Sundry Photography

Enphase Stock Hampered By Interest Rate Headwinds

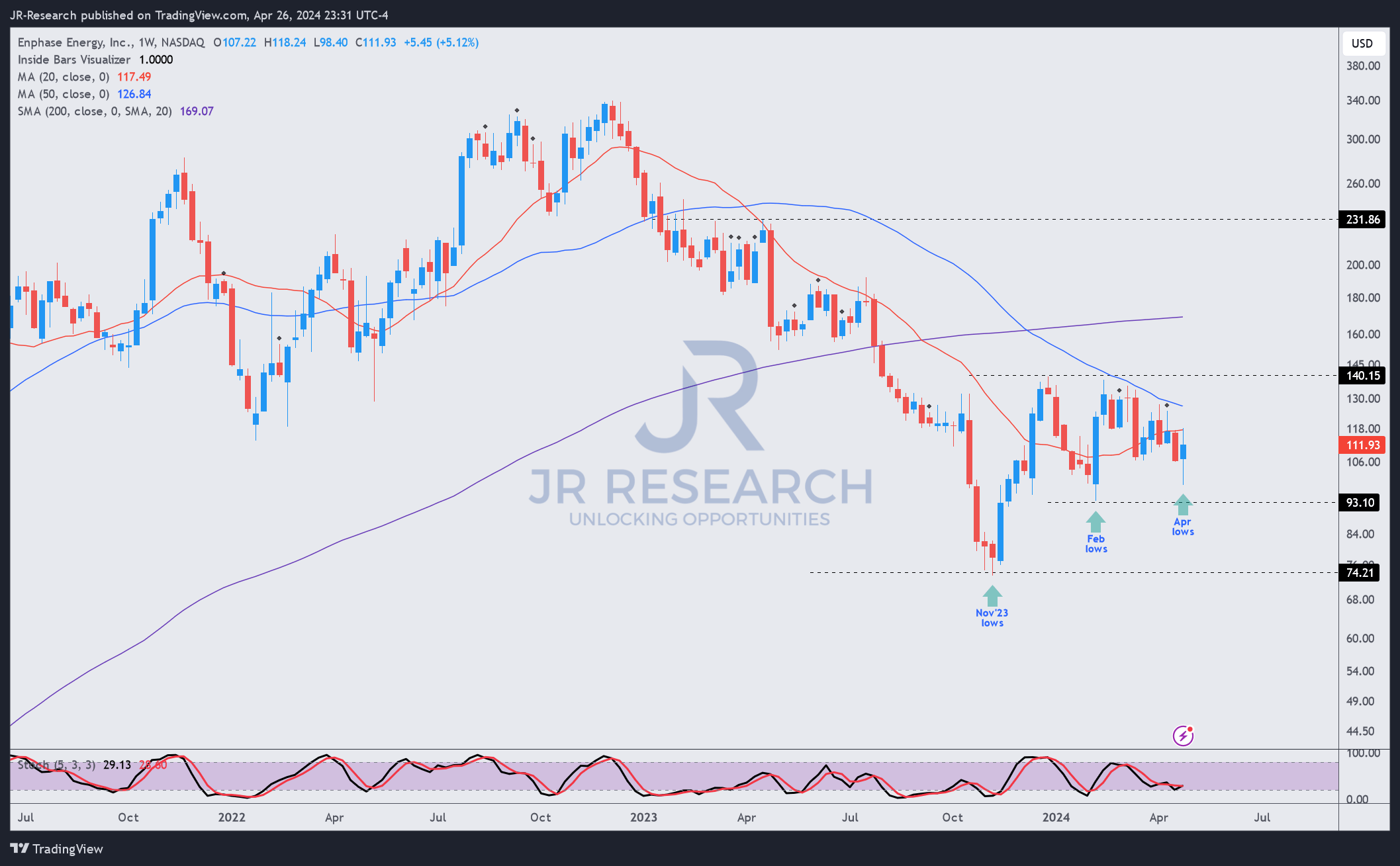

Enphase Energy (NASDAQ:ENPH) investors have continued to experience significant volatility even as ENPH bottomed out in November 2023. ENPH surged to its December 2023 highs as investors anticipated a dovish Fed ready for rate cuts in 2024. I urged investors to consider buying ENPH’s dips in mid-February 2024. However, more recent challenging inflationary dynamics and more hawkish commentary from Fed officials have tempered expectations of the initial six cuts anticipated at the start of 2024. Notably, the market has lowered their expectations significantly to one or even possibly no cuts this year. While Citi (C) analysts still expect 100 bps of rate cuts starting in July 2024, I caution investors to watch the 10Y (US10Y) price action carefully, as the 10Y has resumed its upward climb since bottoming out in early March 2024.

