(Bloomberg) — The great market rally of 2024 looks dangerously close to unraveling as Wall Street’s once-invincible bull brigade begins to withdraw its winnings.

Most Read from Bloomberg

-

US House Passes $95 Billion in Aid to Ukraine, Israel and Taiwan

-

Tesla Cuts US Prices by $2,000 as Sales Slow, Inventories Swell

-

New York’s Rich Get Creative to Flee State Taxes. Auditors Are On to Them

With Treasury yields breaking out, Federal Reserve hawks ascendant and Middle East strife flaring, money has just been pulled out of equities and junk bonds at the fastest rate in more than a year. Dip-buyers have been muzzled. The S&P 500 fell every day this week as the top seven tech behemoths closed nearly 8% lower, with equity volatility climbing.

Fueling the reversal is an uptick in tensions that bulls may be less inclined to brush off after ringing up trillions of dollars in trading profits since late October. First among them is evidence that inflation has supplanted recession as the chief nemesis of central bankers. With commodities surging and economic data stubbornly hot, speakers led by Chair Jerome Powell have poured water on hopes for a long-awaited pivot in monetary policy.

It adds up to a backdrop warranting defense, says Kathryn Rooney Vera, chief market strategist at StoneX Group.

“In a world of high geopolitical risk, upside risk to commodity prices, upside risk to inflation, I think we have to be more conservative in our allocation,” Rooney Vera said by phone. “I would rotate from high-flying equities at this point, and I would put that into really high-yielding short-term paper.”

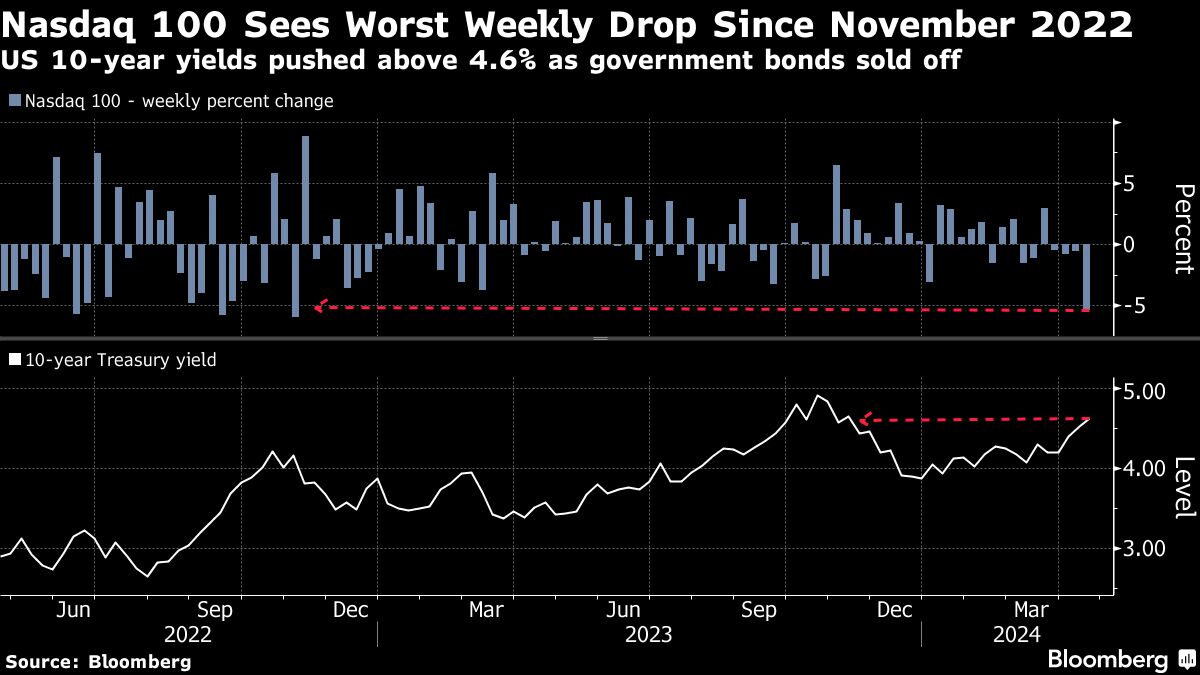

The view suggests oft-ignored valuation imbalances across assets are starting to matter again. With government bonds selling off, the 10-year Treasury rate pushed back above 4.6%, about 40 basis points above the so-called earnings yield of the S&P 500. That gap, the rough basis for a valuation tool known as the Fed model, can be framed as the least favorable for equities since 2002, relatively speaking.

Down six days starting last Friday, the S&P 500 tallied its worst losing streak since 2022, extending its April loss to more than 5%. Two-year Treasuries saw their yield briefly push above 5% on Tuesday, part of a fixed-income rout that has erased gains in high yield- and investment-grade bonds for the month.

Traders this week sensed a deliberate effort by central bankers to restrain bets on imminent easing ahead. Powell said Tuesday that it will probably take “longer than expected” to gain the confidence needed to lower rates. A day later, Fed Governor Michelle Bowman warned progress on inflation may have stalled. On Thursday, asked if it would be appropriate to hold rates steady all year, Minneapolis Fed President Neel Kashkari answered: “potentially.”

Hawkish posturing fanned selling pressure that has been building across investor ranks. Redemptions from stock funds reached $21.1 billion in the two weeks through Wednesday, the most since December 2022, according to Bank of America citing data from EPFR Global. Investors pulled cash out of junk bonds at the fastest pace in 14 months, according to data from LSEG Lipper. Hedge funds ramped up short positions in US exchange-traded funds at the fastest pace since 2022, Goldman Sachs Group Inc.’s prime brokerage data show.

“There are weak hands selling, and will continue to sell, since they weren’t enthusiastic to buy in the first place,” said Peter Tchir, head of macro strategy at Academy Securities Inc. “People got sucked into chasing the rally, buying stocks at high valuations, now, a month or so later, the trades aren’t working.”

Market-implied expectations for monetary easing have collapsed in the past two weeks as traders price in less than two rate cuts this year. That’s down from as many as six earlier in 2024.

Tensions in the Middle East have reinforced the more cautious stance. Israel reportedly struck back at Iran on Friday morning and while the latest tensions were contained, worries remain about a wider war in a region already roiled by the Israel-Hamas conflict that could send oil prices above $100 a barrel.

Investors today face a pile of risks that they have shown themselves able to live with previously thanks to resilient corporate earnings and spirited economic growth. The S&P 500 is up 16% since Hamas attacked Israel, 17% since the 10-year Treasury yield’s 2023 peak, and about 20% since the Fed began raising rates two years ago.

Yet the sheer scale of market gains now threatens to work against risk assets, going forward.

Valuation worries are building within the equity ecosystem, particularly the Nasdaq 100, whose seven biggest members saw the worst weekly drop since November 2022. Cheaper-looking companies have been back to outperforming their often artificial-intelligence-enhanced growth counterparts. The Russell 1000 Value Index fell 0.7% on the week compared to a 5% drop in its growth counterpart.

“There has been a tremendous amount of faith-based investing into AI that pushed up valuations of many megacap tech firms,” said Max Gokhman, head of MosaiQ Investment Strategy at Franklin Templeton Investment Solutions. “A value overweight looks increasingly more attractive and it’s something we are actively discussing.”

–With assistance from Lu Wang.

Most Read from Bloomberg Businessweek

-

What Really Happens When You Trade In an iPhone at the Apple Store

-

Rents Are the Fed’s ‘Biggest Stumbling Block’ in Taming US Inflation

-

Aging Copper Mines Are Turning Into Money Pits Despite Demand

©2024 Bloomberg L.P.