Trimble (TRMB) saw renewed attention after Barclays began coverage with a positive outlook. The firm highlighted the company’s evolving software strategy, growing recurring revenue, and uptake of AI across its platforms.

See our latest analysis for Trimble.

After a stretch of upbeat analyst coverage and new strategic partnerships, Trimble’s momentum seems to be building. The stock’s 11.95% year-to-date share price return hasn’t told the whole story, as its 26.44% total shareholder return over the past year signals robust long-term gains and increasing investor confidence in the company’s shift toward software and AI-driven solutions.

If Trimble’s growth story has you scanning for the next tech mover, consider exploring the full list of high-growth innovators in our tech and AI screener: See the full list for free.

With upbeat analyst ratings and strong long-term returns, is the market underestimating Trimble’s next wave of growth, or has the recent run-up already captured the company’s future potential, leaving little room for a bargain?

Most Popular Narrative: 20.2% Undervalued

With the most followed narrative estimating fair value at $97.75, Trimble’s last close at $78.04 suggests significant upside according to this outlook. The following quote gives a glimpse into a key driver of the story.

The migration from hardware-focused, CapEx models to bundled, subscription-based offerings, even in traditionally hardware-oriented segments, expands the addressable market, improves revenue visibility, and increases recurring revenue mix. This drives greater predictability and enhanced long-term earnings.

Curious about the financial engine behind this valuation? The most influential assumptions hinge on a bullish view of recurring earnings and margin expansion. The full narrative reveals exactly how analysts envision this software-powered transformation propelling Trimble’s value far above its current share price.

Result: Fair Value of $97.75 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, persistent macroeconomic headwinds or delays in customers adopting subscription models could undermine Trimble’s growth outlook and present challenges to optimistic forecasts.

Find out about the key risks to this Trimble narrative.

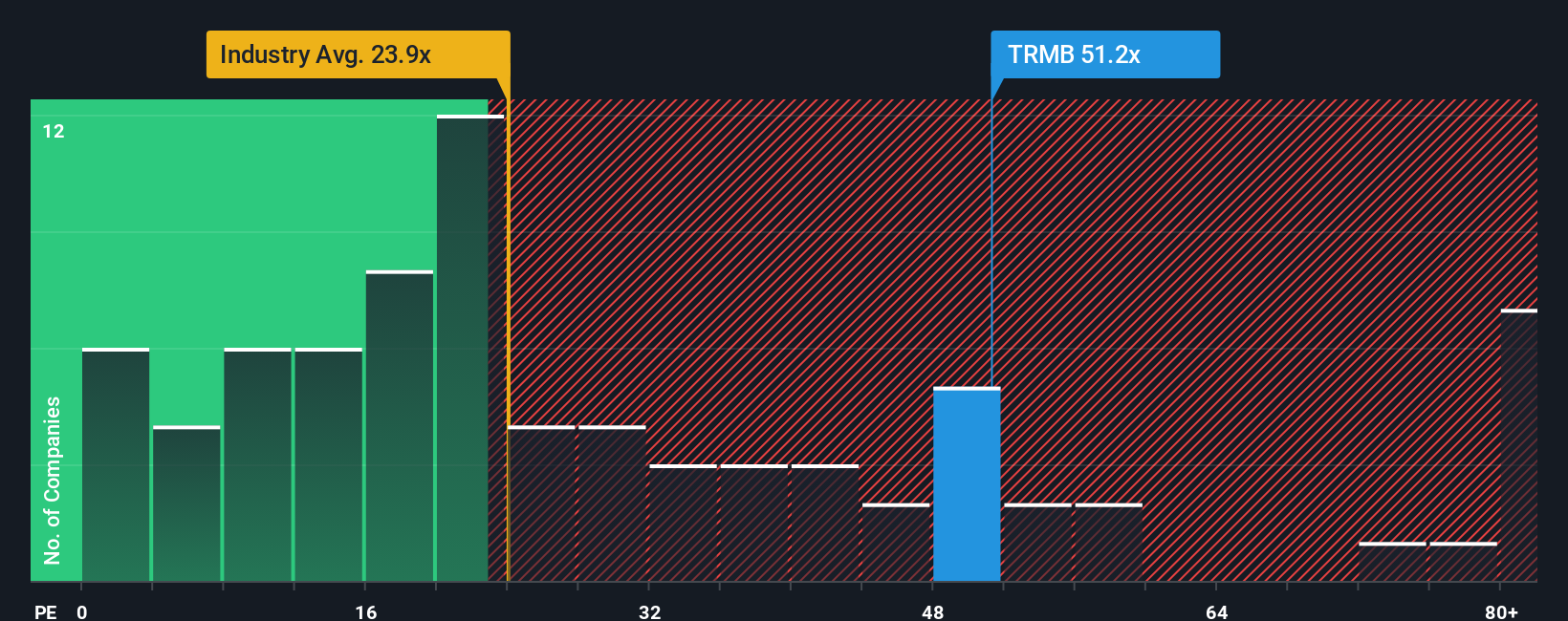

Another View: The Multiples Perspective

While analysts see Trimble as significantly undervalued, a look at its price-to-earnings ratio raises some concerns. The stock trades at 64 times earnings, which is well above both its peer average of 42.2 times and the US Electronic industry average of 24.9 times. The fair ratio, estimated at 35.7 times, suggests the current premium could amplify downside risk if expectations ease. Does high optimism leave investors exposed if growth or margins disappoint?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Trimble Narrative

If you want a different perspective or prefer to dig into the numbers yourself, you’re free to shape your own view with just a few clicks. Do it your way.

A great starting point for your Trimble research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Great opportunities are waiting if you know where to look. Give yourself an edge by acting now. Here are three routes to strengthen your portfolio:

- Unlock the potential of early-stage innovators by checking out these 3573 penny stocks with strong financials that combine growth with solid finances and bold strategies.

- Capitalize on reliable income streams and long-term compounding with these 18 dividend stocks with yields > 3% yielding above 3%.

- Stay ahead in the AI revolution by evaluating emerging leaders through these 25 AI penny stocks shaping tomorrow’s digital transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Trimble might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

![i’m-nervous,-too!-[part-2]](https://10xwealthreport.com/wp-content/uploads/2026/03/177042-im-nervous-too-part-2-1568x784.jpg)