![]()

Summary

- Stocks close at lows for the day, but equally weighted S&P 500 reaches new all-time high, as breadth continues to improve.

- What the bubble bears see is disguised in technology stocks, but superior fundamental growth supports valuations for now.

- Market resembles fair value at the index level, but offers opportunities for stock pickers and sectors.

- This idea was discussed in more depth with members of my private investing community, The Portfolio Architect. Learn More »

DNY59

Stocks took a breather on a sleepy Monday with little in the way of economic data. The major market averages closed at their lows for the day, but the equally weighted version of the S&P 500 powered higher by a small amount to close at another new all-time high. That has been my expectation, as breadth improves, and the average stock starts to outperform the heavyweight technology names that have fueled most of the gains this year. The Russell 2000 small-cap index also outperformed the major averages again.

Finviz

There is no doubt that the stock market has been on a torrent run over the past four months, rising 16 of the past 18 weeks, which is leading some to conclude that we have a bubble in equities. The rebound in Bitcoin towards its all-time high, which could be the most speculative investment of them all, is a persuasive factor. Yet, the bubble, if any, looks to be disguised in technology stocks. I say disguised because the surge has been backed up with phenomenal fundamental growth. That is why it looks more like this segment of the market has reached more than fair value, and that the rest of the market is in the process of catching up, but therein lies the opportunity.

Bloomberg

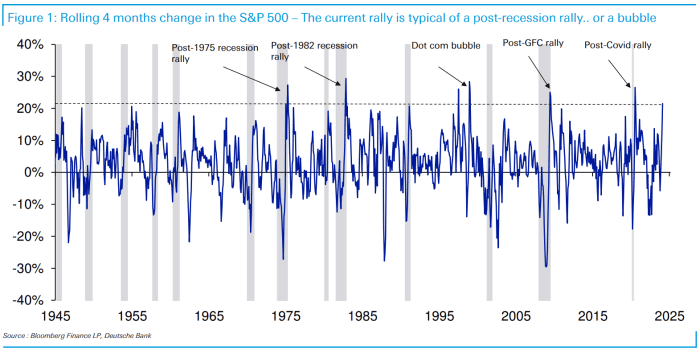

The bears are building their case on historical precedent. There have only been two occasions since World War II when stocks performed as well over a four-month stretch as they have over the past four months. The first was immediately following recessions like the one after the Great Financial Crisis or the pandemic in 2020 when the markets were completely washed out. Those returns were a function of washed out prices and tremendous amounts of stimulus.

Bloomberg

The second was during the late 1990s as the tech bubble was growing. Obviously, today is more reminiscent of the late 1990s, which is what has bears pounding their chests. There are parallels between today’s technology sector and the one we saw explode during the dot-com era, but the current advance is supported by an equally tremendous growth in profitability, which was not the case in the 1990s.

