Primoris Services (PRIM) has landed in the spotlight after recent analyst coverage initiated with a bullish outlook, as investors take notice of its growing role in the accelerating data center construction sector tied to AI and cloud growth.

See our latest analysis for Primoris Services.

Primoris Services has powered higher this year, notching an impressive 52.97% share price return over the past 90 days, and an even more astonishing 123.98% total shareholder return over one year. Momentum has clearly built as investors bet on its growth potential tied to the data center and AI infrastructure boom, making recent analyst optimism appear well-founded.

If you’re curious where the next big opportunities may be, it is a great moment to uncover other fast-growing stocks with high insider ownership. See what’s out there with our fast growing stocks with high insider ownership.

With analyst coverage remaining broadly optimistic and shares already surging, investors must now ask whether Primoris Services is still undervalued, or if future growth has already been priced in by the market. Is there a true buying opportunity here, or has the market moved ahead of itself?

Most Popular Narrative: 2% Overvalued

Primoris Services closed at $141.79, just above the most widely followed narrative’s fair value estimate of $139.56. This sets up an interesting debate between current market optimism and longer-term analyst expectations.

Operational execution, improved productivity, and a favorable project mix in core segments (especially Utilities) are driving company-wide gross margin improvement and improved cash conversion, structurally enhancing Primoris’s earnings and free cash flow profile.

Wondering what ambitious financial targets drive this high sticker price? The narrative hinges on bold projections for record revenues, expanding profit margins, and a powerful earnings ramp, anchored in some aggressive future assumptions. Curious how these numbers stack up against sector norms or if the bar is set too high? You’ll want to check the full narrative to unpack the forecasts behind this valuation.

Result: Fair Value of $139.56 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, a slowdown in data center contract wins or ongoing margin pressures in renewables could quickly shift market sentiment away from the current optimism.

Find out about the key risks to this Primoris Services narrative.

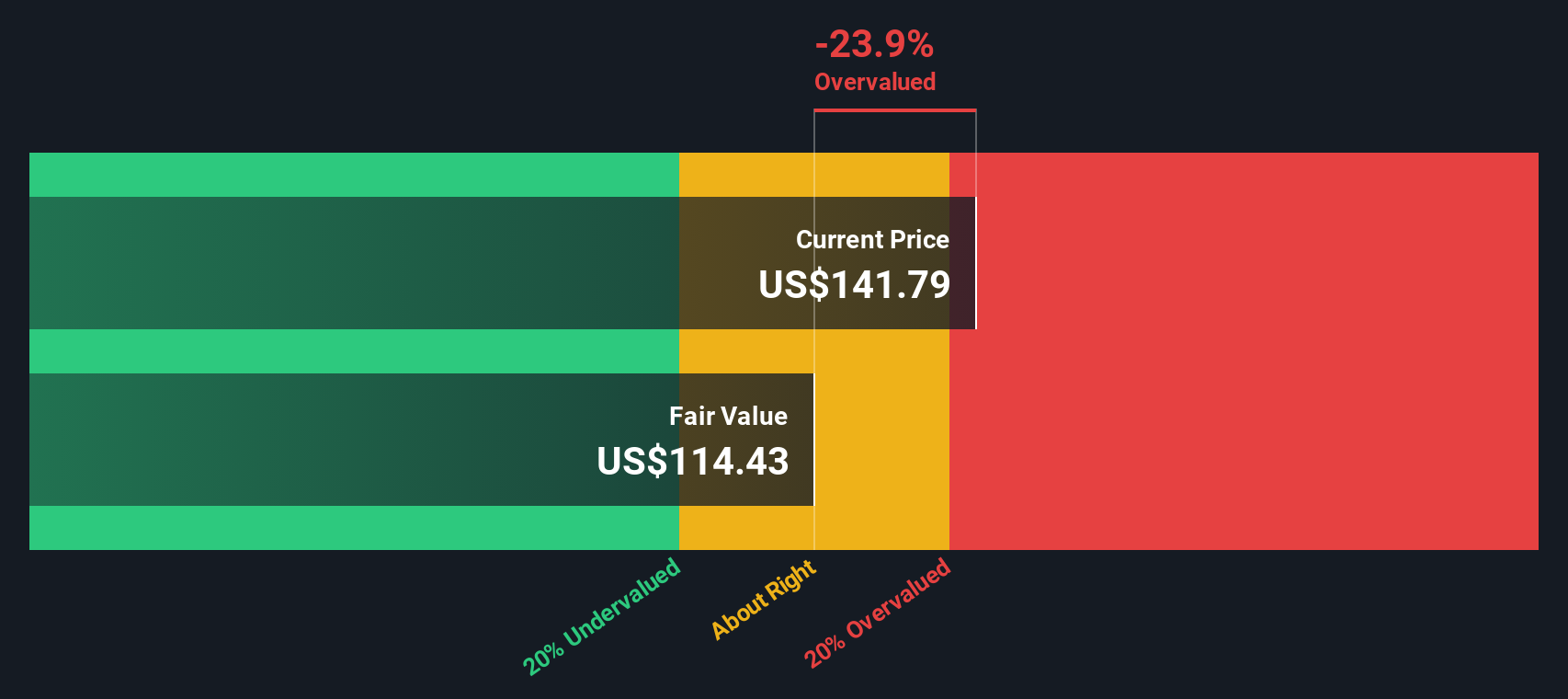

Another View: SWS DCF Model Challenges the Premium

Looking through a different lens, the SWS DCF model values Primoris Services at $114.43 per share, which is well below its current market price of $141.79. This suggests that, based on future cash flow projections, the stock could be overvalued relative to its fundamentals. Will investors keep pushing higher, or will reality bring the price closer to this conservative fair value?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Primoris Services Narrative

Want to dig deeper or think your perspective brings something new? Investigate the data for yourself and shape a custom narrative in minutes: Do it your way.

A great starting point for your Primoris Services research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Opportunities?

Stay ahead by uncovering unique stocks in fast-moving sectors, well before they become the talk of the market. Use these winning ideas and make sure you’re not left behind:

- Seize the chance for powerful income streams by targeting companies known for reliable payouts through these 19 dividend stocks with yields > 3% with high yields and strong fundamentals.

- Ride the momentum of innovation and get in early on market disruptors shaping tomorrow’s healthcare landscape. Start your search with these 34 healthcare AI stocks.

- Capitalize on the digital currency surge by following these 80 cryptocurrency and blockchain stocks that are redefining payment systems and blockchain-powered solutions worldwide.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com