📌 Top story — scroll down for more updates

Oracle Lays Off 30,000 and Nike Falls Flat Once Again

5:00 pm

OpenAI just raised $122 billion—and the market barely reacted. That silence may say more than the headline. Then: Nike (NKE 15.51%) stumbles again, and Oracle (ORCL 1.22%) makes a massive workforce cut.

Travis Hoium, Lou Whiteman, and Rachel Warren discuss:

- Why OpenAI’s raise didn’t move markets

- Nike’s latest stumble—and what’s next

- Oracle’s 30,000-person layoff

🎧 The Motley Fool Money podcast drops daily after the bell! Listen on Apple Podcasts, Spotify, or other podcast platforms—or check out the Fool’s podcast feed.

RH Balances Ambition With Slowing Growth

4:41 pm — RH -19.29% today

By Asit Sharma

Team Rule Breakers

Shares of luxury furnishings brand RH (RH 19.29%) are heading downmarket today, as per-share earnings of $1.53 missed consensus expectations by roughly 30%, and revenue advanced by a meager 3.7%. Investors also balked at RH’s near-term outlook: Fiscal first-quarter 2026 revenue is projected to decline by 2% to 4% over the prior year.

Closing Bell

4:07 pm

Stocks rose to start the month of April as investors priced in a potential near-term end to the U.S.-Iran conflict, extending a “Hormuz Hope” rally. The Nasdaq led gains, while oil prices fell as supply fears eased. President Donald Trump said the U.S. could leave Iran in “two or three weeks,” and claimed Iran had sought a cease-fire. Still, conditions remain fluid: Trump said the Strait of Hormuz must be “open, free, and clear,” while an Iranian official countered it would reopen “but not for you!”

- Oil’s Signal Flip: Crude’s drop suggests traders see lower disruption risk, easing inflation pressure but challenging energy-sector momentum.

- Volatility Isn’t Done: As one strategist put it, markets are “sniffing out” a resolution—but without an “all-clear,” swings may persist.

Data Center Debt Gets Harder

3:39 pm — ORCL -0.99%

Shares of Oracle (ORCL 1.22%) are under the microscope as a $16 billion financing package for a Michigan AI data center nears completion—highlighting both surging demand for AI infrastructure and growing investor skepticism. The project, backed by Blackstone (BX 0.54%) and debt led by Bank of America (BAC +1.07%), is part of Oracle’s broader, capital-intensive push to support OpenAI workloads. But tighter lease terms, rising borrowing costs, and lender hesitation suggest Wall Street is becoming more cautious about funding the AI buildout—even as Oracle doubles down.

- Debt Gets Pricier: Financing spreads have widened to near junk-bond levels, signaling rising perceived risk around AI infrastructure bets.

- Growth vs. Balance Sheet: Oracle’s AI expansion is driving revenue—but also negative free cash flow and increasing credit pressure.