Bloomberg

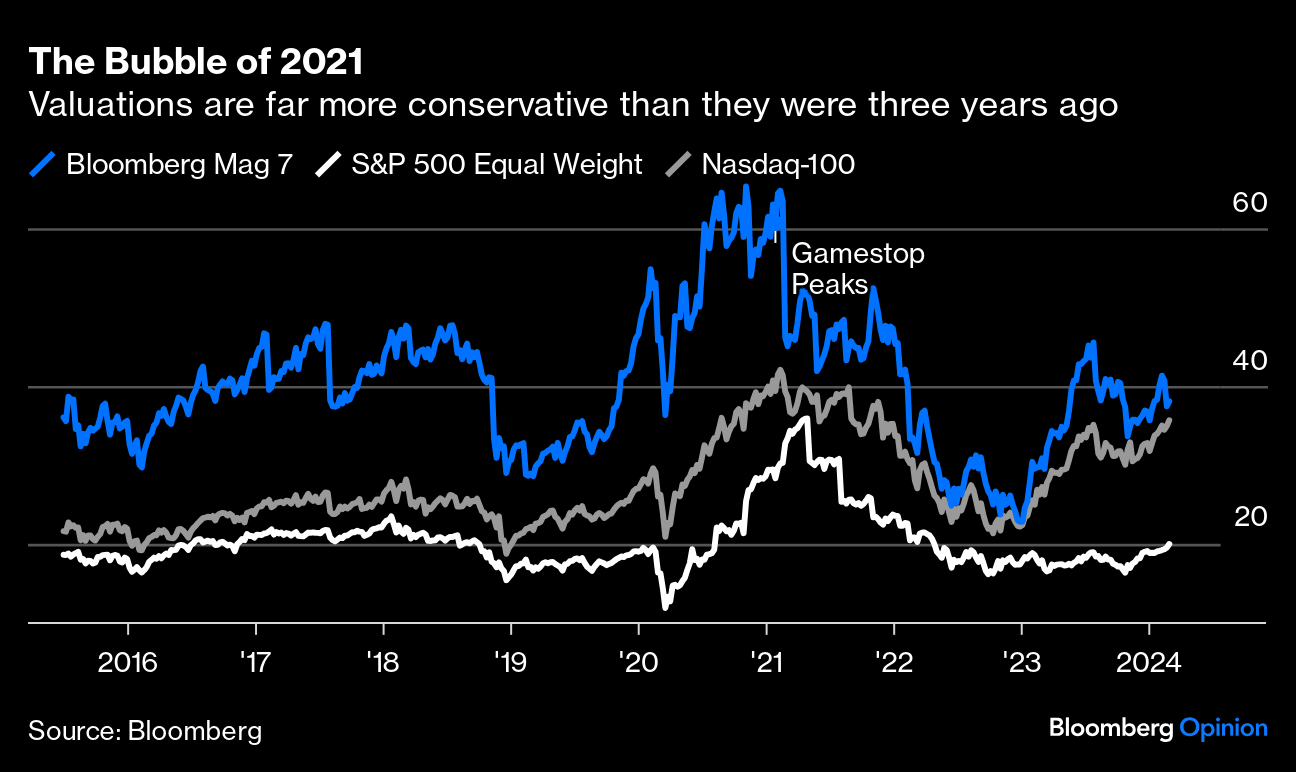

Today feels more like a market approaching fair value at the major market index level, but one that still offers lots of opportunities at the individual stock and sector levels. It is a stock pickers market. We do not see a surge in initial public offerings that would be reminiscent of the late 1990s. We also do not see mega mergers between companies that is typical in a bubble-like period. We also don’t have valuations for the average stock (S&P 500 equal weight) anywhere near what they were just three years ago on a trailing 12-month basis.

Bloomberg

Finally, there is still a tremendous amount of liquidity sitting in money market funds, satisfied with earning better than 5%. In fact, this mountain has grown since the beginning of this year. I continue to assert that when the Fed begins to cut short-term rates, this mountain will shrink, as investors move back into risk assets. There is no bubble in the stock market.

MarketWatch

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

This article was written by

Lawrence Fuller has been managing portfolios for individual investors for 30 years, starting his career at Merrill Lynch in 1993 and working in the same capacity with several other Wall Street firms before realizing his long-term goal of complete independence when he founded Fuller Asset Management. He also manages the Focused Growth portfolio on the new fintech platform called Dub, which is the first copy-trading platform approved by securities regulators in the US, allowing retail investors to copy the portfolio and ongoing trades of the manager they choose automatically.

He is the leader of the investing group The Portfolio Architect, which focuses on an overall economic and market outlook that complements an all-weather investment strategy designed to produce consistent risk-adjusted market returns. Features include: Portfolio construction guidance, access to an “All-Weather” model portfolio and a dividend and options income portfolio, a daily brief summarizing current events, a week ahead newsletter, technical and fundamental reports, trade alerts, and 24/7 chat. Learn More.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Lawrence Fuller is the Principal of Fuller Asset Management (FAM), a state registered investment adviser. Information presented is for educational purposes only intended for a broad audience. The information does not intend to make an offer or solicitation for the sale of purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. FAM has reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. FAM has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances or market events, nature and timing of investments and relevant constraints of the investment. FAM has presented information in a fair and balanced manner. FAM is not giving tax, legal, or accounting advice. Mr. Fuller may discuss and display charts, graphs, formulas, and stock picks which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. Consultation with a licensed financial professional is strongly suggested. The opinions expressed herein are those of the firm and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in market or economic conditions and may not necessarily come to pass.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)

Disagree with this article?

Submit your own.

To report a factual error in this article, .

Your feedback matters to us!