The German share price index DAX graph is pictured at the stock exchange in Frankfurt, Germany, January 19, 2024.

Staff | Reuters

Over the last 12 months, just 11 stocks made up half of the gains that powered the pan-European Stoxx 600 stock index to a record-high close on Friday.

Earlier this month, Goldman Sachs highlighted that Europe’s stock markets were dominated by this group of “internationally exposed quality growth compounders” with the continent’s largest market caps, which the bank termed the GRANOLAS back in 2020.

The momentum of this group — which comprises GSK, Roche, ASML, Nestle, Novartis, Novo Nordisk, L’Oreal, LVMH, AstraZeneca, SAP and Sanofi — has drawn comparisons to the “Magnificent Seven” U.S. tech giants and evoked similar concerns about concentration risks in European equity markets.

Together, the GRANOLAS account for around a quarter of the total Stoxx 600 market cap, and Goldman analysts in a note last week highlighted that they exhibit qualities that are expected to thrive in the current cycle, such as solid earnings growth, high and stable margins and strong balance sheets.

“We think they also stand to benefit from the structural shift towards passive investment and the lack of liquidity in the European equity market,” the Wall Street bank’s analysts suggested.

“From a Global point of view, the GRANOLAS have even outperformed the so-called Magnificent 7 over the past two years. Their (out)performance is even more impressive on a risk-adjusted basis: with a volatility 2x lower than for the Magnificent 7, the GRANOLAS help to boost the Sharpe ratio.”

They noted that, while the group trades with a high price-to-earnings ratio, a measure that gauges whether a stock is overvalued, this is “not unusual for growth companies” and the GRANOLAS actually trade at a significant discount compared to the Magnificent Seven.

What’s more, Goldman Sachs expects the strong growth momentum to continue, with a 7% revenue compound annual growth rate expected for the GRANOLAS through 2025, compared to 2% for the wider market excluding the group. The 11 stocks also provide dividend yields for shareholders in the 2-2.5% range.

“This suggests that, in Europe, nearly all revenue growth of the STOXX 600 will come from the GRANOLAS. We think this will be sustained by high barriers to entry businesses, solid balance sheets and high investment — they reinvest the same share of cash flows in R&D and growth CAPEX as the Magnificent 7,” Goldman Sachs added.

Such a high and potentially deepening concentration of stock market gains gives rise to concerns about concentration risk, but some analysts believe that the diverse sectors represented in the group may insulate the GRANOLAS to some extent.

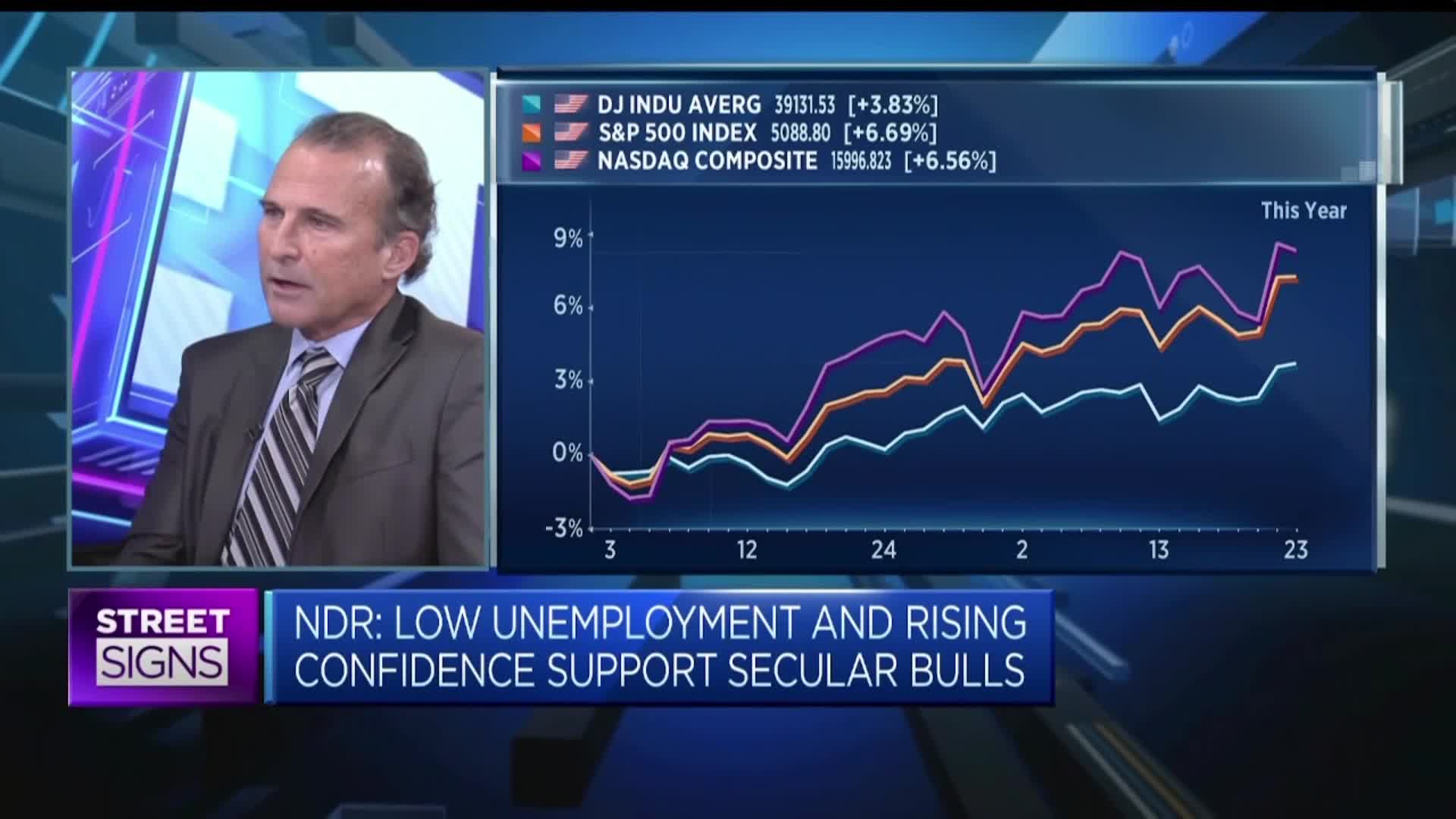

Tim Hayes, chief investment strategist at Ned Davis Research, told CNBC on Monday that, for recent comparisons to the current state of play, market participants should look to the end of 2020, when the market was highly concentrated around a small number of large-cap stocks.

“What happened then was the market broadened out and this brought us into 2021 which turned out to be a very good year, very low volatility — we also had the market broaden out in anticipation of what turned out to be a globally synchronized economic expansion, earnings growth was coming through globally across sectors,” Hayes said.

He suggested this created “a lot of complacency” in the market, which prompted investor confidence to linger despite emerging “divergences” beneath the surface.

“This is what created that very narrow market at the end of 2021, because more and more sectors started to diverge as we started to see signs of these supply chain pressures and the inflationary pressures, commodity prices moving higher, all the things that got us into the 2022 bear market,” Hayes added.

While this does not necessarily have to be a negative indicator right now, he suggested that the longer the current complacency lingers, the more vulnerable the market is to bad news, or the good news that had been priced in failing to come through.

“We’ve seen this recently with the expectation that we’re going to have all these rate cuts, when it turned out, well, maybe we’re not going to have as many rate cuts as the market thought, that set up a little bit of a pullback,” Hayes said.

“That can happen on a bigger scale if the market gets too complacent, and then you’re more vulnerable to some kind of negative surprise entering the picture.”

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)