Ermenegildo Zegna (NYSE:ZGN) is getting fresh attention after JPMorgan Chase & Co. launched its analyst coverage with an upbeat outlook. In addition, several big institutional players have ramped up their positions in the company, catching the eye of anyone scouting for signals of shifting market sentiment. Moves from notable voices and large investors tend to spark both optimism and debate among investors trying to make sense of what might be next for Zegna’s share price.

Momentum has been picking up over the past month, with Zegna’s stock climbing 15% and extending its year-to-date gain to 19%. Over the past year, shares are up 14%, which points to steady (if not explosive) progress, especially considering the negative three-year return. The renewed analyst coverage, along with recent institutional buying, suggests that investors may be rethinking the company’s longer-term prospects and risk profile.

With Zegna seeing stronger interest and its share price on the move, the question remains whether this is a true buying opportunity, or if the market is already factoring in the next stage of growth.

Most Popular Narrative: 3% Undervalued

The most popular narrative suggests that Ermenegildo Zegna is modestly undervalued, with recent analyst consensus price targets slightly above current trading levels.

The Tomas Maier-led TOM FORD fashion line’s strong media and customer reception, along with plans to expand women’s and accessories collections, indicates potential future revenue growth and diversification. This could positively impact gross margins.

What hidden factors are fueling this higher fair value? The narrative relies on aggressive forecasts for both profitability and top-line growth, based on category expansion and a premium valuation rarely seen for luxury apparel. Are you interested in the exact metrics behind analysts’ bullish outlook or the bold assumptions supporting this price? Discover which future milestones are making this luxury brand the analyst favorite this year.

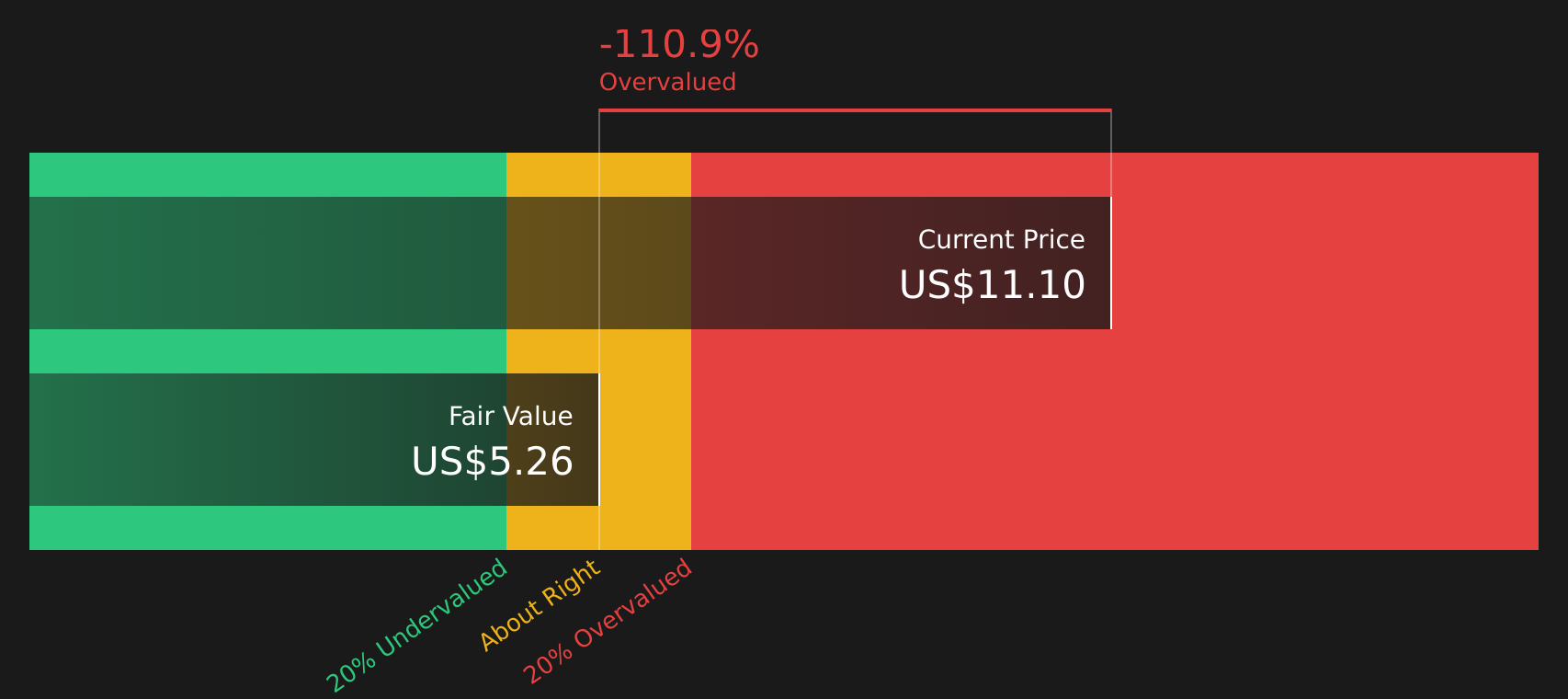

Result: Fair Value of $9.80 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, ongoing weakness in Greater China and declines in Thom Browne’s wholesale segment could challenge Zegna’s ability to deliver on these bullish projections.

Find out about the key risks to this Ermenegildo Zegna narrative.

Another View: Not Everyone Agrees

While analysts see Zegna as undervalued, our DCF model offers a very different perspective. It suggests the shares may actually be priced above their intrinsic value. Which approach better captures the risks and opportunities ahead?

Look into how the SWS DCF model arrives at its fair value.

Stay updated when valuation signals shift by adding Ermenegildo Zegna to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Ermenegildo Zegna Narrative

If you see the numbers differently or want to shape your own perspective, it only takes a few minutes to craft your own analysis, your way. Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Ermenegildo Zegna.

Looking for More Ways to Win?

Don’t limit yourself to just one opportunity. Build a smarter, more powerful portfolio by tapping into unique trends and high-potential market niches with these tailored ideas:

- Unlock the hidden gems of tomorrow’s tech revolution by following the breakthroughs and fast growth found in AI penny stocks.

- Supercharge your returns with steady income from companies boasting strong fundamentals and impressive yields through dividend stocks with yields > 3%.

- Position yourself ahead of the crowd with stocks trading below their true value. Capitalize on fresh opportunities via undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Ermenegildo Zegna might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com