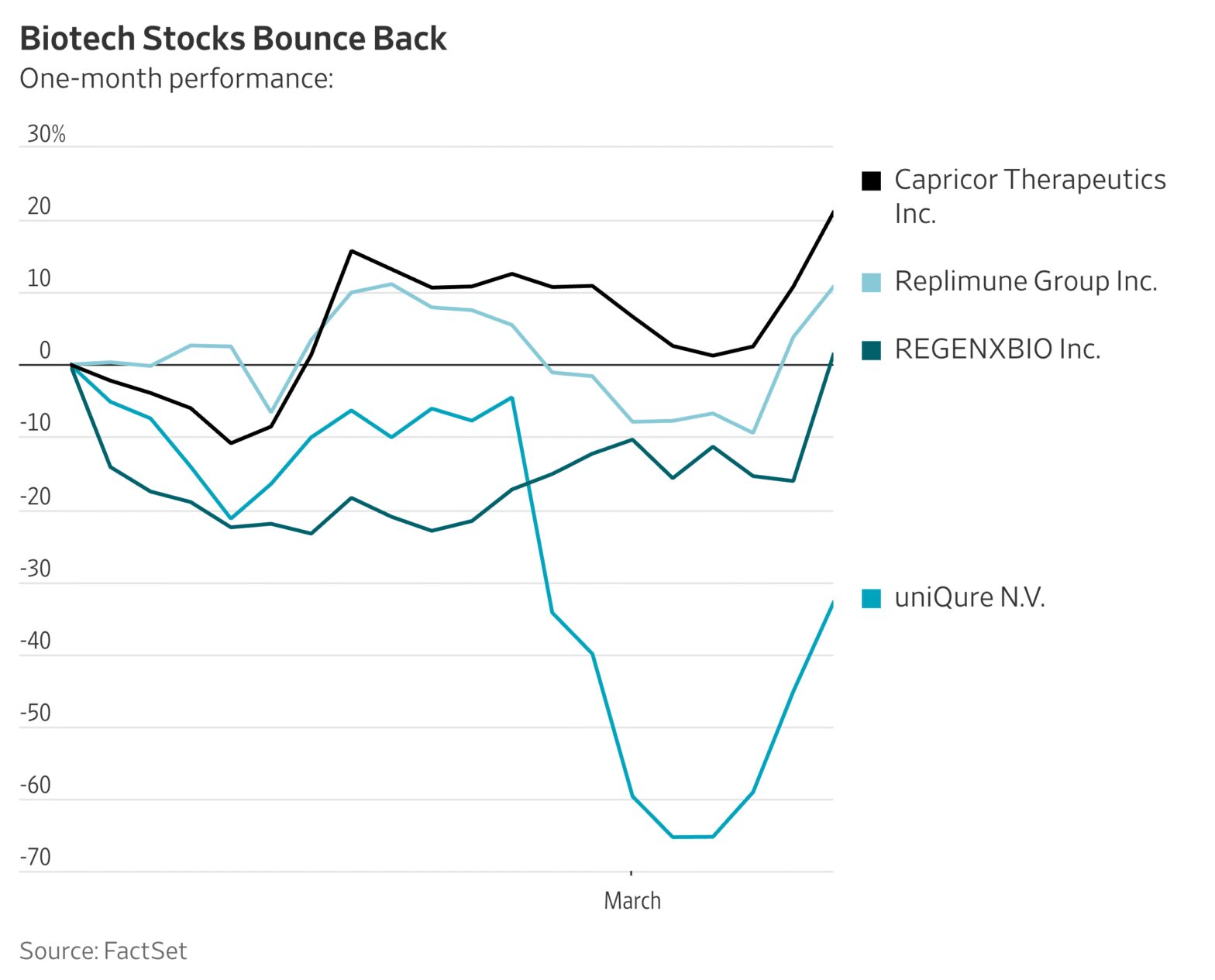

nortonrsx/iStockPhoto / Getty Images

When the world is as turbulent as it is right now, it can be tempting to bail on your stocks and pile into safe investments. But taking this approach can hurt your retirement plans.

Stock market investments are the growth engine of your retirement savings. If you have a lot of GICs and bonds, you are sacrificing this growth and ultimately, your retirement.

Despite the headlines, you need stock market exposure.

Asset allocation – how you divide your investments between cash, bonds, and stock – is the biggest driver of your returns and the most important investing decision you will make. But the tools and shortcuts that some people use to decide on their mix of stocks and bonds are imperfect, and lead to portfolios that are too conservative.

One popular rule of thumb is to subtract your age from 120, and make that your allocation to stocks. By this calculation, a 50 year-old should have 70 per cent of their retirement funds in stocks and the rest in bonds.

This is far too simplistic a method and ignores all kinds of important factors such as when you will need the money, how much you already have saved, and how you feel about risk. It’s also too safe for a lot of people.

You can also fill out a questionnaire like this one to help you decide, or play around with this spreadsheet. These are better approaches, but are also imperfect. Some of the questions require you to assess your tolerance for risk. The lower your self-proclaimed risk tolerance, the less you will have invested in stocks.

The trouble is that some people are too risk-averse, and this means they end up with an inappropriately-high allocation to bonds. In my experience, these folks can learn to have a higher risk tolerance, and that can be hugely beneficial for their retirement savings.

One reason people are afraid of the stock market and its ups and downs is because they just don’t understand it. It’s a black box. But when someone learns even a little bit about the stock market and how it moves over longer periods, they become more comfortable with the idea of investing.

The most powerful way to make you feel more comfortable is to look at a long-term stock market chart. The U.S. stock market performance– represented by the S&P 500 – is a jagged line, but the jagged line runs up and to the right.

I’m 67 and retiring, but my spouse will keep working. Should I wait until 70 to take CPP?

The takeaway is that the stock market has always risen over longer periods of time. Over any 10-year time period since 1942, the S&P 500 has had a positive return.

There are also far fewer negative years than positive years. The S&P/TSX Composite Index in Canada fell in 11 of the past 38 years – that’s about 30 per cent of the time, while the U.S. market had only nine negative years over that period.

It’s also comforting to know that it’s rare for the Canadian or U.S. market to have two years of losses in a row. Over the past 50 years, the U.S. and Canadian markets had two consecutive negative years only twice: In the 70s, and during the tech bubble in the early 2000s.

If stocks have a bad year, we can be pretty confident that the next year markets will rise. And while bear markets feel awful, they are much shorter-lived than bull markets.

This perspective on how the stock market has performed should give you confidence in holding on to your stocks. It’s about understanding how the stock market has behaved historically, and believing that it will continue to follow these patterns in the future.

Deciding how much to put in stocks should not be based on what the market is doing now and what’s going on in the world. That’s called market timing and it doesn’t work. Even if you feel like the market is likely to fall, you need to choose the right allocation and implement it.

Let’s be clear about one thing though: In order for this to work, you need to have a diversified portfolio of stocks. Owning a small number of individual stocks is too risky and will not have the same returns as the overall market. Best to hold an index-tracking exchange-traded fund, or at the very least, a mutual fund.

Don’t cheat yourself out of getting higher returns on your retirement money. Get comfortable with market volatility and jump in. Your future self will thank you.

Anita Bruinsma is a Toronto-based certified financial planner at Clarity Personal Finance.