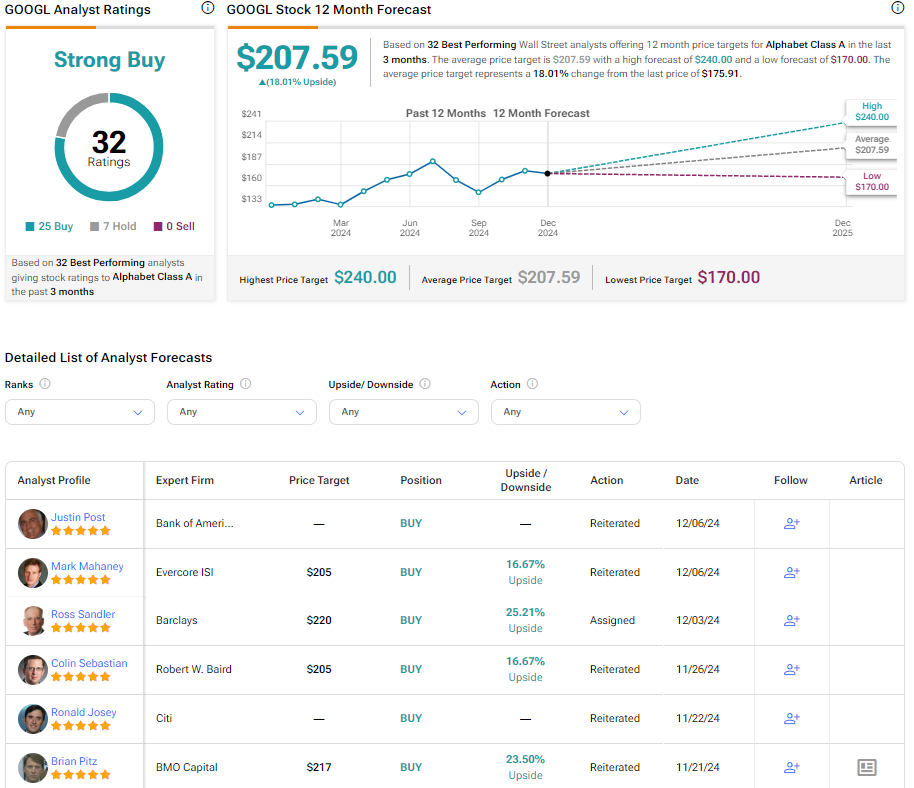

For the most part, the Magnificent Seven are must-owns, in my view. That’s because these businesses offer everything that I like to see as an investor. The growth prospects of these companies are exceptional with strong balance sheets. Alphabet, or Google (GOOGL), is no exception to this rule. After reviewing Google’s third-quarter earnings report, I am initiating coverage with a Buy rating with a $220 price target.

-

Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

-

Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

That’s because the company has tangible growth catalysts and boasts a sizable net cash position. Furthermore, as I’ll discuss in a bit, the factor that puts my bullish sentiment over the top is the arguably cheap valuation.

On October 28th, Google shared its third-quarter earnings that back up my Buy rating. The company’s revenue climbed 15.1% higher year-over-year to $88.3 billion. For more color, this came in ahead of the $86.4 billion analyst consensus. Strength throughout its Google Services and Google Cloud businesses made this topline growth possible.

In addition, Google’s diluted EPS jumped 36.8% over the year-ago period to $2.12. That was $0.28 better than the analyst consensus of $1.84. The firm’s tight cost management kept the growth of operating expenses under control, which is how diluted EPS growth easily outpaced revenue growth.

Google looks to have plenty of catalysts to fuel further growth in the years ahead, which further supports my Buy rating. One catalyst that bodes well for the company is its rollout of AI Overview to more than 100 new countries and territories at the end of October. Per CEO Sundar Pichai‘s opening remarks during the Q3 2024 earnings call, this feature will now reach over one billion users monthly. Pichai also noted that engagement thus far has been strong, which is contributing to increased overall search usage and user satisfaction.

Another reason for optimism is that rapid growth at Google Cloud looks poised to continue (revenue grew 35% in Q3 2024). According to Pichai, this is because technology leadership and the AI portfolio are drawing in new customers, winning larger deals, and spurring 30% deeper product adoption with existing customers. Additionally, YouTube Shorts is garnering tens of billions of views each day.

As Google continues to monetize this business by growing viewership and working with advertisers, that should be another boost for the company. Thus, the analyst consensus is that diluted EPS will rise by 11.6% in 2025 to $8.95, followed by another 14.9% boost in diluted EPS to $10.28 in 2026.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)