Over the past six months, Cushman & Wakefield’s shares (currently trading at $13.27) have posted a disappointing 15.9% loss, well below the S&P 500’s 10% gain. This might have investors contemplating their next move.

Is now the time to buy Cushman & Wakefield, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Cushman & Wakefield Will Underperform?

Even with the cheaper entry price, we’re swiping left on Cushman & Wakefield for now. Here are three reasons we avoid CWK, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

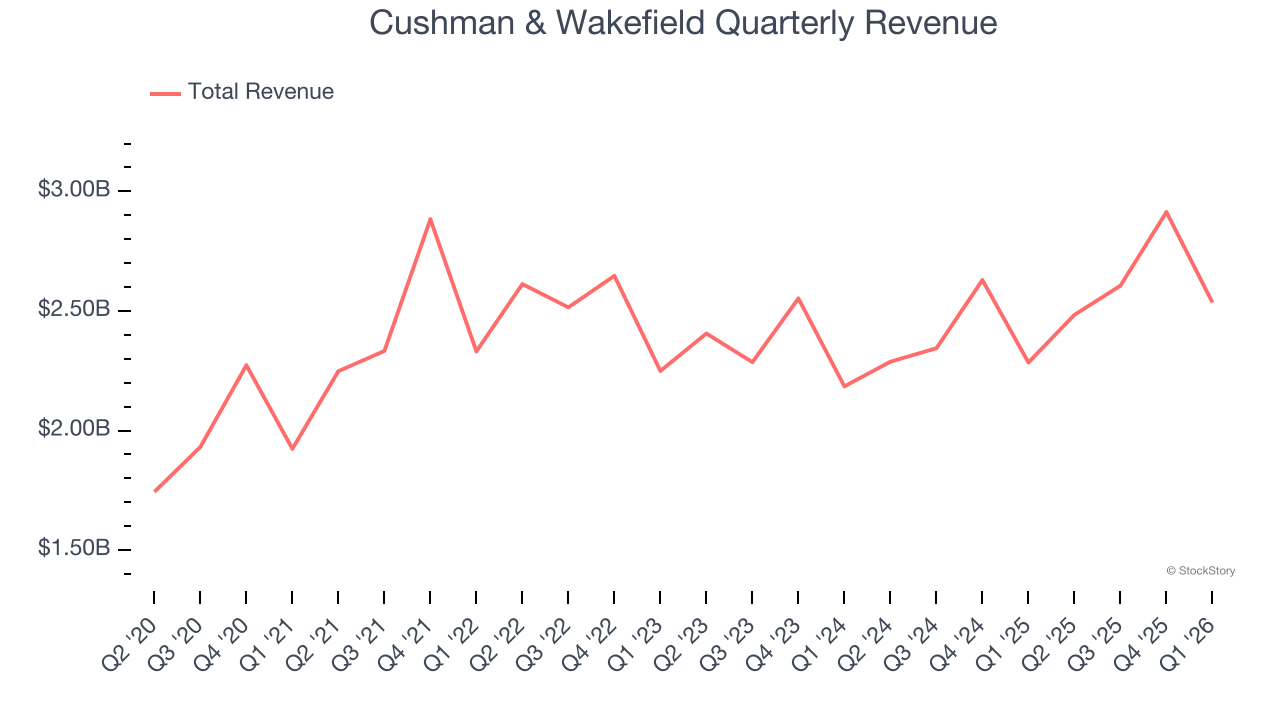

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Cushman & Wakefield’s sales grew at a weak 6% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector.

