Driven by the strong performance of technology stocks, the S&P 500 Index and Nasdaq Composite reached new highs. The Nasdaq 100 Index, which includes the world’s top technology companies and is regarded as a ‘bellwether for tech stocks,’ has risen for 12 consecutive trading days.

According to Zhitong Finance APP, as of the close of the U.S. stock market on Thursday, the S&P 500 Index and the Nasdaq Composite Index surged to record highs, driven by strong gains in technology stocks amidst ongoing geopolitical conflicts in the Middle East, persistent disruptions in oil supply, and warnings from economists that prolonged geopolitical tensions could suppress economic growth.

The S&P 500 Index closed at a record high for two consecutive days on Thursday, with an increase of 11% since the end of March. The Nasdaq 100 Index, which includes the world’s top technology companies and is known as the “barometer of tech stocks,” along with the Nasdaq Composite Index, both rose for 12 consecutive trading days, with the former achieving its longest winning streak since July 2017. Despite the unresolved geopolitical conflict in Iran and the continued blockade of oil shipments through the Strait of Hormuz, global stock markets, including those in the U.S., have demonstrated strong upward resilience.

Although the geopolitical storm in the Middle East has yet to subside, bullish sentiment among Wall Street analysts toward global equity markets has grown increasingly fervent. After experiencing initial waves of sharp sell-offs, institutional investors on Wall Street seem to be filtering out noise related to the conflict, no longer viewing the war as a ‘core variable determining market direction’ as they did in early March, but instead beginning to largely ‘ignore the noise of war.’

Although the geopolitical storm in the Middle East has yet to subside, bullish sentiment among Wall Street analysts toward global equity markets has grown increasingly fervent. After experiencing initial waves of sharp sell-offs, institutional investors on Wall Street seem to be filtering out noise related to the conflict, no longer viewing the war as a ‘core variable determining market direction’ as they did in early March, but instead beginning to largely ‘ignore the noise of war.’

Several financial giants on Wall Street directly attribute the current resilience in the stock market to continuously improving corporate earnings expectations, particularly the robust profit outlook for technology companies closely tied to explosive demand for AI computing infrastructure, which has remained unbroken by the conflict.

Many investors might wonder: Why has the stock market been able to reach new record highs during the Iran conflict? Economists and market analysts widely explain that this is largely because the stock market serves as a barometer reflecting investors’ views on what will happen in the future, rather than an immediate pricing or evaluation of the current situation. They note that investors are essentially treating the Middle East geopolitical conflict as a short episode that will be resolved relatively quickly and are not overly concerned.

Additionally, another major trend has played a significant role in the rebound of global stock markets: growing market confidence in Trump’s ‘backing down at the last minute’ playbook—whereby Trump ultimately chooses to retreat when facing major issues approaching deadlines, leading to a sharp rebound in the stock market, commonly referred to as the ‘TACO’ strategy.

The ‘TACO’ strategy (Trump Always Chickens Out), now widely adopted by traders as one of the hottest trading strategies, involves global equity and bond market investors betting that Trump will eventually back down or that the implemented policies will be significantly weaker than his verbal threats whenever he makes new, more aggressive tariff threats or other major threats that trigger market crashes. Investors then take advantage of opportune downturns to aggressively buy the dip, betting heavily that the stock market will rebound strongly in the near future.

As the U.S. earnings season officially kicked off this week, expectations of strong profit expansion driven by AI computing infrastructure provided a solid foundation, and the market increasingly believes that a long-term ceasefire agreement under domestic pressure will soon be reached between the U.S.-Israel alliance and Iran, as well as Lebanon. Top-tier investment institutions on Wall Street, including Blackrock, Goldman Sachs, and Morgan Stanley, have become marginally more optimistic about the future of the equity market. This highlights how major Wall Street banks are viewing post-ceasefire market valuation recovery, resilient corporate profitability, and upward revisions in earnings for technology companies driven by AI-related demand as evidence of a significant recovery in risk appetite.

Joe Seydl, Senior Market Economist at JPMorgan Private Bank, stated, ‘The stock market is not trying to price in everything happening today.’ ‘It is always attempting to price in what the world will look like six to twelve months from now.’

