Dividend Kings are an elite group of companies that have distributed and raised their payouts for at least 50 consecutive years. As valuable as this track record is, Dividend Kings tend to take a back seat to faster-growing names during a market that keeps going higher.

After all, optimistic investors would much rather find a company with growth prospects and that can pour all its excess earnings and cash flow into that growth rather than pass it along to shareholders in the form of a dividend. But long-term investors know that the true value of Dividend Kings is when equity prices are falling all around you, and yet, the Dividend King is there no matter what to provide reliable passive income.

Here’s why one of the best-known Dividend Kings, Coca-Cola (NYSE: KO), along with two other well-known names, Emerson Electric (NYSE: EMR) and Procter & Gamble (NYSE: PG), are all worth buying now.

Coca-Cola just reminded investors of this timeless lesson

Daniel Foelber (Coca-Cola): At first glance, Coca-Cola’s recent quarter and dividend raise weren’t too special. Case volume — a key metric that shows demand for Coke’s products — grew just 2% in the year, but revenue and earnings growth were solid. 2024 guidance calls for non-GAAP (generally accepted accounting principles) organic revenue growth of 6% to 7% and comparable non-GAAP earnings-per-share growth of 4% to 5%.

What’s more, Coke raised its dividend by 5.4% to an annual $1.94 per share, marking the 62nd consecutive annual increase.

All told, Coke delivered a great 2023, good but not great 2024 guidance, and the largest percentage increase to the dividend since 2017. So why is Coke up over 3% since reporting earnings a couple of weeks ago? The answer has more to do with what investors expect from Coke than from its recent results.

Coke is an industry-leading business with an above-average dividend yield and a below-market valuation. Once factoring in the recent raise, its dividend yield is a hearty 3.2% — more than double the 1.4% dividend yield of the S&P 500. Coke’s price-to-earnings (P/E) ratio of 24.8 is also less than the S&P 500’s P/E multiple of 27.

Opponents of Coke stock will say it deserves to trade at a discount to the market because of its low growth. But I’d argue that you can count on one hand how many dividend stocks are in the same league as Coke when it comes to paying and raising a reliable dividend.

Coke isn’t the kind of company that needs to deliver outstanding growth. All it has to do is grow earnings per share in the mid-single-digit range per year, and it can fund a sizable buyback program and grow its payout. Coke’s 2023 performance and latest dividend raise validate why Coke remains a top-tier dividend stock to buy and hold for decades to come.

Emerson Electric’s pivot toward growth continues

Lee Samaha (Emerson Electric): The industrial company has increased its dividend for the last 65 years. That’s excellent news for income-seeking investors, as well as growth investors. It’s not often discussed that being able to grow your dividend implies having the ability to grow the earnings and cash flow to fund the increase.

The company’s current dividend yield of 2% is well and fine, but it’s not the key reason investors are holding the stock. Instead, management’s plan to pivot the company toward automation and adjacent markets has caught the eye. Its stated aim is to “become a pure-play global automation company serving diversified end markets,” and management took a big step in that direction by selling its majority share in its climate technologies business in 2023.

That deal followed Emerson’s deal in 2022 to combine its industrial software business with AspenTech to create a new Aspen Technology, of which Emerson owns 55%. The dealmaking continued in 2023 with the successful acquisition of software-connected automated test and measurement systems company NI in October. The timing of the acquisition may prove opportune as the semiconductor and consumer electronics industries are expected to pass a trough in 2024.

Thinking longer-term, Emerson’s focus on automation makes it ideally placed to benefit from powerful reshoring trends in the U.S. economy and the drive toward using automation to enhance productivity in general. There may be better value automation-focused stocks out there. Still, they tend to be foreign, and investors who don’t want to worry about exchange rate movements will prefer Emerson Electric for its combination of dividends and growth.

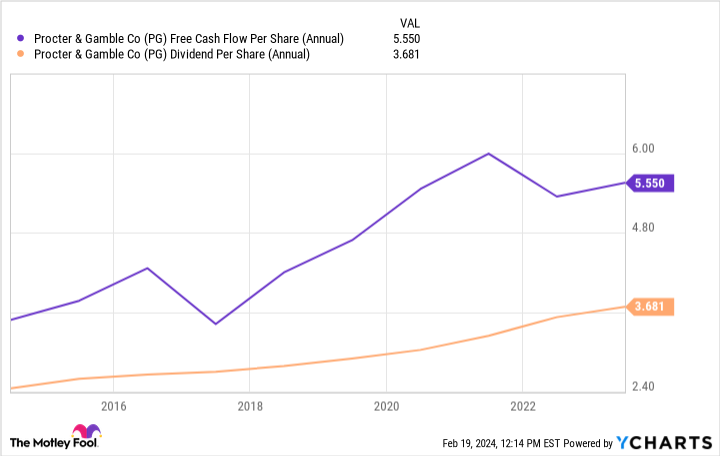

P&G produces prodigious cash from a diverse portfolio of brands

Scott Levine (Procter & Gamble): For those keen on drinking up the dividends Coca-Cola offers, Procter & Gamble will also be appealing. Like Coca-Cola, P&G is a consumer staples company with an impressive history of rewarding shareholders, hiking its dividend higher for the past 67 consecutive years.

How has it accomplished this striking feat? The company maintains a portfolio of leading consumer products, which helps it generate massive amounts of cash it then returns to investors. For those looking to further fortify their portfolios with a consumer staples stalwart, P&G — and its 2.4% forward-yielding dividend — is an ideal consideration.

From baby care to home care to grooming, P&G owns some of the most popular consumer staples brands found in our homes today — and many located around the globe. And the company does an excellent job of translating sales of these items into strong cash flow. In 2023, for example, P&G converted 16.8% of its revenue into free cash flow. While this allows the company to pursue growth through acquisitions, it also helps fund its dividend payments without jeopardizing its financial well-being.

And that’s not the only perspective from which the company’s dividend looks secure. Over the past 10 years, P&G has averaged a payout ratio of 80.6%, which seems even more conservative if you discount the uncharacteristically high payout ratio of 186% it had in 2019.

The remarkable strength of P&G’s portfolio is unlikely to wane anytime soon. In fact, it may grow even stronger if the company pursues further acquisitions or grows organically through its own innovations — two strategies the company has excelled at over its 187-year history.

Moreover, it’s quite probable the company will continue to increasingly reward shareholders, making the stock a great choice for those looking to supplement their passive income.

Should you invest $1,000 in Coca-Cola right now?

Before you buy stock in Coca-Cola, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Coca-Cola wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 20, 2024

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Emerson Electric. The Motley Fool has a disclosure policy.

If You Own Coca-Cola, Then You Will Love These 2 Dividend Kings was originally published by The Motley Fool