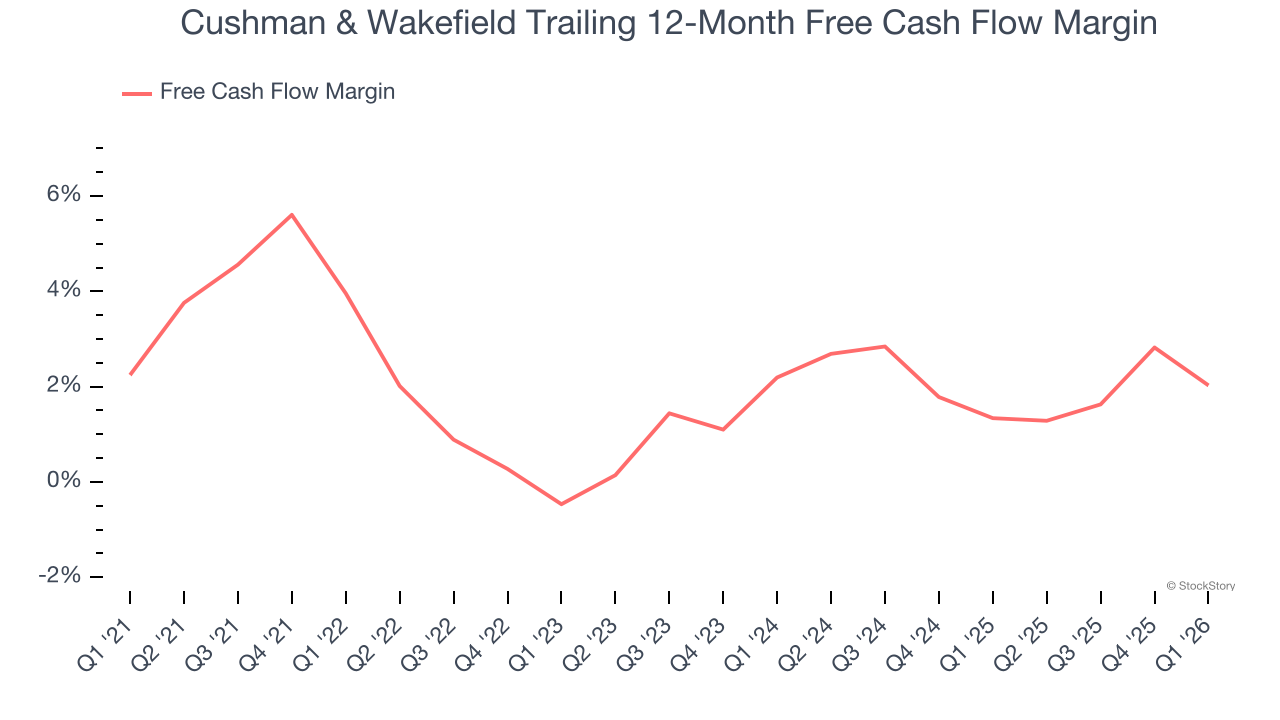

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Cushman & Wakefield has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.7%, below what we’d expect for a consumer discretionary business.

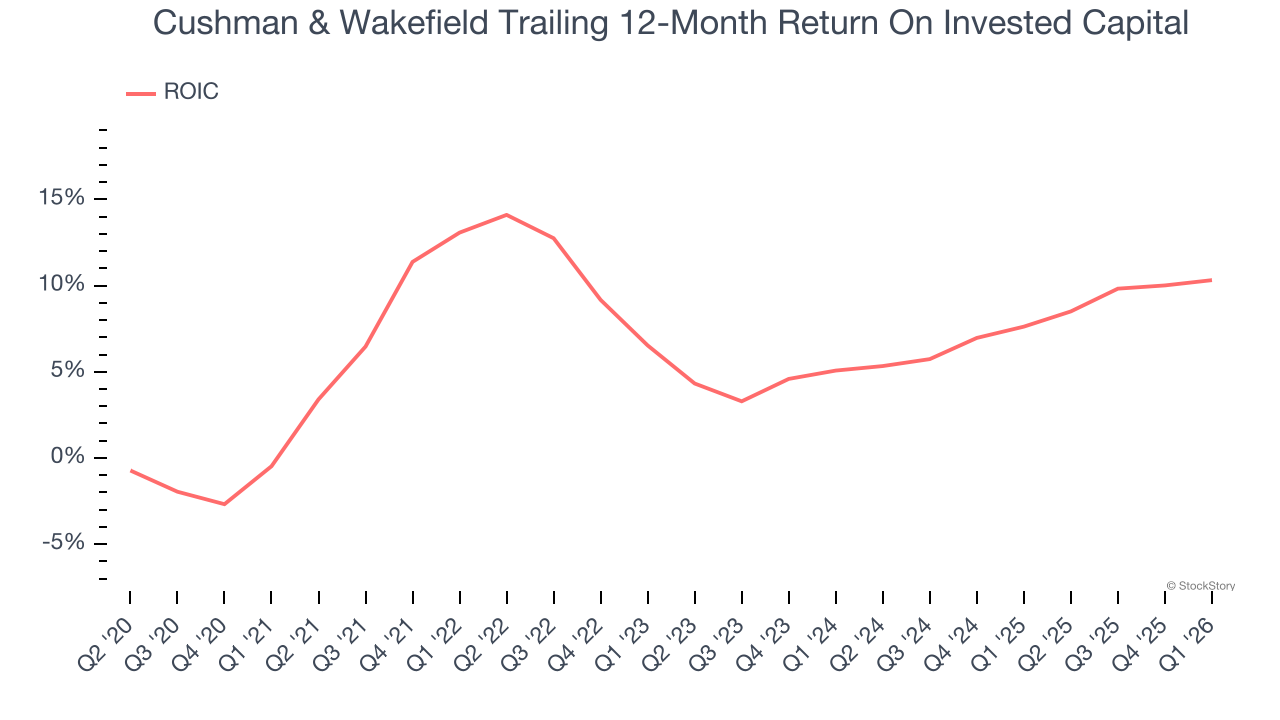

3. New Investments Aren’t Moving the Needle

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Cushman & Wakefield’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

Final Judgment

Cushman & Wakefield falls short of our quality standards. After the recent drawdown, the stock trades at 8.6× forward P/E (or $13.27 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Cushman & Wakefield

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.