Today’s Change

Current Price

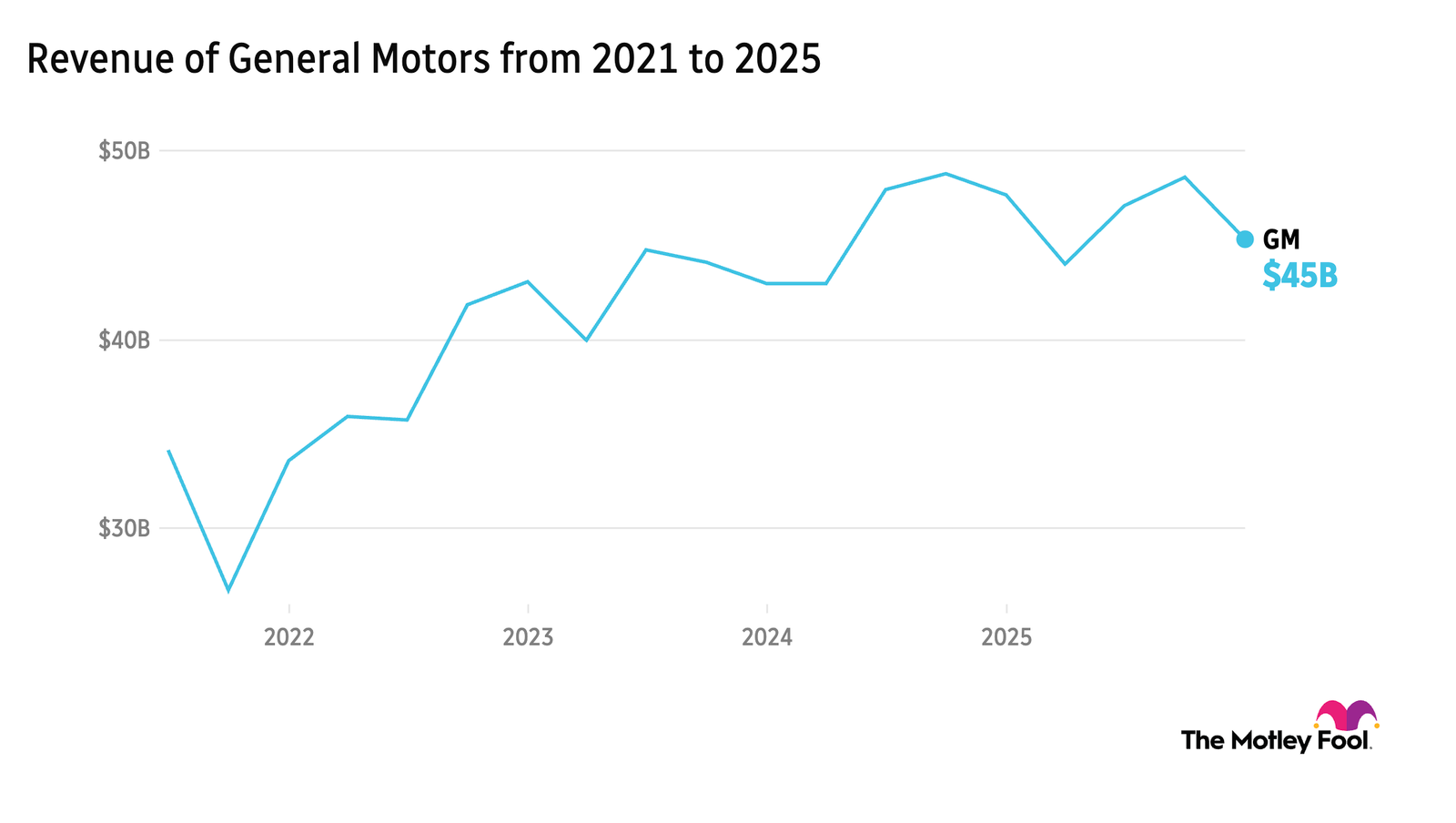

Car Sales Stall Across Industry

3:00 pm — GM +0.44%

Auto demand is hitting resistance. General Motors (GM +0.89%) reported a 9.7% Q1 sales decline—its steepest drop in nearly four years—as high rates, rising prices, and fading EV incentives cooled buyers. (GM’s sales surged 17% a year ago.) Industrywide, U.S. new-vehicle sales are expected to fall ~7%, with weakness spreading across Ford Motor (F +1.21%) and Tesla (TSLA +2.59%). As Motley Fool contributor Jason Hall said of GM on a recent Scoreboard video, “The margins are thin, the capital demands are extremely high… [and] it’s also viciously cyclical,” with EV transition costs already running into the billions.

- Affordability Crunch Tightens: Record financing (~$43.9K) and higher insurance costs are stretching consumers, slowing purchase decisions.

- Capital Cycle Pressure: Automakers are balancing today’s profits with heavy EV investment—an expensive guessing game on future demand.

Oil Dip Could Mask Bigger Risk

2:41 pm — CVX -4.53%

★ CVX is recommended in Dividend Investor as a Foundational Stock

Shares of Chevron (CVX 4.50%) fell after crude prices dipped below $100 on hopes of a near-term pause in U.S. conflict with Iran. The pullback highlights how tightly energy stocks are tracking short-term oil moves—but the broader setup remains uncertain. The Strait of Hormuz, a critical artery for global energy flows, is still largely closed, and any prolonged disruption could constrain supply and support higher-for-longer prices. As an integrated major, Chevron remains positioned to benefit not just from crude prices but also from refining margins in a constrained market.

- Beyond Crude: Integrated players like Chevron can capture upside from both upstream pricing and downstream spreads.

- Bottleneck Still Intact: A significant share of global oil and LNG trade remains disrupted, limiting near-term supply relief. As Motley Fool analyst Yasser El-Shimy wrote recently, “The lack of a time horizon as to when this ends, and the apparent Iranian determination to exact a high and protracted cost against U.S. allies, may signal a longer-than-expected global energy crisis. The fact that major producers like Russia are also under sanctions by the U.S. and the EU makes the energy outlook even dimmer.”

