Stock markets cheer as inflation data lifts Fed rate cut hopes, but global recession risk is brewing in the background

-

Stocks, bonds and metals cheer as the dollar sinks after U.S. inflation data.

-

Hopes for a replay of Q1 enthusiasm may be dashed as global growth slows.

-

Recession fears may reemerge if data from China underwhelms forecasts.

Financial markets squealed with delight as April’s U.S. inflation data printed squarely in line with consensus forecasts.

Perhaps most critically, the core price growth measure resumed the march lower after getting stuck in February and March. It slid to 3.6% year-over-year, the lowest in three years.

Stocks roared higher, posting new record highs on the bellwether S&P 500 index as well as the tech-centric Nasdaq. Bonds pushed higher across maturities, though gains were tilted in favor of the long end. Gold and silver prices raced higher while the U.S. dollar slumped against an average of its major counterparts.

Stock markets cheer as U.S. disinflation underpins Fed rate cuts

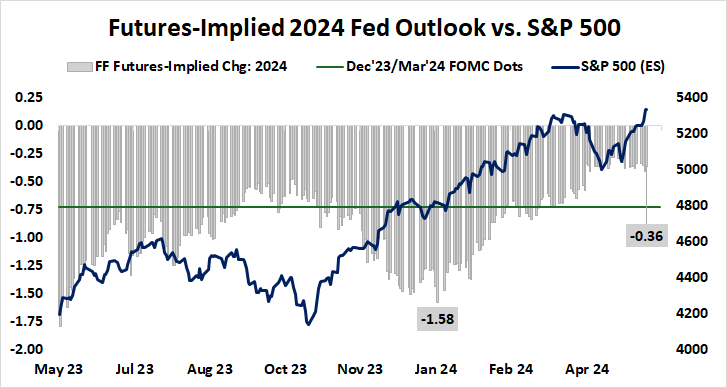

The logic telegraphed in this price action seems straight-forward. The markets concluded that the Federal Reserve looks better positioned to cut interest rates this year now that disinflation has resumed. Fed funds futures are pricing in 37 basis points (bps) for 2024, implying one 25 bps reduction and a 48% probability of a second one.

It’s tempting to conclude that traders should dust off the first-quarter playbook and rerun it. The latest upswell in risk appetite appears to be missing a key ingredient however: the economy itself. Analytics from Citigroup reveal that while U.S. data outcomes were improving in the first three months of the year, they are now floundering.

April’s leading purchasing managers index (PMI) data from S&P Global and the Institute of Supply Management (ISM) paint a worrying picture. The former put the pace of U.S. economic activity growth at a four-month low. The latter showed the first month that manufacturing and services contracted in tandem since December 2022.

This is unwelcome news for a global economy that is largely without a “plan B” for growth absent resilience in the U.S.

The world’s largest economy along with China and the Eurozone make up about 50% of global gross domestic product (GDP). This understates their contribution since much of the rest of the world is made up of vendor economies that depend on demand from the “big three.”

Will weak data from China revive global recession fears?

For the past 12 months, the U.S. has been the essential pillar of support amid weak conditions elsewhere. China is still struggling to reboot after a belated exit from COVID lockdowns. Meanwhile, the Eurozone has only just returned to growth in March after nine months of contracting manufacturing- and service-sector activity.

Incoming data from China may highlight once again that the East Asian giant would struggle to offset a U.S. downturn. Retail sales and industrial production are seen improving in April, but Citigroup warns that outcomes have weakened relative to forecasts in the past month. That may set the stage for disappointment.

This hardly sounds supportive for risk appetite. Stock markets are cheering hopes for a dovish Fed, but that may be a hollow victory if it comes because the threat of global recession has returned. If incoming news-flow underscores as much, burgeoning risk appetite may be quick to dissipate.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)