Besides a critical Federal Reserve announcement, observers are waiting for a flurry of economic reports

- The euro is at risk as inflation and growth data sets the stage for European Central Bank rate cuts.

- The Fed monetary policy meeting is front and center for market-wide risk appetite.

- Wall Street is set to view U.S. jobs data through the lens set by the Federal Open Market Committee outcome.

Stock markets rebounded last week, buoyed by mixed U.S. economic data and an upbeat earnings report from Google’s parent company Alphabet (GOOG). Gold prices took a leg lower as the cycle of escalation between Israel and Iran seemed to be closed. Treasury yields continued to inch higher while the U.S. dollar idled.

Here are the macro waypoints likely to shape price action in the week ahead.

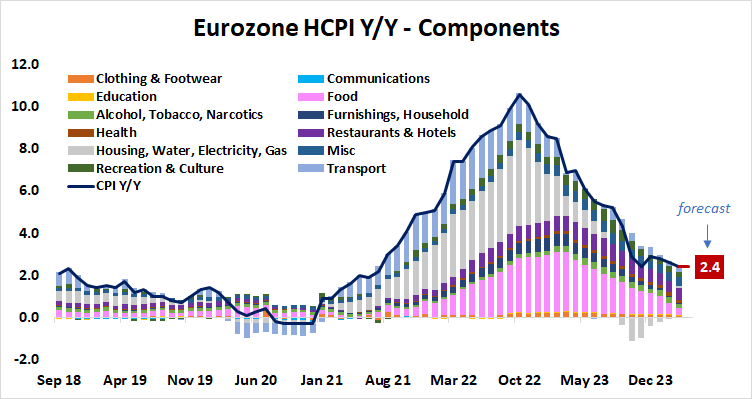

Eurozone CPI and GDP data

Eurozone consumer price index (CPI) data is expected to put price growth at 2.4% year-on-year in April, matching the four-month low set in March. Meanwhile, first-quarter gross domestic product (GDP) numbers are seen showing the economy added a meager 0.1% after stagnating in the last three months of 2023.

Broadening disinflation and barely-there economic growth are likely to reinforce the case for stimulus at the European Central Bank (ECB). That might weigh on the euro. Three standard-sized 25-basis-point (bps) cuts are on the menu for this year, with the first one all but fully priced in for June.

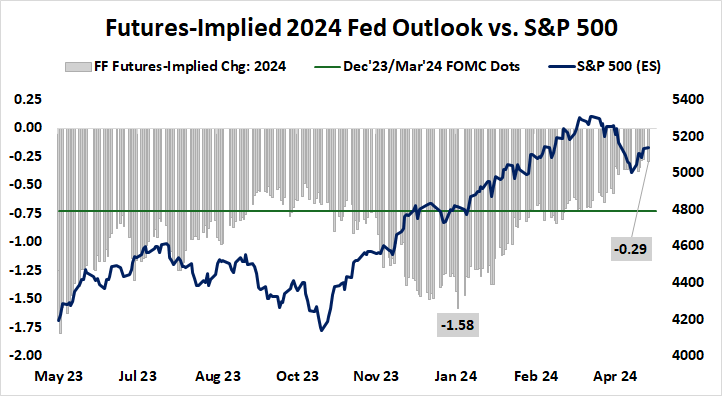

Federal Reserve monetary policy meeting

The U.S. central bank is likely to take top billing on the economic calendar this week. A string of hotter-than-expected inflation readings have eaten away at interest rate cut expectations, with markets now pricing in just 29bps in stimulus this year. That amounts to one 25bps cut and a 16% probability of a second one.

Comments from Fed officials in recent weeks have already started to signal that a hawkish rethink is afoot. Stocks are likely to cheer if Chair Powell and company signal that scope for easing has diminished but some amount of cutting remains on the menu for 2024. That much seems priced in already, and stopping there may be a relief for traders.

The downside risks lurk in the possibility that policymakers open the door for scrapping rate cuts altogether, or even suggest that hiking rates has become an active consideration once again. That is likely to demand repricing from the markets, weighing on Wall Street and sending the U.S. dollar higher.

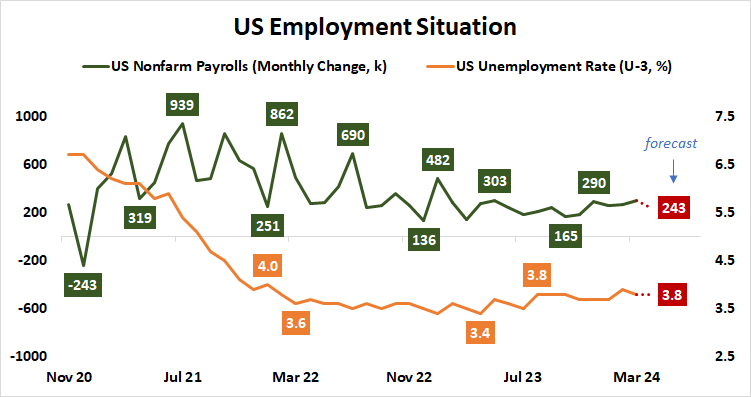

U.S. employment data

The first test of whatever stage-setting is established by the Fed mid-week will come with the release of April’s U.S. jobs report. An increase of 243,000 in non-farm payrolls is expected while the unemployment rate holds steady at 3.8%. That would fall well within the narrow range of outcomes on display since March 2023.

Analytics from Citigroup show that U.S. macro data outcomes have deteriorated relative to baseline forecasts in the past two weeks, warning that economists’ models are tuned rosier than reality has validated. This opens the door for downside surprises. A “risk-on” lead from the Fed may be amplified by such results, while a “risk-off” one is moderated.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.