As global conflicts escalate, the chances of a stock market crash increase. We already experienced some volatility Monday (2 March 2025) and I expect to see more in the coming days.

But rather than panic and smash the sell button, follow these three tips to navigate the turmoil…

When the world feels risky, money often moves into so‑called ‘defensive’ shares. Think utilities, healthcare, and everyday consumer staples. They don’t magically avoid crashes, but their profits usually remain steadier because people rely on them in good times and bad.

For a UK investor, shifting your portfolio into these areas is like swapping a sports car for a sturdy family SUV. It might still get dented in a storm but, overall, it’ll hold up better.

Stockpiling a decent amount of spare cash means you can capitalise on low prices before the market rebounds.

With around 20% of your portfolio in cash, you won’t need to sell shares in an emergency. When markets get wobbly, I tend to reduce my holdings of ‘risky’ stocks and keep the cash aside.

Stock picking during a sell‑off can be daunting because it’s hard to know which companies will recover. But if you’ve done your homework in advance, you can use these moments to snap up top-quality shares at rock bottom prices.

For example, one of my favourite UK companies is Diploma (LSE: DPLM), but the shares typically trade at sky high prices.

Here’s exactly why I think it’s a compelling stock to consider if the stock market crashes.

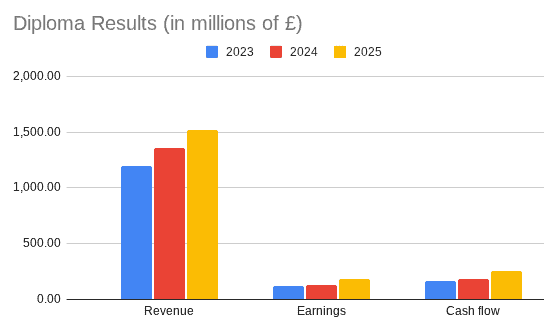

Diploma’s a UK‑listed specialist distributor that supplies vital components and services in areas including controls, seals, and life sciences. Sounds boring, but there’s a consistently high demand for its niche parts and products.

It has a long record of steady growth, strong margins and smart bolt‑on acquisitions. Revenue and earnings have been compounding at roughly mid‑teens percentages for many years.

In 2025, earnings grew around 43% to roughly 138p, and kept return on invested capital (ROIC) near 20% — impressive numbers for a mature business.

It also pays a dividend that’s been rising at around low‑to-mid‑teens each year, with a payout ratio just under 50%. That leaves sufficient room to keep investing for growth while still rewarding shareholders.

The catch is valuation. Right now the shares trade on a price-to-earnings (P/E) ratio of about 41, versus sector peers closer to the mid‑teens. Its price‑to‑sales (P/S) ratio is also very high and price‑to‑book (P/B) is close to 8.