Today’s Change

Current Price

Memory Stocks Snap Back

2:06 pm — MU +10.22%, SNDK +11.02%

Shares of Sandisk (SNDK +9.07%) surged alongside Micron Technology (MU +8.96%) after a bullish note from Cantor Fitzgerald helped spark a relief rally across the memory sector. The move follows recent pressure tied to Alphabet‘s (GOOG +2.80%) new TurboQuant compression algorithm, which initially raised concerns about reduced storage demand. Cantor’s reaffirmed confidence in Micron appears to have shifted sentiment, lifting peers like Sandisk in tandem.

- Efficiency Begets Demand: Greater efficiency from compression tech could actually increase overall data usage—and memory demand. “Memory has become so expensive it’s literally flatlining wide swaths of consumer electronics as all available production capacity is turned toward the highest-price stuff — IA-chasing modeules,” Motley Fool analyst Seth Jayson recently wrote, noting that “Even Nvidia (NVDA +0.77%) can’t supply its formerly-flagship PC GPUs properly.”

- Energy Shock Edge: Geopolitical advantages were among factors that inspired confidence for Cantor. Constraints tied to Middle East tensions may favor U.S. chipmakers over energy-dependent Asian rivals.

Today’s Change

Current Price

AI vs. Chargebacks: Visa’s $106M Move

1:30 pm — V -0.5%

Visa (V 1.23%) is deploying six new artificial intelligence tools to automate the increasingly bloated charge dispute process. The payments giant processed 106 million disputes in 2025 — a 35% surge since 2019 — taxing the manual back-office systems of merchants and banks alike. By using generative AI to draft merchant responses and predictive models to flag “unfamiliar” charges for cardholders, Visa aims to transform a reactive, costly headache into a proactive digital workflow. This efficiency drive mirrors aggressive tech spending at JPMorgan Chase (JPM +0.35%), Goldman Sachs (GS +1.68%), and BNY (BK +1.97%), as the financial sector pivots toward a leaner, AI-augmented labor model.

- The Margin Protector: By automating document summaries and autofill for issuers, Visa is effectively offloading manual labor costs to silicon, shielding profit margins from the rising volume of global transaction friction.

- Proactive Resolution: New “Order Insights” tools will allow merchants to resolve customer confusion mid-transaction, potentially stopping a dispute before it ever hits the expensive formal litigation stage.

Today’s Change

Current Price

Today’s Lunchtime News

1:15 pm — LLY +5.6%, NVO -0.2%

Eli Lilly (LLY +3.78%) received FDA approval Wednesday for Foundayo, its once-daily weight-loss pill, intensifying the competition with Novo Nordisk (NVO 0.82%), which launched its own obesity pill earlier this year. Lilly shares rose as much as 5.6% on the news while Novo shares slipped as much as 2%.

- Race to pills: Foundayo will cost $149 a month for cash-paying patients and analysts project sales could reach $18 billion by 2030. The pill market is expected to drive the broader GLP-1 market past $100 billion by 2030 as oral options lower barriers to treatment. Lilly says it has already produced billions of doses to ensure a swift launch.

- Head to head: Novo’s pill leads to slightly more weight loss — about 13.6% versus Lilly’s 11% in separate trials — but Lilly’s comes with fewer dosing restrictions. Novo’s pill must be taken on an empty stomach with a sip of water, with a 30-minute wait before eating. Lilly’s has no such limits, a distinction doctors say could matter significantly for patient adherence.

Can Intel Finally Catch Up?

12:25 pm — INTC +9.7%

Intel (INTC +8.78%) shares surged 10% after announcing a $14.2 billion deal to repurchase the 49% stake in its Irish Fab 34 facility from Apollo Global Management (APO 1.05%). This reversal of a 2024 capital-raising move signals renewed financial discipline and confidence in the “CPU renaissance.” As agentic AI shifts compute needs, industry leaders like Nvidia (NVDA +0.77%) and AMD (AMD +3.32%) are highlighting a “quiet supply crisis” where traditional processors are becoming the bottleneck. Intel’s move to consolidate its manufacturing footprint comes as its advanced 18A node in Arizona begins production, positioning the firm to capitalize on a projected surge in general-purpose AI compute demand.

- The Agentic Tailwind: Unlike LLM training which favors GPUs, the rise of autonomous AI agents requires massive sequential processing power, potentially allowing CPU growth to outpace graphics chips by 2028.

- Foundry Independence: By reclaiming full ownership of the Irish plant, Intel strengthens its unique IDM 2.0 model, aiming to prove it can both design world-class silicon and manufacture for a global market increasingly desperate for diversified supply.

