Microsoft’s growth doesn’t depend on a single product, service, or industry trend.

It was a little over six years ago that Apple became the world’s first trillion-dollar company. Now, there are several others with market caps over $1 trillion and a handful of companies valued at over $3 trillion.

The stock market can do just about anything in the short term, so it’s impossible to know how a company will do in 2025. But Microsoft (MSFT 0.99%) has what it takes to chart a path toward steady growth, which can’t be said for all of the companies valued at over $1 trillion

Here’s why Microsoft stands out as the best all-around buy of the ultra-megacap growth stocks.

Image source: Getty Images.

Staying nimble

What impresses me the most about Microsoft is its ability to strengthen the quality of its earnings while continuing to take risks and innovate. In recent years, it has undergone transformational growth while maintaining many of its software solutions that are multiple decades old.

The company has integrated artificial intelligence (AI) into its highly profitable Intelligent Cloud segment. It continues to expand its AI assistant tool, Copilot, across the Microsoft 365 software suite and other aspects of its business.

For example, GitHub Copilot has become the most widely adopted AI-powered developer tool. According to the company’s fourth-quarter fiscal 2024 earnings call, GitHub’s annual revenue run rate is now $2 billion.

On Oct. 21, Microsoft announced new autonomous agents that can be assigned specific tasks through Copilot Studio. Businesses can create agents for simple administrative tasks like processing sales orders. Agents can assist with sales lead generation, data management, customer service, and more. This new product announcement is just one of many examples of how Microsoft maintains its entrenched foothold across several end markets.

Too often, we see companies reach a certain size and get bogged down by inefficiencies. Their size works against them, and they lose that innovative spirit that made them successful in the first place.

Microsoft uses its size to its advantage while avoiding making it a weakness. It has been ramping up spending to accelerate growth, but not to the point of being wasteful. The company is still buying back a ton of stock and making sizable raises to its dividend every year.

The company has several levers to pull to create value for shareholders. It doesn’t rely entirely on new ideas or lean too heavily on its legacy products and services. It isn’t an all-or-nothing growth stock that doesn’t pay a dividend and dilutes shareholders.

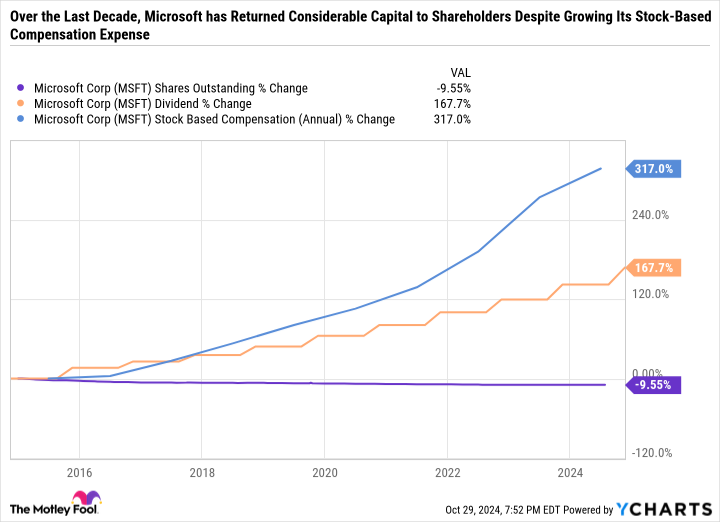

In fact, Microsoft buys back more than enough stock to offset stock-based compensation. As you can see in the following chart, it has made consistent and sizable raises to its dividend and reduced its share count by 9.6% over the past decade despite rapidly expanding its stock-based compensation, which surpassed $10 billion for the first time in fiscal 2024.

MSFT shares outstanding; data by YCharts.

Perhaps most important of all, Microsoft has more cash, cash equivalents, and marketable securities than debt on its balance sheet. It finished fiscal 2024 (ended June 30) with $18.32 billion in cash and cash equivalents, $57.23 billion in short-term investments like marketable securities, and just $42.69 billion in long-term debt.

A high-margin cash cow

Too often, investors focus on the quantity of company’s revenue and earnings without determining if those results are sustainable. There are countless examples of companies that developed a hit product that contributed to unbelievable results. But the product proves to be a fad, demand falls, results plummet, and the company can’t score another big idea.

Or the product gets surpassed by a better alternative: Think Apple replacing BlackBerry, Netflix surpassing Blockbuster, or simply the shift to online sales that led to companies like RadioShack going bankrupt.

Microsoft has arguably the best moat of any company valued over $1 trillion because it does so many different things so well — Microsoft Cloud, Windows, office commercial and consumer products, LinkedIn, Xbox content and services fueled by Microsoft-owned Activation Blizzard, server products, devices, enterprise services, and more.

Here’s a look at Microsoft’s fiscal 2024 results by segment.

|

Segment Revenue |

2024 Results |

|---|---|

|

Productivity and business processes |

$77.73 billion |

|

Intelligent cloud |

$105.36 billion |

|

Other personal computing |

$62.03 billion |

|

Total revenue |

$245.12 billion |

|

SEGMENT OPERATING INCOME |

|

|

Productivity and business processes |

$40.54 billion |

|

Intelligent Cloud |

$49.58 billion |

|

Other personal computing |

$19.31 billion |

|

Total operating income |

$109.43 billion |

|

OPERATING MARGIN |

44.6% |

Data source: Microsoft.

A decade ago, Microsoft earned $86.83 billion in revenue and $27.9 billion in operating income. So while its revenue is only up 161.9% over the last 10 years, its operating income is up nearly fourfold. The Intelligent Cloud business alone is generating more revenue and nearly double the operating income than the company as a whole was booking a decade ago.

Built to last

Microsoft faces competition across all of its segments, but the company does an excellent job developing new tools that can be used across the business. Copilot, and AI in general, are great examples of how it deployed a similar solution across its segments and improved them all.

In sum, it would take a lot to damage the structural integrity of Microsoft’s earnings profile. So although you could say the stock looks expensive at 37.1 times earnings, the quality of those earnings and the ability to grow earnings through multiple segments and stock buybacks makes it a much better value than it appears at first glance.

For these reasons, Microsoft stands out as the company with the best balance of risk and potential reward that is valued at over $1 trillion.

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Microsoft, and Netflix. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)