Pool’s stock price has taken a beating over the past six months, shedding 20.8% of its value and falling to $190.29 per share. This might have investors contemplating their next move.

Is now the time to buy Pool, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Pool Will Underperform?

Even though the stock has become cheaper, we’re swiping left on Pool for now. Here are three reasons why POOL doesn’t excite us, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

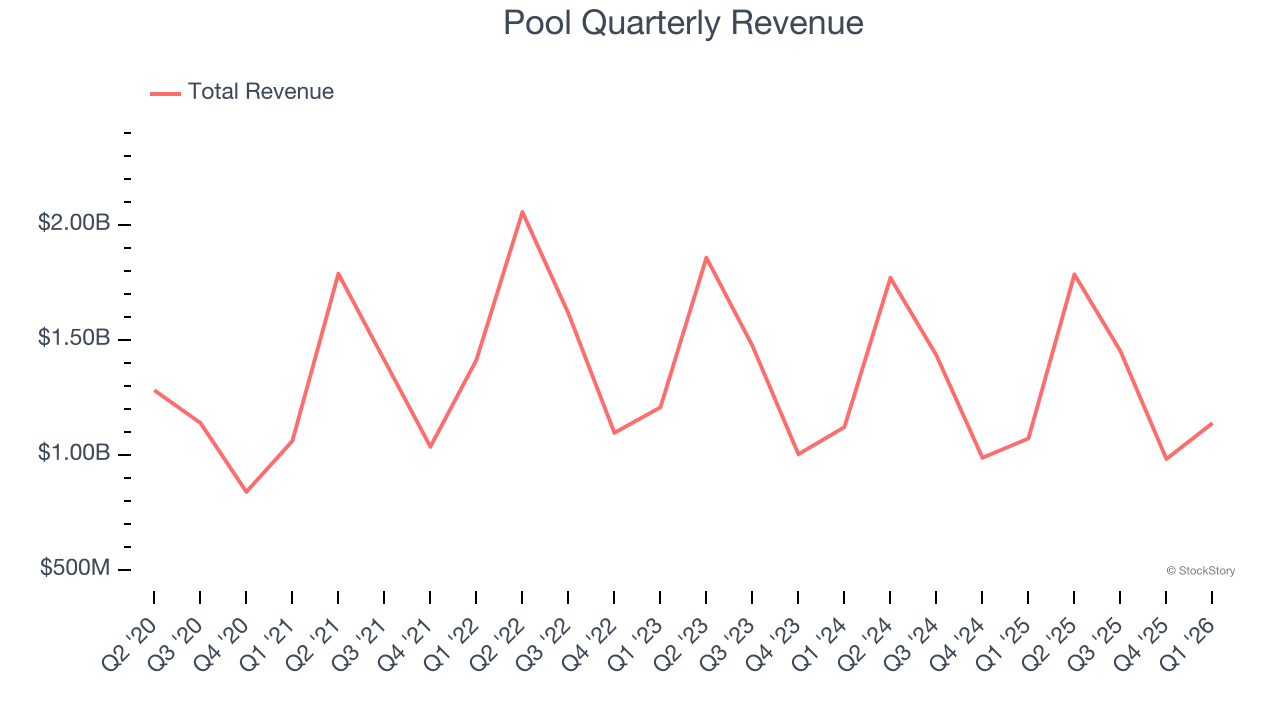

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Pool’s 4.4% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector.