Retail Investors Get 20% of SpaceX

11:50 am

SpaceX has confidentially filed for what could be the largest IPO in history, targeting a June listing with a valuation potentially hitting $1.5 trillion. The space giant, bolstered by the high-margin profitability of its Starlink satellite wing, expects to raise up to $75 billion. In a move echoing his history with Tesla (TSLA +2.59%), Elon Musk reportedly plans to allocate 20% of the offering to retail investors — double the industry standard. The capital influx will fund “orbital data centers,” a pivot toward space-based AI computation following a strategic shift from Mars colonization to more financially feasible lunar and satellite infrastructure goals.

- The Terafab Connection: A new joint venture with Tesla will consolidate semiconductor production in Austin, designing “hardened” chips to power everything from Tesla’s Robotaxis to SpaceX’s orbital data centers and xAI.

- The Compute Frontier: Musk is betting that moving AI processing into orbit will drastically lower costs compared to Earth-bound facilities, potentially tethering SpaceX’s future valuation to the global AI infrastructure race.

Small Biz Leads Hiring, Health Care Jobs Surge

10:20 am

Private sector employment grew by 62,000 in March, according to data from Automatic Data Processing (ADP 0.94%), easily topping the Dow Jones consensus of 39,000. While large firms shed 4,000 positions, small businesses with fewer than 50 employees proved resilient, adding 85,000 jobs to “catch up” with inflation-driven demand. Education and health services led the charge with 58,000 gains, partly rebounding after a resolved strike at the private nonprofit Kaiser Permanente. Despite the beat, manufacturing and transportation sectors shed nearly 70,000 combined roles, suggesting a stark divergence between service-sector strength and industrial softness ahead of Friday’s official federal jobs data.

- Small-Cap Hiring Engine: Small firms are dominating the labor market for a second straight month, potentially signaling that consumers are seeking secondary income sources to keep pace with persistent price levels.

- The Health Care Moat: Nela Richardson, ADP Chief Economist, notes health care is fundamentally “transforming” the market; the sector’s consistent hiring provides a defensive floor for the economy even as trade and transport face significant headwinds.

Opening Bell

9:35 am

Wall Street opened April with gains as the Dow added 363 points on hopes of a Middle East resolution. President Trump revealed that Iran has requested a ceasefire, though he maintains that military operations will continue until the Strait of Hormuz is “open, free, and clear.” Oil prices responded by retreating, with West Texas Intermediate dipping to $100 per barrel. While the S&P 500 and Nasdaq climbed on the prospect of a U.S. exit within weeks, investors remain wary of a 9 p.m. ET presidential address that could dictate the market’s direction for the new quarter.

Top of the Morning

9:30 am — NKE -11.4% in pre-market trading

By Andy Cross

Motley Fool CIO

It’s been about a year since Elliot Hill rejoined Nike (NKE 15.51%) as CEO to light a fire under the world’s largest athletic apparel company. While it’s still smoldering, there are some sparks. As we reported earlier, Q3 sales were flat with strength in wholesale but DTC (direct-to-consumer) dropped. Back out currency impacts and growth was even worse. Yet the Win Now program Hill put in place is starting to take shape.

Nike Running grew 20% and is the paragon of success for the turnaround plans. Football/Soccer with the North American-hosted World Cup will be next. Wholesale is starting to see some life again after a few years of pivoting more to direct selling. Share and shelf space are growing. They have been rebuilding those critical relationships, and that is showing in strong North America performance. That’s not just a flip-the-switch strategic change. After focusing much more on selling to consumers at the expense of wholesale partners like Dick’s Sporting Goods (DKS 3.26%), Hill and his team are flipping the page in the playbook.

Bank of America is an advertising partner of Motley Fool Money. JPMorgan Chase is an advertising partner of Motley Fool Money. This article was created using Large Language Models (LLMs) based on The Motley Fool’s insights and investing approach. It has been reviewed by our AI quality control systems. Since LLMs cannot (currently) own stocks, it has no positions in any of the stocks mentioned. Andy Cross has positions in Alphabet, Nvidia, and Tesla. Asit Sharma, CPA has positions in Advanced Micro Devices, Intel, Nvidia, and Oracle. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Blackstone, Chevron, Goldman Sachs Group, Intel, JPMorgan Chase, Micron Technology, Nike, Nvidia, Oracle, Tesla, and Visa. The Motley Fool recommends General Motors, Novo Nordisk, and RH. The Motley Fool has a disclosure policy.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)