ENPH Quant Grades (Seeking Alpha)

As a result, I’m not surprised by the volatility observed in ENPH, as it remained in a consolidation zone between the $93 and $140 levels. Recent buying sentiments suggest investors are still relatively pessimistic (“D+” momentum grade) as they reassess Enphase’s customers’ inventory digestion and sell-through levels. I noted that the weaknesses in residential solar installations have not subsided, as installations “are projected to decline by 13% in the US this year.”

Enphase’s Q1 Earnings Suggest Bottom Is Close

Enphase’s Q1 earnings call suggests management still expects the intense challenges in the market to subside in Q2, with Q1’s performance expected to be the bottom. However, that also suggests we would likely get more clarity only in the second half, suggesting ENPH’s buying sentiments are expected to remain tepid in the near term.

Accordingly, Enphase reported revenue of $263.3M in Q1, down 64% YoY. Enphase’s adjusted EPS dropped markedly to $0.35, down 75% YoY. Therefore, I gleaned that the market’s pessimism over Enphase’s business model is justified, as it has demonstrated to be more cyclical than previously anticipated. Investors must assess whether Enphase’s long-term thesis of benefiting from the secular growth drivers of solar energy adoption has hit a significant (but transitory) road bump or could face a structural decline.

China’s solar growth slowdown experience suggests that the massive market has also observed a normalization phase, although it is still expanding. However, market dynamics in Enphase’s key markets (the US and Europe) indicate that the double whammy of seasonality and high-interest rate factors hampered growth. Consequently, it impacted demand dynamics significantly even as inventory swelled.

However, Enphase’s guidance indicates that the company intends to under-ship end market demand in Q2 by about $90M in response to the still weak dynamics. I believe the caution is justified as SunPower (SPWR) management highlighted that the slower-than-expected recovery disappointed SunPower, behooving its recent workforce reduction. Moreover, the industry challenges are pervasive, as “approximately two-thirds of household solar installers in California are facing difficulties generating sufficient sales.”

With that in mind, I assessed that Enphase’s Q2 revenue guidance range of between $290M and $330M is prudent, as it also lowered its expected shipment of IQ batteries to between 100 megawatt hours and 120 megawatt hours. Revised Wall Street revenue estimates of $317M are more optimistic than Enphase’s guidance. As a result, it suggests Enphase could be conservative with its outlook, as Enphase management also concurred, providing potential “opportunities for upside in the battery business.”

Furthermore, ENPH’s “B-” growth and “B+” profitability grades augur well for Enphase to regain market share as intense headwinds in the residential solar market possibly peak in the first half. It should provide Enphase the capabilities and investors the clarity that ENPH remains well-positioned to invest through the cycle. Enphase also highlighted that it’s confident in launching its next-gen IQ9 microinverters in the first half of 2025. Accordingly, it should broaden Enphase’s market opportunities, allowing it to capitalize on the “residential and three-phase small commercial markets.”

While Enphase has a $1B share purchase program from its July 2023 authorization, management only repurchased $42M worth of shares in the first quarter. Coupled with a lack of any dividends, it’s clear that ENPH endears itself to growth and renewable energy investors. Considering ENPH’s current market cap of $14.67B, the lack of a more aggressive repurchase cadence will not likely convince growth investors that management believes its shares are significantly undervalued.

However, I assessed the need for Enphase to manage its free cash flow prudently, which is justified, as Enphase delivered an FCF of $42M in Q1. As a result, I believe the anticipated improvement in underlying inventory and demand dynamics is expected to be more significant in influencing buying sentiments than Enphase’s repurchase program at the current levels.

Is ENPH Stock A Buy, Sell, Or Hold?

ENPH price chart (weekly, medium-term) (TradingView)

While near-term buying sentiments on ENPH stock are expected to remain tepid, dip-buyers have returned to support ENPH’s bottom above the $93 zone. This suggests that ENPH’s November 2023 lows ($75 level) are expected to be its long-term bottom. Therefore, the market seems to be in sync with Enphase management’s expectations of a more robust second-half recovery as market conditions potentially improve.

Moreover, with the market already considering and pricing in a more hawkish Fed, it should lower the yields-related headwinds against ENPH moving forward. In other words, I believe growth investors will increasingly turn their focus on Enphase’s execution, which we should receive more clarity on in Q3.

However, since the market is always forward-looking, high-conviction investors anticipating ENPH’s long-term lows to hold should capitalize on the market’s pessimism to add exposure.

Rating: Maintain Strong Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA’s bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!