Why has the stock market shown ‘resilience’? One answer lies in the increasingly robust profitability that companies have demonstrated during the earnings season.

In the view of Mark Hackett, Chief Market Strategist at Nationwide, institutional investors on Wall Street have been the core driving force behind this round of stock market recovery. After experiencing aggressive sell-offs, market attention has shifted back to corporate fundamentals during the earnings season, and he believes these fundamentals are highly supportive.

Wall Street’s top-tier traders currently remain unfazed by negative developments in the Middle East, opting to continue allocating capital to equities. Institutional investors have been the key drivers behind the recent recovery in the U.S. stock market. These investors seem to believe that the impact from the Middle East is more akin to a manageable oil price disruption rather than a systemic supply crisis. As long as the conflict does not undermine the resilience of U.S. corporate earnings, permanently push oil prices into an uncontrollable range, or force the Federal Reserve to adopt a hawkish stance comprehensively, its impact on the stock market will likely be temporary.

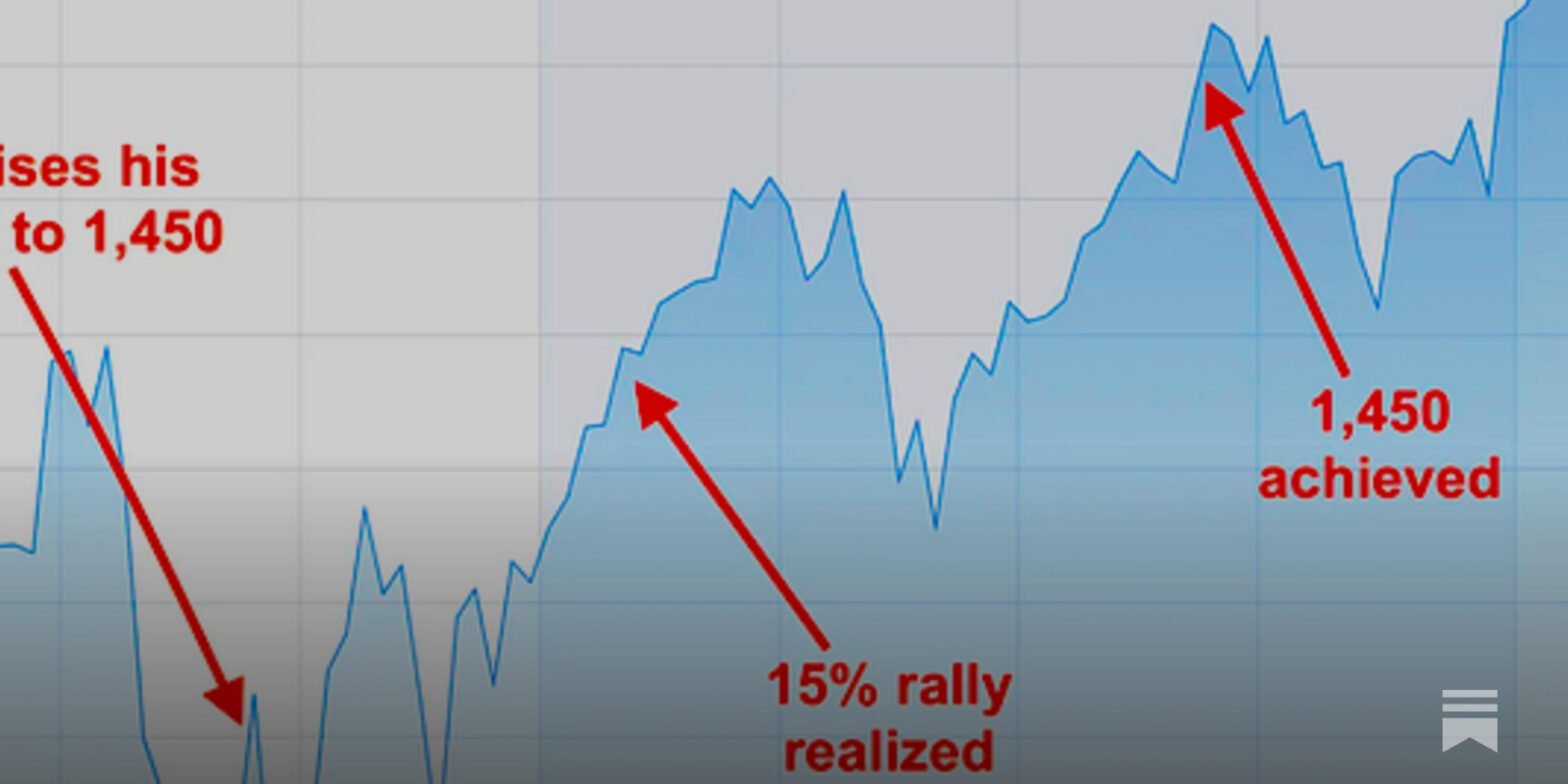

The S&P 500 Index, one of the benchmark indices for the U.S. equity market, fell by approximately 8% during the initial weeks of the Iran war, from February 28, when the conflict began, to a recent low on March 30.

However, since then, global equity markets, including the U.S. stock market, have experienced a strong rebound, erasing all declines since the outbreak of the war. Particularly since April, the uptrends in South Korea, Taiwan, and mainland China’s A-share markets — home to the world’s leading companies in the AI computing power supply chain — have been even stronger. The S&P 500 Index closed at a record high on Thursday, about 11% above its late-March low. The index also set a record closing high on Wednesday.

Mark Zandi, Chief Economist at Moody’s, one of the three major credit rating agencies, stated: ‘The market has shown remarkable resilience in the face of this war and surged strongly amid expectations that geopolitical issues would be resolved.’

At first glance, it seems that not much has changed since the end of February, leaving ordinary investors puzzled by this sudden surge in market enthusiasm.

The initial selloff in the stock market was driven by investor concerns that an oil supply shock could ripple through the global economy, pushing up inflation and potentially leading to ‘stagflation’ — a scenario feared by central banks worldwide.

