- On March 9, 2026, Life Time Group Holdings announced that Class I director Alejandro Santo Domingo would resign from its board effective March 31, 2026, while KeyBanc Capital Markets began covering the company with an Overweight rating amid favorable fitness-industry conditions.

- The coverage initiation underscores Life Time’s positioning as a premium fitness brand benefiting from rising interest in holistic health and wellness across age groups.

- Next, we’ll examine how KeyBanc’s positive industry view and premium-brand positioning could influence Life Time’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

Life Time Group Holdings Investment Narrative Recap

To own Life Time Group Holdings, you need to believe in its ability to turn a premium, club-centered wellness model into durable cash generation, despite high capital needs and competition from at-home options. KeyBanc’s upbeat initiation and Santo Domingo’s board exit do not appear to alter the near term focus on funding expansion while managing leverage, or the key risk that tighter real estate and credit markets could strain its sale leaseback fueled growth plans.

The recently approved US$500,000,000 share repurchase program is the clearest companion to KeyBanc’s positive coverage, as both highlight confidence in Life Time’s equity story while the company continues opening large, capital intensive clubs like the new Alston Town Center location. How effectively Life Time balances buybacks with debt management and new club spending will remain central to whether today’s premium wellness positioning translates into attractive long term shareholder outcomes.

Yet despite the upbeat premium brand narrative, investors should be aware that Life Time’s reliance on sale leasebacks and sizable expansion capex could…

Read the full narrative on Life Time Group Holdings (it’s free!)

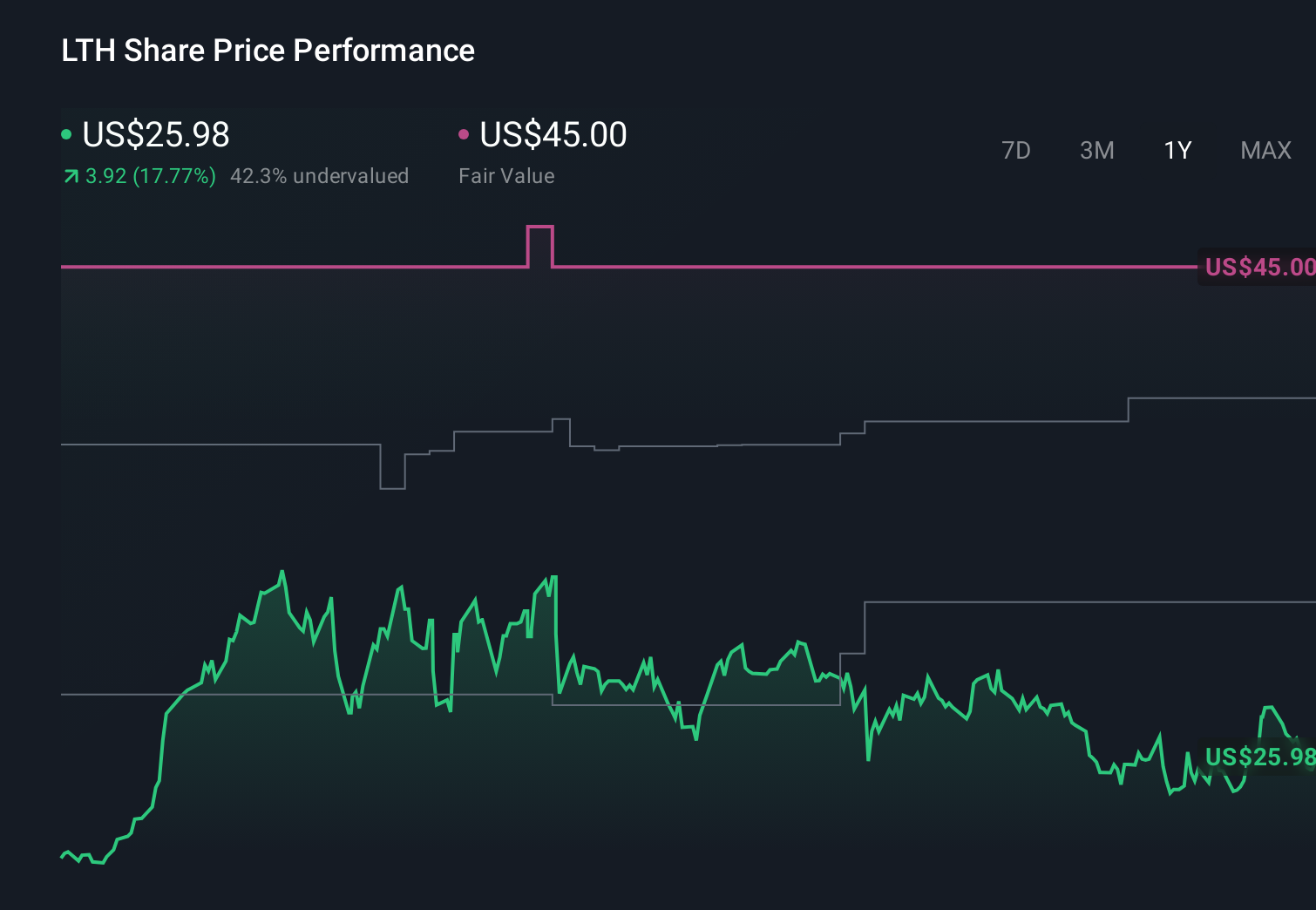

Life Time Group Holdings’ narrative projects $3.8 billion revenue and $457.9 million earnings by 2028. This requires 10.7% yearly revenue growth and a $231.1 million earnings increase from $226.8 million today.

Uncover how Life Time Group Holdings’ forecasts yield a $40.18 fair value, a 55% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much tougher picture, assuming revenue of about US$3.6 billion and earnings near US$361 million by 2028, which is far less generous than consensus and reflects concern that heavy capex and digital bets could weigh on returns; the new KeyBanc coverage and board change may eventually shift both this cautious view and the more optimistic consensus narrative, so it is worth comparing several perspectives before you decide what you believe.

Explore 3 other fair value estimates on Life Time Group Holdings – why the stock might be worth as much as 74% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Life Time Group Holdings’ overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com