Pure Storage (PSTG) has shown some impressive performance over the past three months, with its stock rising more than 62%. Investors may be wondering what is driving the momentum and if it is sustainable.

See our latest analysis for Pure Storage.

Pure Storage’s momentum is no flash in the pan. After a rapid 62.6% share price return over the last three months, the company’s one-year total shareholder return now stands at an impressive 75%. These figures reflect investors’ growing confidence in Pure Storage’s growth prospects and its ability to deliver strong long-term results amid fast-changing tech trends.

If Pure Storage’s breakout has you rethinking your strategy, now is a great moment to broaden your search and discover fast growing stocks with high insider ownership

With shares on a remarkable run and strong growth figures on the board, the key question now is whether Pure Storage is still undervalued, or if the market is already factoring in all of its future upside potential.

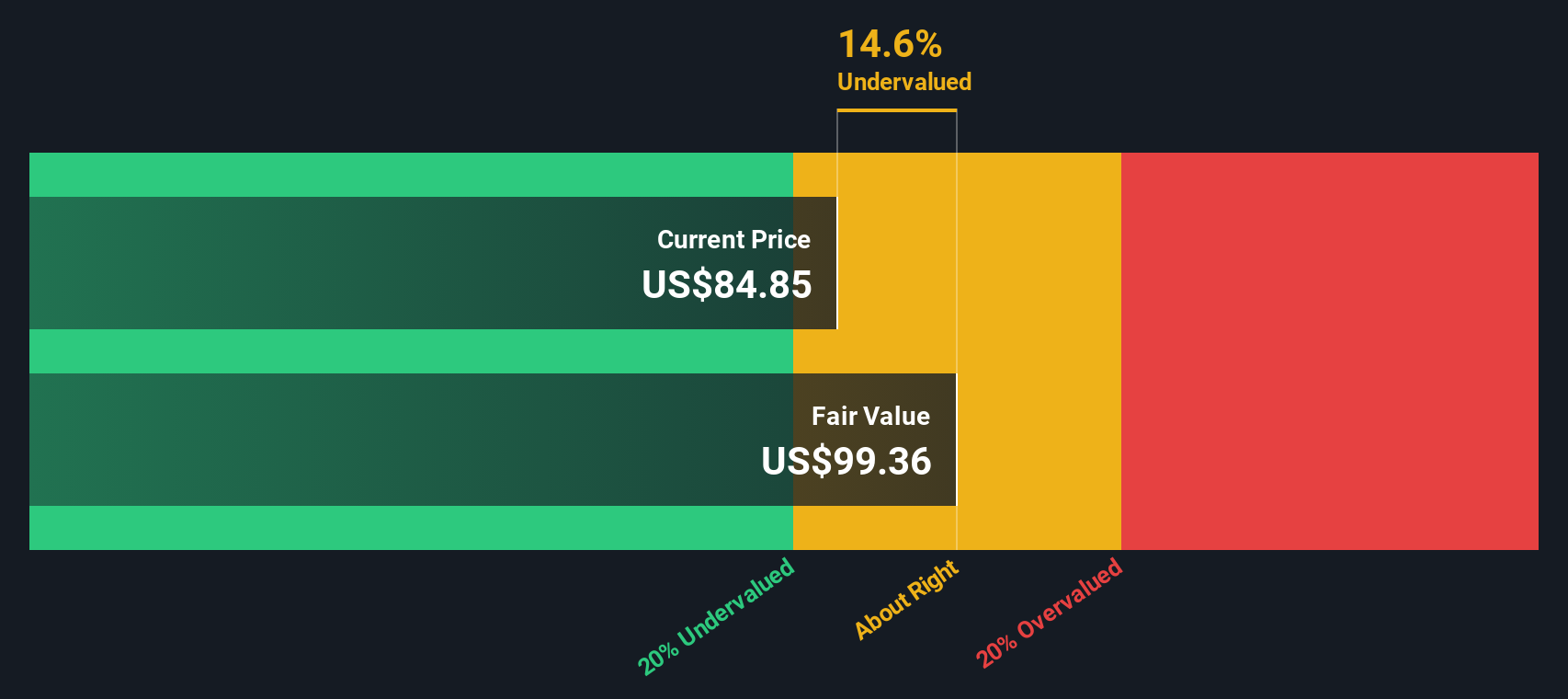

Most Popular Narrative: 10.2% Overvalued

With Pure Storage closing at $93.63, the most followed narrative puts its fair value at $84.94. This places the current price moderately above what analysts believe reflects its underlying fundamentals. Valuation debates here revolve around just how much growth and margin expansion Pure Storage can realistically deliver compared to what is already reflected in the price.

The adoption of Pure’s Enterprise Data Cloud architecture and software-defined solutions is accelerating among large enterprises, driven by the need to manage rapidly growing and increasingly valuable data assets in the evolving AI economy. This positions Pure to capture rising long-term revenue from digital transformation and AI/ML-driven workloads.

What is the hidden engine behind this ambitious valuation? The narrative leans on bold calls for future recurring revenue growth and a profit leap only seen at tech’s top performers. Want the full story and the disruptive forecasts driving this price? There is more beneath the surface.

Result: Fair Value of $84.94 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still risks, such as unpredictable revenue from early-stage hyperscaler partnerships and ongoing margin pressure from required infrastructure investments. These factors could challenge this growth story.

Find out about the key risks to this Pure Storage narrative.

Another View: SWS DCF Model Suggests Undervaluation

While analysts lean toward Pure Storage being moderately overvalued, the SWS DCF model offers a different perspective. According to our cash flow analysis, Pure Storage’s fair value is estimated at $103.09, nearly 10% above the current price. Could this disparity reveal hidden upside for the patient investor?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Pure Storage for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own Pure Storage Narrative

If you see things differently or want to test your own ideas, you can dig into the data and build a custom view in just a few minutes. Do it your way

A great starting point for your Pure Storage research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Expand your horizons and get ahead. Don’t limit yourself to just one company when countless breakthrough opportunities are within reach on Simply Wall Street.

- Supercharge your portfolio with growth potential and stay ahead of the curve by checking out these 26 AI penny stocks reshaping the global economy.

- Capture steady returns by targeting income opportunities through these 17 dividend stocks with yields > 3%, offering yields over 3% for consistent earning power.

- Tap into next-level tech innovation and early-mover advantages when you browse these 27 quantum computing stocks, featuring companies advancing quantum computing breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)