Iran has effectively continued to disrupt tanker traffic through the Strait of Hormuz, a maritime shipping route through which approximately 20%-30% of the world’s oil and gas passes. This blockade represents the largest oil supply disruption in history, causing oil prices to soar throughout March and significantly raising market expectations of stagflation.

Although the United States and Iran reached a two-week ceasefire agreement on April 7, the blockade remains largely effective.

Moreover, while investors cheered the potential diplomatic de-escalation of the conflict and the possibility of a long-term ceasefire pathway, the temporary ceasefire appears fragile, with both the U.S. and Iran accusing each other of violating the agreement.

With only two weeks left before the expiration of the ceasefire, the parties still failed to reach a long-term peace agreement. US Vice President JD Vance stated that American officials left the peace talks held in Pakistan last weekend after the Iranian delegation rejected the US demand to halt the development of nuclear weapons. However, the robust performance of global stock markets suggests that investors are increasingly confident that the US, Israel, Iran, and Lebanon will eventually reach a long-term stable ceasefire agreement under domestic economic pressures.

From the ‘TACO strategy’ to the profit expansion driven by the AI technology boom: The two core pillars behind the record highs of US equities amidst geopolitical storms.

Economists generally noted that, at its core, the stock market is expressing a collective belief: tensions will ease comprehensively, the war will end soon, oil shipments through the Strait of Hormuz will eventually normalize, and the world will inevitably seek alternative energy routes bypassing the Strait of Hormuz after a long-term peace agreement is reached, similar to how Europe gradually stabilized while reducing dependence on Russian oil and gas.

Economists pointed out that this is largely because investors have been ‘trained over the long term’ to increasingly believe that once economic pain becomes too severe, US President Donald Trump will back down – a concept known as the ‘TACO’ trading strategy, an acronym for ‘Trump always chickens out’.

The increasingly popular trading strategy on Wall Street—TACO (Trump Always Chickens Out): It emerged in April 2025 when Trump launched an unprecedented ‘reciprocal tariff’ campaign against the world. At that time, traders bet that either the US government would withdraw the tariff threat or, even if implemented, it would be far less severe than Trump’s threats and insufficient to significantly drag down US economic expansion.

