sentiment survey and saw that the number of “Bulls” dropped to 49.5 percent (later to 43.2 percent).

A reading of 43.2 percent is nothing to get excited about; the historical average is 37.5 percent. But boring can be good.

Fewer bulls are typically a good sign for stock market contrarians, like Berkshire Money Management. Stock prices often climb a wall of worry, meaning we buy stocks more aggressively when the crowd is freaked out (an industry term). Conversely, if everyone is happy, the market has probably priced in all the good news and is thus more vulnerable to shocks.

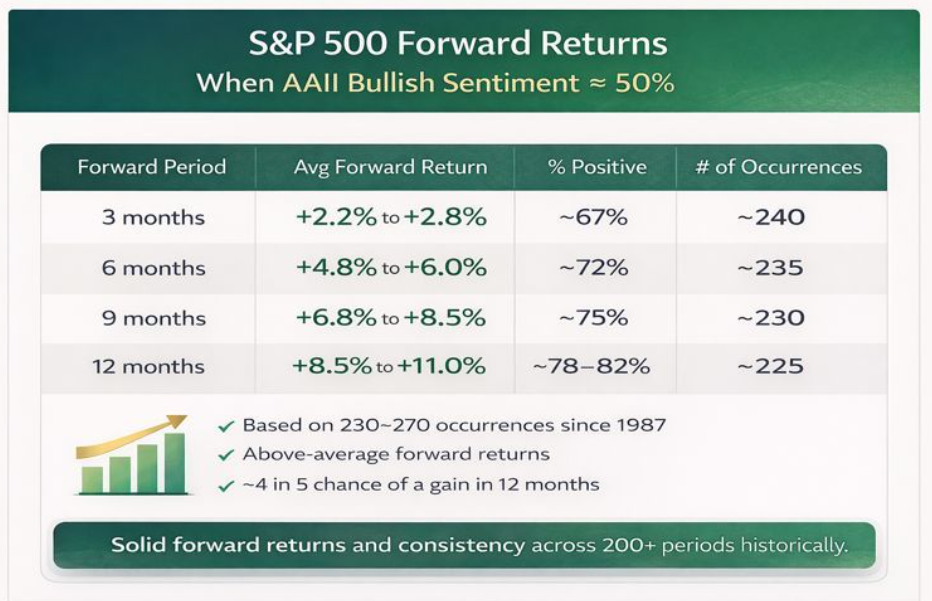

Boring means that investors are not euphoric and excesses do not have to be worked off. For Year 2 of a presidential year—so long as there is not a recession and the Fed does not raise rates—the historical AAII data suggests an 8.5 percent return for the S&P 500, with a four-in-five win rate.

Looking out further, if we can get through the next 12 months, Year 3 is the best year of the four-year presidential cycle, and Year 4 is similar to Year 1.

I do not predict an eight percent return for the stock market; my base case is a slight decline. Nonetheless, there is always a chance for Year 2 to end significantly lower—or much higher. On the surface, that sounds useless, but dig deeper and the Year 2 and AAII data reinforce what I have said before: The stock market will probably go sideways for the full duration of 2026, but it seems to have a much better chance of an upside surprise than a downside shock. I remain invested in stocks, even if it is more diversified than in previous years. In the stock market and economic outlook for 2026, I addressed the global markets as follows:

For most of the last decade plus, “stay home” (overweight the U.S.) was the right trade. It worked spectacularly.

But the world changes. And in 2025, non-U.S. markets reminded investors that global leadership rotates. Part of this is valuation. Part of it is currency. From a portfolio perspective, here is the simplest point: When the U.S. is already an outsized share of global benchmarks, you do not need to make heroic bets to have a lot of U.S. exposure because you already do. Next year, 2026, could be the year to take diversification more seriously, not as a defensive posture, but to participate if leadership broadens. And not only in foreign stocks but also in domestic sectors, asset classes, and capitalizations beyond the aforementioned Magnificent Seven storyline.

I reduced my overweight exposure to large-cap U.S. growth stocks and used the proceeds to buy the Innovator International Developed Power Buffer ETF (symbol: INOV) for portfolios intended to be on the more conservative side and Vanguard FTSE Developed Markets Index ETF (symbol: VEA) for more “moderate” and growth-oriented portfolios. Heading into 2026, I plan to stay diversified, watch for leadership shifts, and position to capture upside if market sentiment improves.

Allen Harris is an owner of Berkshire Money Management in Great Barrington and Dalton, managing more than $1 billion of investments. Unless specifically identified as original research or data gathering, some or all of the data cited is attributable to third-party sources. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Advisor’s clients may or may not hold the securities discussed in their portfolios. Advisor makes no representation that any of the securities discussed have been or will be profitable. Full disclosures here. Direct inquiries to Allen at AHarris@BerkshireMM.com.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)