Inflation-adjusted Dow index

Dan Runkevicius

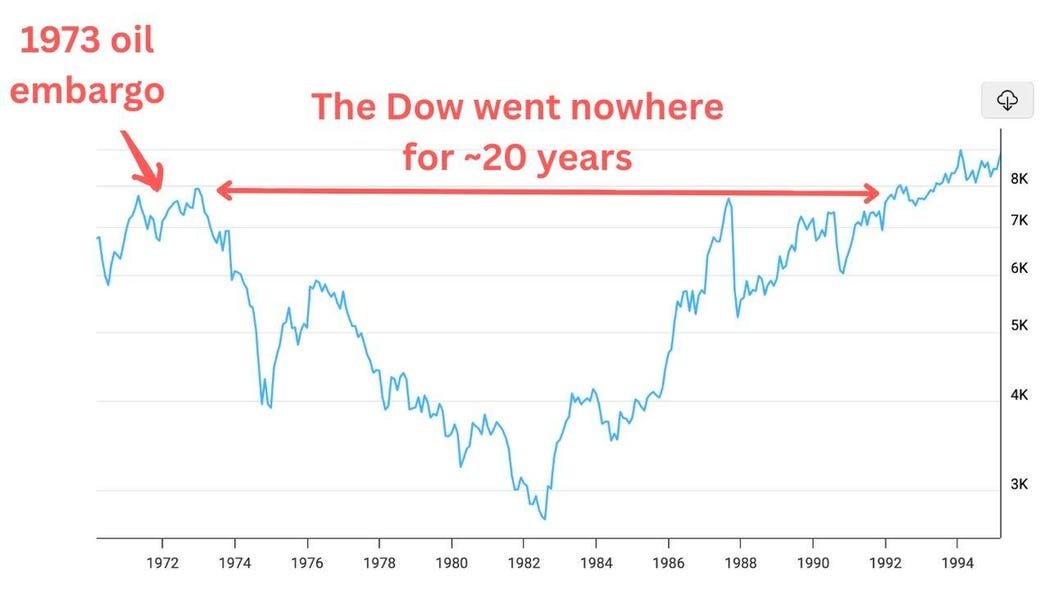

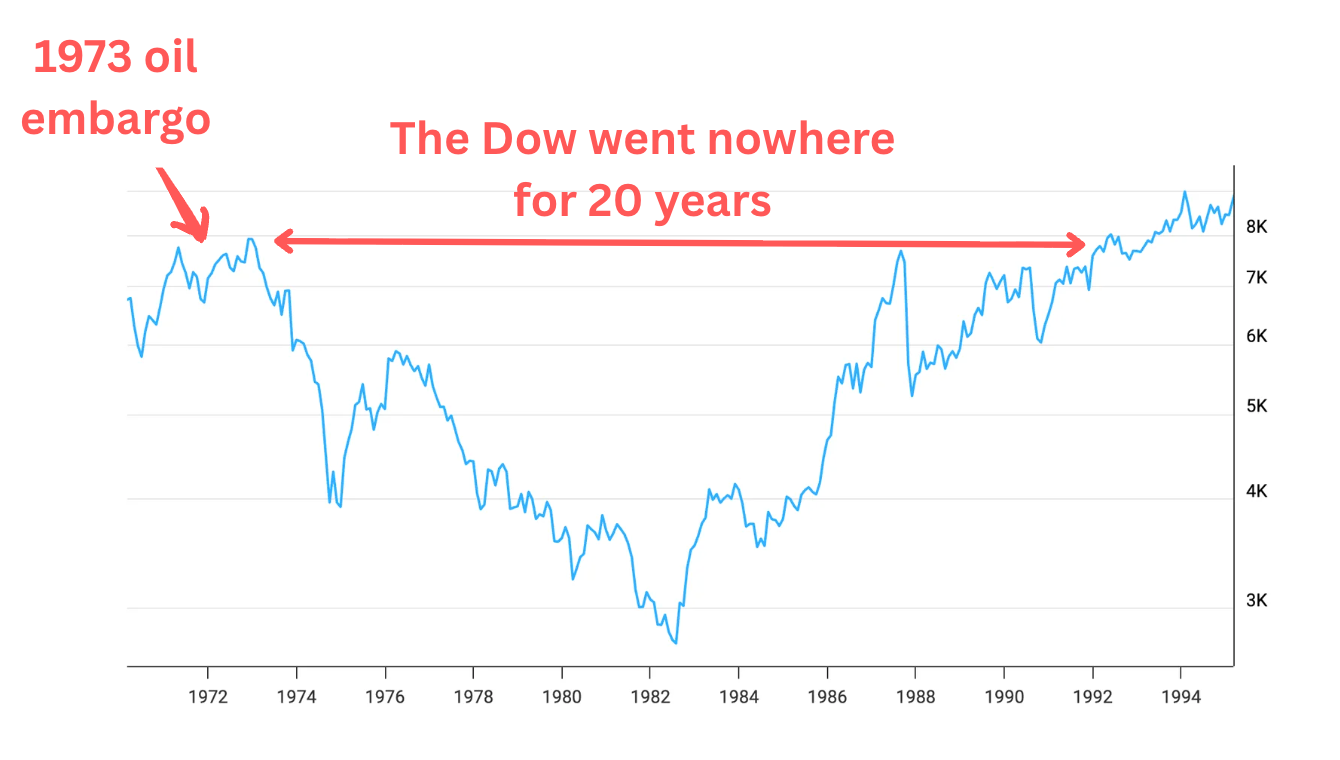

After 1973’s oil shock, the Dow crashed 40%, plunging into what was later dubbed a “lost decade.” Adjusted for inflation, it took the index roughly 20 years to recover. Can that happen again?

The parallel is striking. The same place, same key adversaries, in a way, the same political motives, and most importantly, the disruption happening right now is surprisingly similar in scale to that of 1973.

On paper, the Hormuz blockade took offline 20 million barrels per day, or about 20% of global supply. That’s roughly five times more than in 1973, when the oil embargo erased around 4.5 million barrels per day.

But as Nobel Prize-winning economist Paul Krugman pointed out, comparing 1973’s immediate supply losses understates the shortfall it created back in the 1970s.

“World oil supply fell only moderately after 1973, but it had been on a rapidly rising trend until then, so there was a large shortfall relative to that trend,” he wrote in a recent Substack.

If we adjust for trend, the 1973 embargo wiped out about 17.5% of oil output by 1975, which is roughly in line with today’s shortfall. And the aftereffects haunted the U.S. for decades.

Double-digit inflation, the most severe recession since the Great Depression, the highest unemployment since World War II, and a stock market that went nowhere until the 1990s.

By Krugman’s estimates, the equivalent economic downturn today would mean negative or at best zero growth for the next several years, unleashing a “global disaster.”

“A comparable slowdown now would mean zero or negative world growth over the next two years, compared with the current IMF forecast of 3 percent. This would be a true global disaster,” he wrote.

But while the scale is, again, surprisingly similar, 2026 is not 1973. Perhaps the most obvious difference is that the world is far less dependent on oil than it was in the 1970s by almost any measure.

Not only does the U.S. have strategic oil reserves, it’s also a net oil exporter. Other major economies are far more insulated as well. So Iran can only blackmail the world with marginal supply disruptions because, long term, you can’t starve a country of oil if it produces more than it needs.

Then there’s the fact that this oil shock is Iran’s doing alone. Unlike in 1973, other Arab OPEC members have no interest in embargoing the U.S. In fact, the Saudis and other major OPEC exporters are rerouting oil supplies through pipelines to bypass Iran.

So far, the market is betting this is not a repeat of 1973 and that oil prices will fall back toward $60 per barrel by year-end, adding roughly 0.7 percentage points to headline inflation.

Not exactly a 1973-style disruption, but there’s one condition: Hormuz has to reopen by summer.