The term TACO was coined by a Financial Times columnist to describe Trump’s repeated wavering on tariff issues after his ‘Liberation Day’ speech on April 2, 2025, although he eventually backed down, leading to a major stock market rebound. When asked about ‘TACO’ during a press conference, Trump became furious, calling the question ‘malicious.’

The ‘TACO’ strategy has now been widely adopted by traders as the hottest trading strategy. Whenever Trump issues new, more aggressive tariff threats or unleashes other major threats that trigger market crashes, global equity and bond investors bet that he will ultimately back down or that the actual policies implemented will be significantly weaker than his verbal threats, prompting them to aggressively bottom-fish during opportune downturns and heavily wager on a forthcoming stock market rebound.

Zandi remarked, ‘Investors strongly believe – and have been conditioned to increasingly believe – that he will yield, find a way to transition smoothly, declare victory, and move forward.’

Trump has repeatedly refuted claims that he would retreat, describing this brinkmanship strategy as a sophisticated negotiation tactic under his leadership.

Economists cited a recent example of this dynamic: the so-called ‘Liberation Day’ in April 2025, when the Trump administration imposed a series of tariffs on US trading partners globally. Within days – following a sharp drop of over 12% in the US stock market – Trump announced a 90-day suspension of these tariffs. Subsequently, after a significant reversal of Trump’s tariff policy stance, global stock markets experienced one of the largest single-day gains in history.

Seydl noted that investors remember how Trump often de-escalates geopolitical and tariff shocks – which is why they cling to any headlines suggesting positive progress in peace negotiations. ‘The market has a memory,’ Seydl added.

Economists widely agree that other key factors are supporting market resilience during wartime. ‘Among them, investor enthusiasm and confidence in the strong profit trajectory of tech companies, driven by a massive wave of spending on AI computing power, is crucial. These tech stocks account for nearly half of the total market capitalization of the S&P 500,’ Zandi said.

The powerful profit expectations of tech stocks fueled by the AI technology boom also form the core logic driving US equities to new highs and a major rally in global stock markets.

Stocks directly tied to AI computing infrastructure—those carrying both ‘earnings certainty’ and ‘high beta’ attributes, including NVIDIA, Taiwan Semiconductor, AMD, and Broadcom-led ‘AI Computing Power Elite Group’—are often the most sensitive, fastest-moving, and highest-gaining layer in the logic of a broader stock market or tech sector rebound. The core rationale behind this is exceptionally robust: this layer is directly tied to record-breaking AI capital expenditures by tech giants, rather than mere speculative narratives. AI hyperscalers (such as Google, Microsoft, and Amazon) continue their arms race in capital expenditure. As long as they prefer taking on more debt or cutting jobs rather than retreating from the AI capex race (the so-called ‘AI computing power arms race’), leading players in the AI computing power supply chain will remain valuable for allocation.

Blackrock has therefore upgraded its rating for the US and emerging market equities to ‘overweight’, pointing out that profit growth expectations for the technology sector in 2026 have risen to 43%; Citi also upgraded the US stock market to ‘overweight’, considering the valuation after the recent pullback more attractive, with US technology continuing to contribute significantly to global earnings growth.

Equity strategists from Blackrock, the largest asset management giant on Wall Street, have shifted back to an “overweight” stance on U.S. and emerging market equities, primarily because they believe the actual economic damage caused by the new round of Middle Eastern geopolitical conflicts “is likely to be very manageable.” Regarding core investment themes/trends, Blackrock strategists are particularly bullish on semiconductor stocks closely linked to AI computing infrastructure, including key players in the AI computing supply chain listed on U.S., South Korean, and **** stock exchanges.

Blackrock emphasized the upcoming US earnings season, proclaiming that the engine of profit growth can sustain the main theme of a bull market. Strategists wrote: ‘Even during periods of geopolitical conflict, corporate earnings expectations continue to rise, largely due to the robust demand for AI computing power driven by AI-related investment themes.’

