Thanks to tariffs, huge spending, and pressure on the Federal Reserve, the Trump administration has injected a great deal of uncertainty into global financial markets. But things went a step further on Feb. 28 when the U.S. and Israel began strikes on Iran. Let’s explore what this could mean for stocks and the crude oil market.

How does war affect stocks?

There is some data on the stock market during wartime — including this research from The Motley Fool — but there isn’t a clear relationship between military conflicts and stock market performance. While some economists credit World War II with helping end the Great Depression and setting the stage for an economic boom in the 1950s, investors shouldn’t expect military conflicts to have such a big impact (either positive or negative) on modern economies because systems are much more complex now, and current wars are less widespread than World War II.

Large-scale conflicts such as the Russian invasion of Ukraine that started in 2022 didn’t lead to a sustained decline in global stocks. In fact, the STOXX Europe 600, an index that tracks a basket of eurozone equities, has risen by over 30% since the invasion.

Image source: Getty Images.

I expect a similar story to play out with the current Iran war, as the market focuses on things like consumer spending and capital spending related to generative artificial intelligence, which will have a more direct impact on corporate earnings over the next few years.

Could things change?

While the Iran war doesn’t look like a huge downside risk to stocks and the economy right now, that could change if it expands into a full-fledged ground operation. According to an analysis from Brown University, the post-9/11 20-year “war on terror” cost the U.S. an eye-popping $8 trillion.

We don’t know what the latest war will end up costing, but rising U.S. debt levels could shake investor confidence in the dollar and cause Treasury bond yields to spike. If Treasury yields jump, it could increase capital costs throughout the economy and reduce the valuations of growth stocks, as those companies often aren’t able to fund their operations with internal cash flow.

What about oil?

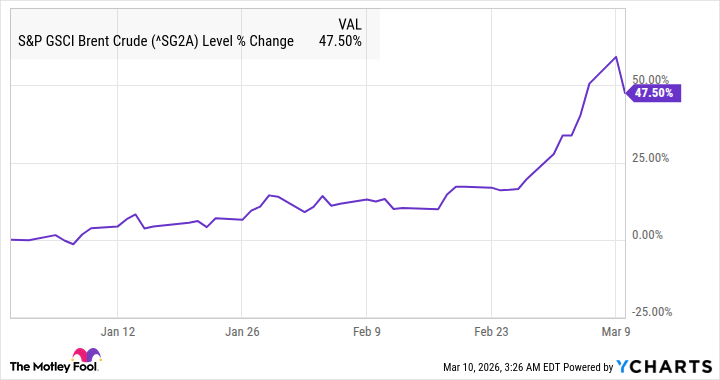

The current war’s influence on oil markets is much clearer. Iran is the ninth-largest oil producer in the world, with 3.99 million barrels per day in 2023 (4% of the total), and some of the country’s oil facilities have already been attacked — alongside facilities in neighboring countries. That reduces supply, which leads to higher prices. And Iran has closed the Strait of Hormuz, a key oil transport route, putting more pressure on oil supplies.

The price of Brent Crude is up roughly 48% since the start of 2026 as I write this.

That said, the U.S. is the world’s top oil producer (22% of the total in 2023), and this dramatically limits the impact of supply problems in other parts of the world. Rising oil prices will spur U.S. producers to increase their output. It will also increase the incentive to develop other sources in the Western Hemisphere, like those in Guyana and Venezuela.

And don’t forget, the White House is incentivized to help increase the amount of oil in the market to offset the disruption caused by what’s happening in the Middle East. It makes sense to take a wait-and-see approach to the Iran war’s impact on the equity and crude oil markets.