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

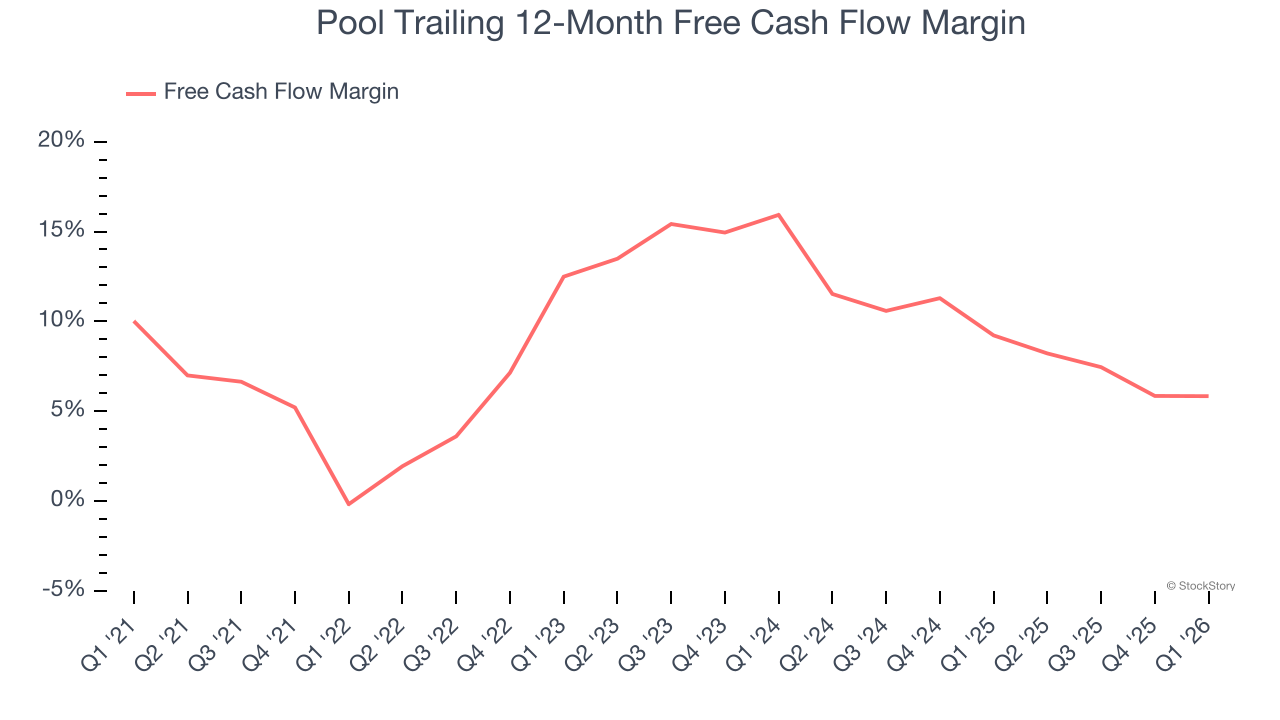

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Pool has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 7.5%, below what we’d expect for a consumer discretionary business.

3. New Investments Fail to Bear Fruit as ROIC Declines

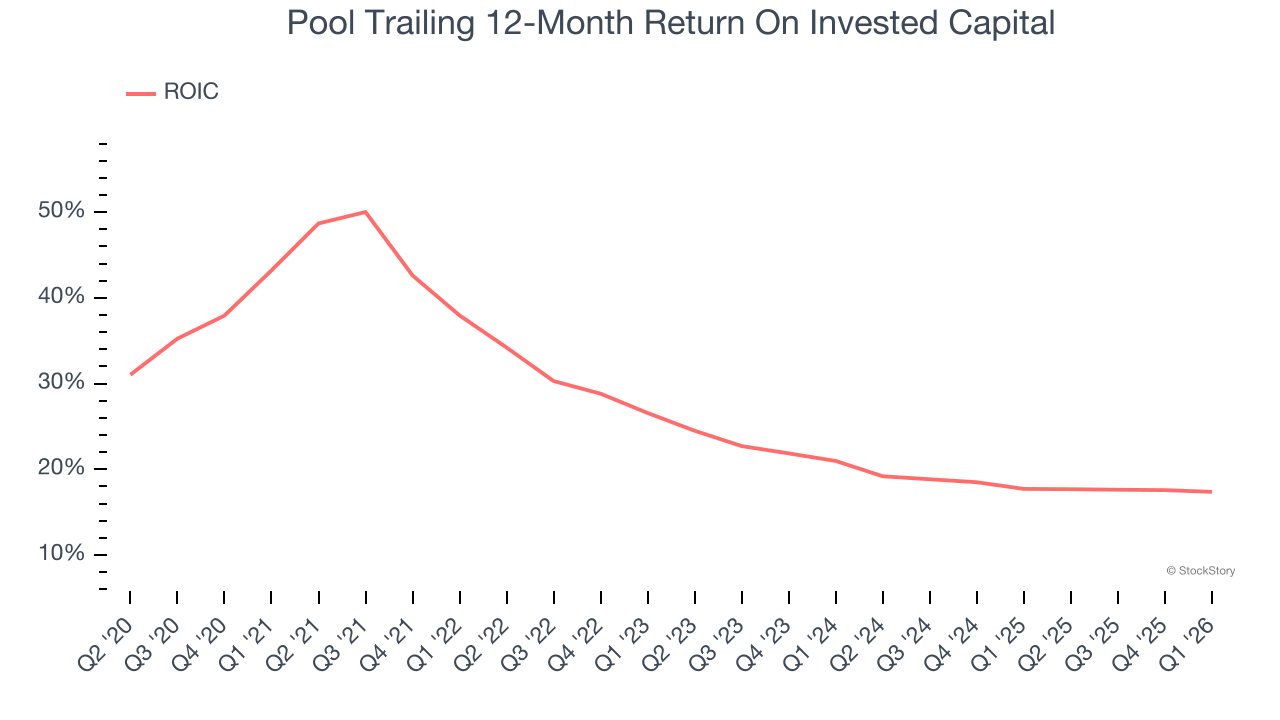

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

Over the last few years, Pool’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

We see the value of companies helping consumers, but in the case of Pool, we’re out. Following the recent decline, the stock trades at 16.9× forward P/E (or $190.29 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in – we think there are better opportunities elsewhere. We’d recommend looking at a dominant aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.