Zandi stated: ‘These stocks follow their own logic, independent of any external factors, including the Iran war.’ ‘I believe that if it were not for the extremely optimistic bullish sentiment surrounding the AI mega-trend, we would have fallen further and recovery would have been more challenging.’

Seydl stated that we are currently in an ‘AI-driven tech boom,’ and investors are likely to remain optimistic until they believe this tech cycle has run its course. More broadly, equity investors are essentially betting on a company’s increasingly robust future earnings growth trajectory, while the current earnings backdrop ‘has remained quite solid,’ Seydl noted.

For instance, economists noted that consumer spending appears stable. Zandi mentioned that companies’ post-tax profits are receiving a strong boost from what Republicans call the ‘big and beautiful bill,’ which, among other provisions, makes it easier for businesses to expense investments, thereby reducing their tax burden.

The market has begun to anticipate a new round of a ‘super bull market’ in equities.

The stock market reaching new highs amid geopolitical conflicts underscores why long-term retail investors should stick to their investment plans and ignore the noise.

Seydl said: ‘For ordinary investors, trying to time the market is extremely difficult, if not impossible.’ ‘A better approach is to adopt a long-term investment perspective to weather any sharp volatility.’

The reason the stock market seems to have ‘forgotten about the war’ is not because the market is ignoring geopolitical risks, but rather because it trades on earnings growth trajectories 6 to 12 months ahead, supported by strong earnings resilience and policy support expectations; conversely, the global bond market remains more directly influenced by inflation expectations and interest rate paths tied to rising oil prices.

As technology stocks lead a major rally in global equities—especially with the Nasdaq Composite and S&P 500 indices repeatedly hitting new record highs amid geopolitical tensions—investors have effectively sounded the rallying cry for a new global stock market ‘bull market.’

Tom Lee, a senior stock market strategist known as the ‘Oracle of Wall Street’ and co-founder of Fundstrat, believes that the current position of the U.S. stock market, and even the global stock market, is stronger than when it reached its previous historical high earlier this year. Lee agrees with a typical assessment by the Wall Street financial giant JPMorgan, which states that the technology sector centered on AI computing power infrastructure must lead the main theme of the next super bull market phase. Citi has upgraded its rating for U.S. stocks from ‘neutral’ to ‘overweight,’ and the institution forecasts that the S&P 500 index will reach 7,700 points by the end of the year. As of Thursday’s closing on the U.S. stock market, the S&P 500 index closed at 7041.28 points.

The narrative driving the current new bull market is essentially supported by three key factors: the resilience of corporate earnings demonstrated in the latest U.S. earnings season, the renewed risk appetite driven by tech stocks and AI computing themes, and the market’s judgment that the impact of Middle Eastern tensions will not evolve into long-term inflation akin to that of 2022. As long as these three pillars remain intact, Wall Street will continue to treat war-related headlines as mere trading noise.

According to Citi’s latest research report, the technology sector, which had been suppressed by geopolitical conflicts, valuation concerns, and overly optimistic expectations, is now entering a window where risk appetite recovery is transitioning to fundamental revaluation. Following a marginal cooling of tensions in Iran, the market swiftly shifted from safe-haven assets back to risk assets, with both the S&P 500 and Nasdaq indices strengthening simultaneously. This indicates that capital has begun to focus on ‘the overall future earnings growth trajectory driven by AI’ rather than ‘current panic.’ Within this framework, tech stocks—especially large tech platforms—are no longer merely liquidity-driven抱团targets but have once again become the core anchor of risk appetite and earnings expectations in the U.S. stock market.

Citi’s strategy team emphasized that the market is transitioning from a narrow bull market characterized by ‘a few leading AI companies’ to a broader upward trend that spreads ‘from point to surface.’ However, this transition hinges on two conditions being met simultaneously: first, leading tech companies must continue to justify their high valuations through earnings and guidance, proving that they are not a bubble; second, geopolitical risks must continue to evolve in a predictable and manageable direction. Once these two conditions are satisfied, the market will gradually expand from a few heavyweight tech stocks to a broader range of software, communication services, and even cross-sector cyclical segments, potentially forming a ‘market breadth improvement bull market scenario’ in the summer.